Chapter 11: Notes, Bonds, and Leases

Student: ___________________________________________________________________________

1. Firms typically finance long-term assets, particularly property, plant, and equipment, with long-term

2. The more long-term debt in a firm’s capital structure, the less the risk that the firm will experience difficulty

4. Modern business usage has come to restrict the word equity to mean only shareholders’ equity, both

7. The amount borrowed initially and the market value of a note or bond at any date subsequent to the initial

borrowing equals the present value of the future, or remaining, cash flows discounted at an appropriate interest

8. The internal rate of return, often called yield to maturity, is the discount rate that equates the future cash

10. Common terminology refers to the calculations for amortizing a financial instrument to its maturity value

12. When the coupon rate equals the historical market interest rate or initial yield to maturity, then the initial

13. U.S. GAAP and IFRS provide for two methods of accounting for long-term leases: the operating lease

14. Operating leases are economically similar to purchasing assets with funds obtained from issuing long-term

15. Capital leases are economically similar to purchasing assets with funds obtained from issuing long-term

16. When analyzing leases, the risks of ownership include the risk of interest rate increases, the risk of

17. Firms must disclose in notes to the financial statements the cash flows associated with capital leases and

18. Both the lease asset and the lease liability appear on the lessee’s balance sheet under the capital lease

19. The capital lease method classifies all of the lease payment each period as an operating

22. Big City Electric is a regulated monopoly providing electric services in a large city. Property, plant, and

23. Charm City Electric is a regulated monopoly providing electric services in a large city. Property, plant, and

24. Divine Paper, a United States-based company, processes wood pulp into paper products in fixed-asset

intensive facilities. It has a large ratio of property, plant, and equipment to total assets and a high debt-equity

25. Excellent Paper, a United States-based company, processes wood pulp into paper products in fixed-asset

intensive facilities. It has a large ratio of property, plant, and equipment to total assets and a high debt-equity

26. First Communications Group is a communication services firm whose employees provide advertising,

market research, public relations, and other services world-wide. Other than relatively small amounts of

equipment, it owns virtually no property, plant, and equipment (it leases most of its office space). Which of the

27. General Semiconductor is a European-based designer and manufacturer of semiconductors. It manufactures

semiconductors in fixed-asset intensive plants. The moderate fraction of its total assets that are property, plant,

and equipment results from depreciating its technology-intensive manufacturing facilities over periods as short

28. Firms that need cash for long-term purposes, such as acquiring buildings and equipment or financing a

29. Firms that need cash for long-term purposes, such as acquiring buildings and equipment or financing a

33. A _____ is a financial contract in which the borrower and the lender agree to certain conditions about

37. A zero coupon bond provides for _____ periodic payments of interest while the bond is outstanding; and the

38. A _____ bond requires periodic payments of interest plus a portion of the principal throughout the life of the

39. Some bonds are _____, which means the issuing firm has the right to repurchase the bonds prior to maturity

40. Investors in bonds sometimes hold a _____ option, meaning they can force the issuing company to repay the

41. Investors in bonds might exercise a _____ option if interest rates increase, and investors can reinvest the

42. The typical _____ bond pays interest periodically, usually every six months, during the life of the bond and

43. _____bonds permit the holder to exchange the bonds for shares of the firm’s common stock under certain

44. The conversion option of convertible bonds has value because the holder can benefit from some of the later

45. What determine(s) the risk of investing in a bond issue, which in turn affects the interest rate investors

47. _____ of a note or bond at any date subsequent to the initial borrowing equals the present value of the

48. The amount borrowed initially and the market value of a note or bond at any date subsequent to the initial

50. The approach which dominates current financial reporting of financial instruments [uses the historical

market interest rate to compute the carrying value of notes and bonds while these obligations are outstanding] is

51. Firms typically borrow from banks, insurance companies, and other financial institutions by signing a note,

52. When the stated interest rate for a loan equals the yield required by the lender, then the amount borrowed

54. _____ often advise corporate borrowers on the sorts of financial instruments the lending market appears to

55. Bonds whose indentures contain a provision which gives the issuing company the option to retire portions of

the bond issue before maturity if it so desires, but the provision does not require the company to do so are called

57. A firm classifies mortgages, notes, bonds, and leases which were used to acquire its long-term assets that

58. When the bond indenture provides that stated amounts of principal will become due during the term of the

60. Bonds whose indentures contain a provision which requires the issuing firm to make a provision for partial

62. In return for promising to make future payments, a firm receives cash or other assets with a measurable

cash-equivalent value. The firm records a long-term liability for that amount and the book value of that

63. In return for promising to make future payments, a firm receives cash or other assets with a measurable

cash-equivalent value. The firm records a long-term liability for that amount and determines the market interest

65. Borrowers who retire long-term liabilities debit the liability account for its current book value, credit Cash,

66. Bonds whose indentures contain a provision which requires the issuing firm to make a provision for partial

68. In historical cost accounting, the discounting process uses the original interest rate appropriate for the

particular borrower at the time it incurred the obligation. That rate will have depended on the amount and terms

of the borrowing arrangement as well as the risk that the borrower will default on the obligations. The rate is

69. A document or agreement giving the terms of the bond and the rights and duties of the borrower and other

parties to the contract that provides some protection to the bondholders and typically limits the borrower's right

70. The most common type of corporate bond, except in the railroad and public utility industries, that carries no

71. A bond that does not require a periodic cash payment, but instead promises a single payment at maturity, is

72. Debentures that the holder (lender) can exchange, possible after some specific period of time has elapsed,

for a specific number of shares of common stock or, perhaps, preferred stock of the borrower are called _____

73. Common terminology refers to the calculations for amortizing a financial instrument to its maturity value

75. An initial issue price equal to the face value of the bonds means that the implicit interest rate equals the

76. On January 1, Year 4, Jones Realty Company issued 8 percent term bonds with a face amount of $1 million

due January 1, Year 14. Interest is payable semi-annually on January 1 and July 1. On the date of issue,

investors were willing to accept an effective interest rate of 6 percent. Assume the bonds were issued on

January 1, Year 4. for $1,148,959. Using the effective interest amortization method, Jones Realty Company

77. On January 1, Year 4, Jones Realty Company issued 8 percent term bonds with a face amount of $1 million

due January 1, Year 14. Interest is payable semi-annually on January 1 and July 1. On the date of issue,

investors were willing to accept an effective interest rate of 6 percent. Assume the bonds were issued on

78. On February 1, Year 1, Centra issues $100,000 semi-annual 12% bonds at par plus accrued interest. The

interest is payable on July 1 and January 1 of each year. What entry is necessary to record the issuance of the

79. In Year 7, Nortel Manufacturing issued $100,000 semi-annual 12% bonds at par. Interest is payable on July

81. Fox Co., Inc.

On January 1, Year 1, Fox Co., Inc., issues $100,000 par value, 10% bonds maturing in 10 years to yield 12%

per year, compounded semiannually on January 1 and July 1. Use the present value tables.

Refer to the Fox Co. Inc. example. What is the bonds payable account (net of any bond discount or premium)

82. Fox Co., Inc.

On January 1, Year 1, Fox Co., Inc., issues $100,000 par value, 10% bonds maturing in 10 years to yield 12%

per year, compounded semiannually on January 1 and July 1. Use the present value tables.

84. (CMA adapted, Jun 86 #5) A bond issue sold at a premium is valued on the statement of financial position

85. (CMA adapted, Dec 86 #20) On January 1, Year 1, Nicole Company sold its 5-year, $100,000 face value,

8% bonds at $108,530, to yield an effective annual interest rate of 6%. The bonds are dated January 1, Year 1,

and interest is payable annually on January 1. Using the effective interest method of premium amortization, the

86. Heather Corporation

Heather Corporation issued $2,000,000, 10-percent, 10-year bonds on January 2, Year 2. The bonds pay interest

semiannually on January 1 and July 1. The bonds were priced on the market to yield 8 percent.

87. (CMA adapted, Dec 90 #12) Marla, Inc. issued $6,000,000 of 12% bonds on December 1, Year 1, due on

December 1, Year 6, with interest payable each December 1 and June 1. The bonds sold for $5,194,770 to yield

16%. If the discount is amortized by the effective interest method, Marla, Inc.'s interest expense for the fiscal

88. U.S. GAAP and IFRS permit firms to account for notes and bonds under which of the following

89. The FASB and the IASB refer to the approach that uses the current market interest rate instead of the

90. A firm that does not account for long-term notes and bonds using the fair value option, uses the _____ to

91. Authoritative guidance requires firms that account for notes and bonds using the _____ market interest rate

to report the carrying values, or book values, on the balance sheet and to disclose the _____ of these notes and

95. The capital lease method is appropriate when the lessee enjoys most of the _____ and bears most of the

96. The operating lease method is appropriate when the lessor enjoys most of the _____ and bears most of the

100. The capital lease method classifies the portion of the lease payment related to interest expense as an

104. Firms must disclose in notes to the financial statements the cash flows associated with capital leases and

with operating leases for each of the succeeding _____ years and for all years after _____ years in the

110. (CMA adapted, Dec 92 #10) There are many similarities between lessee and lessor accounting for the

111. Henson Manufacturing Company signed a 3-year contract for the use of certain manufacturing equipment

with an estimated life of three years. Henson Manufacturing Company cannot cancel the contract. What entry is

112. Quan Restaurant

On January 1, Year 7, Quan Restaurant is planning to enter as the lessee into the two lease agreements

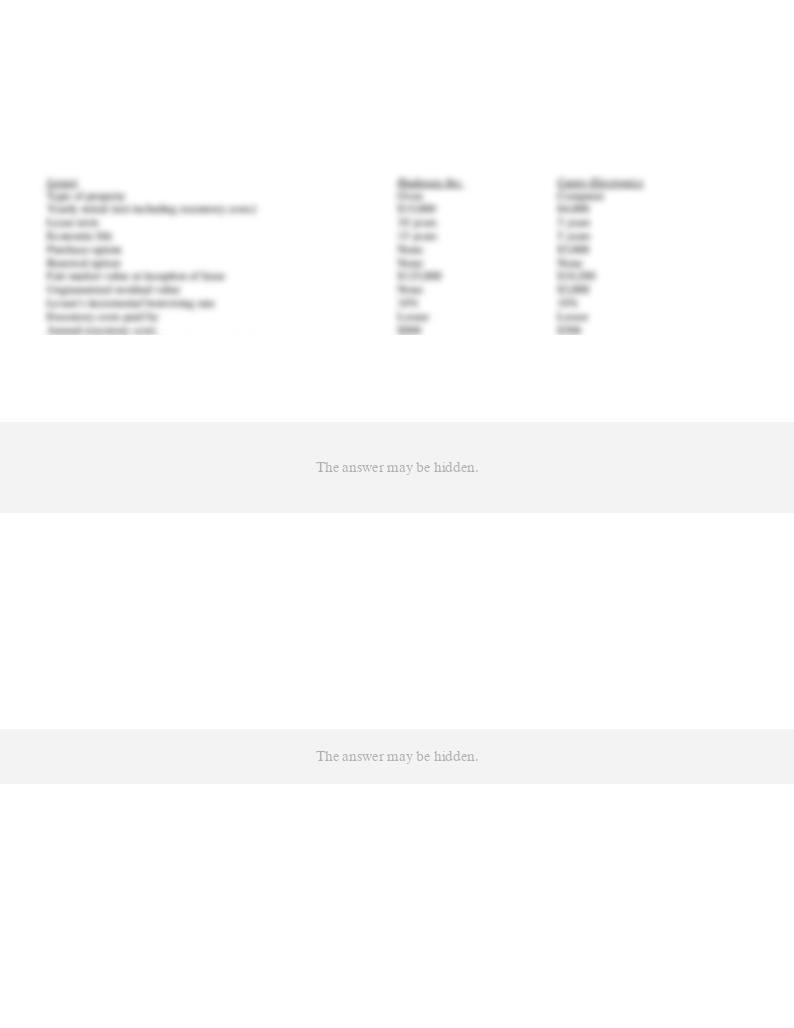

described below. Each lease is noncancelable, and Quan does not receive title to either leased property during or

at the end of the lease term. All payments required under these agreements are due on January 1 each year.

Present value factor at 10% (of an annuity due)

6.76

2.74

113. Quan Restaurant

On January 1, Year 7, Quan Restaurant is planning to enter as the lessee into the two lease agreements

described below. Each lease is noncancelable, and Quan does not receive title to either leased property during or

at the end of the lease term. All payments required under these agreements are due on January 1 each year.

Present value factor at 10% (of an annuity due)

6.76

2.74

(CMA adapted, Dec 93 #28) Refer to the Quan Restaurant example. Quan Restaurant should treat the lease agreement with Cutter Electronics as

114. On January 1, Year 1, Lamp Company acquires new equipment in exchange for a note. Lamp must pay a

lump sum of $32,000 on December 31, Year 3. The equipment is being specifically manufactured for Lamp, so

no market price exists for the equipment. On similar types of equipment purchases, Lamp has paid 15% interest.

The equipment has a five-year life and the company uses straight-line depreciation with a 10% salvage value.

Required:

Prepare journal entries to record the following:

115. On January 1, Year 6, Pearson Corporation issued $1,000,000 face value, 20-year bonds. The bonds carry

coupon interest of 6 percent per year, payable semiannually on June 30 and December 31. The bonds were

initially priced on the market to yield 8 percent, compounded semiannually (for an effective annualized yield

greater than 8 percent).

Required:

a.

Compute the issue price of these bonds on January 1, Year 6.

b.

Compute the amount of interest expense on these bonds for Year 6, assuming that the firm uses the effective-interest method of amortizing

bond premium or discount.

116. Rotor Corporation issues $10,000,000 face value, 10-year, 6% semiannual coupon bonds

on January 1, 2013. The bonds require coupon payments on June 30 and December 31 of

each year. The market initially priced the bonds to yield 6% compounded semiannually.

The current market yield on these bonds was 6.2% compounded semiannually on June 30,

2013, and 6.6% compounded semiannually on December 31, 2008. Rotor Corporation

computes interest expense for each six-month period using the market yield at the beginning

of the period.

Required:

117. Indicate whether each of the following independent transactions is a capital (C) or operating (O) lease.

118. The annual report of Sign Corporation for Year 1 reports capital leases requiring payments totaling $228

million over future years, including $58 million payable at the end of Year 2. The interest rate on these

obligations is 12 percent and their present value (discounted at 12 percent) at the end of Year 1 was $181

million. The assets financed by capital leases appear on the Year 1 year-end balance sheet at $220 million.

Assume no new leases were entered into during Year 2 and that leasehold assets have a remaining useful life of

10 years at the start of Year 2, but no salvage value. Ignore income taxes.

Required:

119. ALT Company, as tenant, acquired for $600,000, paid in a single amount, the right to use an entire office

building for the next ten years. ALT expects to rent out the floors in the building to various commercial tenants.

As tenant, ALT accounts for its lease as a capital lease amortizing the leasehold asset on a straight-line basis

over ten years. ALT, as landlord, signed operating leases with the tenants for all of the rentable space. The rents

total $150,000 received at the end of each year for the next ten years, $1.5 million in total.

Required:

120. Bolton Co. leases workout equipment to health clubs. On January 1, Year 1, Bolton Co. leases to

121. Raines Corporation entered into a five-year lease for a computer on January 1, Year 3. The lease requires

Raines to make equal payments of $20,000 on January 1 each year for the five years of the lease, with the first

payment made on January 1, Year 3. Raines’ borrowing rate is 10 percent. Raines uses the straight-line

depreciation method for financial reporting. It estimates a zero salvage value. The accounting period is the

calendar year. Round amounts to the nearest dollar.

Required:

122. The following information is available from the comparative balance sheets and related income statement

of the Horner Company for the year ended December 31, Year 7.

December 31,

December 31,

Year 6

Year 7

Present value of lease obligation

$2,040,508.60

$1,862,939.10

123. Describe the sources of long-term debt financing.

124. Consider a firm that recently issued bonds. Further, consider that the firm also set up a bond sinking fund.

Required:

a.

Why would a firm create a long-term liability?

b.

Why would a firm set up a bond sinking fund?

c.

If a firm paid $10,000 into its bond sinking fund at the end of the year, how would this transaction be journalized?

125. Part 1: Briefly explain a bond contract and its relationship to cash flows.

126. How are bonds measured at issuance?

127. Describe what bond provisions exist.

128. What are the cash flows patterns related to bonds?

129. When a company issues bonds, it must sometimes issue them at a discount, while at other times it will

issue them at a premium.

130. What are the general principles for measuring financial instruments?

131. How are notes valued and accounted for under the authoritative guidance?

132. What are the requirements for the disclosure of the carrying and fair values of debt?

133. Discuss the fair value option in accounting for certain assets and liabilities.

134. Describe the various methodologies in accounting for leases.

135. Describe the effect of the operating and capital lease methods on the financial statements of the lessee.

136. What factors enter into choosing the accounting method for leases under U.S. GAAP and IFRS?

137. How does a lessor account for leases?

138. What are the effect of the operating and capital lease methods on the financial statements of the lessor?

139. What disclosures are required for leases?

Chapter 11: Notes, Bonds, and Leases Key

1. Firms typically finance long-term assets, particularly property, plant, and equipment, with long-term

2. The more long-term debt in a firm’s capital structure, the less the risk that the firm will experience difficulty

4. Modern business usage has come to restrict the word equity to mean only shareholders’ equity, both

7. The amount borrowed initially and the market value of a note or bond at any date subsequent to the initial

borrowing equals the present value of the future, or remaining, cash flows discounted at an appropriate interest

8. The internal rate of return, often called yield to maturity, is the discount rate that equates the future cash

10. Common terminology refers to the calculations for amortizing a financial instrument to its maturity value

12. When the coupon rate equals the historical market interest rate or initial yield to maturity, then the initial

13. U.S. GAAP and IFRS provide for two methods of accounting for long-term leases: the operating lease

14. Operating leases are economically similar to purchasing assets with funds obtained from issuing long-term

15. Capital leases are economically similar to purchasing assets with funds obtained from issuing long-term

16. When analyzing leases, the risks of ownership include the risk of interest rate increases, the risk of

17. Firms must disclose in notes to the financial statements the cash flows associated with capital leases and

18. Both the lease asset and the lease liability appear on the lessee’s balance sheet under the capital lease

19. The capital lease method classifies all of the lease payment each period as an operating

22. Big City Electric is a regulated monopoly providing electric services in a large city. Property, plant, and

23. Charm City Electric is a regulated monopoly providing electric services in a large city. Property, plant, and

24. Divine Paper, a United States-based company, processes wood pulp into paper products in fixed-asset

intensive facilities. It has a large ratio of property, plant, and equipment to total assets and a high debt-equity

25. Excellent Paper, a United States-based company, processes wood pulp into paper products in fixed-asset

intensive facilities. It has a large ratio of property, plant, and equipment to total assets and a high debt-equity

26. First Communications Group is a communication services firm whose employees provide advertising,

market research, public relations, and other services world-wide. Other than relatively small amounts of

equipment, it owns virtually no property, plant, and equipment (it leases most of its office space). Which of the

27. General Semiconductor is a European-based designer and manufacturer of semiconductors. It manufactures

semiconductors in fixed-asset intensive plants. The moderate fraction of its total assets that are property, plant,

and equipment results from depreciating its technology-intensive manufacturing facilities over periods as short

28. Firms that need cash for long-term purposes, such as acquiring buildings and equipment or financing a

29. Firms that need cash for long-term purposes, such as acquiring buildings and equipment or financing a

33. A _____ is a financial contract in which the borrower and the lender agree to certain conditions about

37. A zero coupon bond provides for _____ periodic payments of interest while the bond is outstanding; and the

38. A _____ bond requires periodic payments of interest plus a portion of the principal throughout the life of the

39. Some bonds are _____, which means the issuing firm has the right to repurchase the bonds prior to maturity

40. Investors in bonds sometimes hold a _____ option, meaning they can force the issuing company to repay the

41. Investors in bonds might exercise a _____ option if interest rates increase, and investors can reinvest the

42. The typical _____ bond pays interest periodically, usually every six months, during the life of the bond and

43. _____bonds permit the holder to exchange the bonds for shares of the firm’s common stock under certain

44. The conversion option of convertible bonds has value because the holder can benefit from some of the later

45. What determine(s) the risk of investing in a bond issue, which in turn affects the interest rate investors

47. _____ of a note or bond at any date subsequent to the initial borrowing equals the present value of the

48. The amount borrowed initially and the market value of a note or bond at any date subsequent to the initial

50. The approach which dominates current financial reporting of financial instruments [uses the historical

market interest rate to compute the carrying value of notes and bonds while these obligations are outstanding] is

51. Firms typically borrow from banks, insurance companies, and other financial institutions by signing a note,

52. When the stated interest rate for a loan equals the yield required by the lender, then the amount borrowed

54. _____ often advise corporate borrowers on the sorts of financial instruments the lending market appears to

55. Bonds whose indentures contain a provision which gives the issuing company the option to retire portions of

the bond issue before maturity if it so desires, but the provision does not require the company to do so are called

57. A firm classifies mortgages, notes, bonds, and leases which were used to acquire its long-term assets that

58. When the bond indenture provides that stated amounts of principal will become due during the term of the

60. Bonds whose indentures contain a provision which requires the issuing firm to make a provision for partial

62. In return for promising to make future payments, a firm receives cash or other assets with a measurable

cash-equivalent value. The firm records a long-term liability for that amount and the book value of that

63. In return for promising to make future payments, a firm receives cash or other assets with a measurable

cash-equivalent value. The firm records a long-term liability for that amount and determines the market interest

65. Borrowers who retire long-term liabilities debit the liability account for its current book value, credit Cash,

66. Bonds whose indentures contain a provision which requires the issuing firm to make a provision for partial

68. In historical cost accounting, the discounting process uses the original interest rate appropriate for the

particular borrower at the time it incurred the obligation. That rate will have depended on the amount and terms

of the borrowing arrangement as well as the risk that the borrower will default on the obligations. The rate is

69. A document or agreement giving the terms of the bond and the rights and duties of the borrower and other

parties to the contract that provides some protection to the bondholders and typically limits the borrower's right

70. The most common type of corporate bond, except in the railroad and public utility industries, that carries no

71. A bond that does not require a periodic cash payment, but instead promises a single payment at maturity, is

72. Debentures that the holder (lender) can exchange, possible after some specific period of time has elapsed,

for a specific number of shares of common stock or, perhaps, preferred stock of the borrower are called _____

73. Common terminology refers to the calculations for amortizing a financial instrument to its maturity value

75. An initial issue price equal to the face value of the bonds means that the implicit interest rate equals the

76. On January 1, Year 4, Jones Realty Company issued 8 percent term bonds with a face amount of $1 million

due January 1, Year 14. Interest is payable semi-annually on January 1 and July 1. On the date of issue,

investors were willing to accept an effective interest rate of 6 percent. Assume the bonds were issued on

January 1, Year 4. for $1,148,959. Using the effective interest amortization method, Jones Realty Company

77. On January 1, Year 4, Jones Realty Company issued 8 percent term bonds with a face amount of $1 million

due January 1, Year 14. Interest is payable semi-annually on January 1 and July 1. On the date of issue,

investors were willing to accept an effective interest rate of 6 percent. Assume the bonds were issued on

78. On February 1, Year 1, Centra issues $100,000 semi-annual 12% bonds at par plus accrued interest. The

interest is payable on July 1 and January 1 of each year. What entry is necessary to record the issuance of the

79. In Year 7, Nortel Manufacturing issued $100,000 semi-annual 12% bonds at par. Interest is payable on July

81. Fox Co., Inc.

On January 1, Year 1, Fox Co., Inc., issues $100,000 par value, 10% bonds maturing in 10 years to yield 12%

per year, compounded semiannually on January 1 and July 1. Use the present value tables.

Refer to the Fox Co. Inc. example. What is the bonds payable account (net of any bond discount or premium)

82. Fox Co., Inc.

On January 1, Year 1, Fox Co., Inc., issues $100,000 par value, 10% bonds maturing in 10 years to yield 12%

per year, compounded semiannually on January 1 and July 1. Use the present value tables.

84. (CMA adapted, Jun 86 #5) A bond issue sold at a premium is valued on the statement of financial position

85. (CMA adapted, Dec 86 #20) On January 1, Year 1, Nicole Company sold its 5-year, $100,000 face value,

8% bonds at $108,530, to yield an effective annual interest rate of 6%. The bonds are dated January 1, Year 1,

and interest is payable annually on January 1. Using the effective interest method of premium amortization, the

86. Heather Corporation

Heather Corporation issued $2,000,000, 10-percent, 10-year bonds on January 2, Year 2. The bonds pay interest

semiannually on January 1 and July 1. The bonds were priced on the market to yield 8 percent.

87. (CMA adapted, Dec 90 #12) Marla, Inc. issued $6,000,000 of 12% bonds on December 1, Year 1, due on

December 1, Year 6, with interest payable each December 1 and June 1. The bonds sold for $5,194,770 to yield

16%. If the discount is amortized by the effective interest method, Marla, Inc.'s interest expense for the fiscal

88. U.S. GAAP and IFRS permit firms to account for notes and bonds under which of the following

89. The FASB and the IASB refer to the approach that uses the current market interest rate instead of the

90. A firm that does not account for long-term notes and bonds using the fair value option, uses the _____ to

91. Authoritative guidance requires firms that account for notes and bonds using the _____ market interest rate

to report the carrying values, or book values, on the balance sheet and to disclose the _____ of these notes and

95. The capital lease method is appropriate when the lessee enjoys most of the _____ and bears most of the

96. The operating lease method is appropriate when the lessor enjoys most of the _____ and bears most of the

100. The capital lease method classifies the portion of the lease payment related to interest expense as an

104. Firms must disclose in notes to the financial statements the cash flows associated with capital leases and

with operating leases for each of the succeeding _____ years and for all years after _____ years in the

110. (CMA adapted, Dec 92 #10) There are many similarities between lessee and lessor accounting for the

111. Henson Manufacturing Company signed a 3-year contract for the use of certain manufacturing equipment

with an estimated life of three years. Henson Manufacturing Company cannot cancel the contract. What entry is

112. Quan Restaurant

On January 1, Year 7, Quan Restaurant is planning to enter as the lessee into the two lease agreements

described below. Each lease is noncancelable, and Quan does not receive title to either leased property during or

at the end of the lease term. All payments required under these agreements are due on January 1 each year.

Present value factor at 10% (of an annuity due)

6.76

2.74

113. Quan Restaurant

On January 1, Year 7, Quan Restaurant is planning to enter as the lessee into the two lease agreements

described below. Each lease is noncancelable, and Quan does not receive title to either leased property during or

at the end of the lease term. All payments required under these agreements are due on January 1 each year.

Present value factor at 10% (of an annuity due)

6.76

2.74

(CMA adapted, Dec 93 #28) Refer to the Quan Restaurant example. Quan Restaurant should treat the lease agreement with Cutter Electronics as

114. On January 1, Year 1, Lamp Company acquires new equipment in exchange for a note. Lamp must pay a

lump sum of $32,000 on December 31, Year 3. The equipment is being specifically manufactured for Lamp, so

no market price exists for the equipment. On similar types of equipment purchases, Lamp has paid 15% interest.

The equipment has a five-year life and the company uses straight-line depreciation with a 10% salvage value.

Required:

Prepare journal entries to record the following:

a.

original acquisition of equipment

b.

any adjusting journal entry necessary at December 31, Year 1

c.

entry to record depreciation at December 31, Year 2

d.

entry to record payment on December 31, Year 3

115. On January 1, Year 6, Pearson Corporation issued $1,000,000 face value, 20-year bonds. The bonds carry

coupon interest of 6 percent per year, payable semiannually on June 30 and December 31. The bonds were

initially priced on the market to yield 8 percent, compounded semiannually (for an effective annualized yield

greater than 8 percent).

Required:

a.

Compute the issue price of these bonds on January 1, Year 6.

b.

Compute the amount of interest expense on these bonds for Year 6, assuming that the firm uses the effective-interest method of amortizing

bond premium or discount.

c.

Assume for this part that the firm recorded interest expense in Part b. in an amount equal to interest paid for the year. That is, it failed to

record amortization of bond premium or discount. Indicate the effect (direction and amount) of this omission on the line items in the

statement of cash flows using "O/S" (overstated), "U/S" (understated), or "No" (no effect). Ignore income taxes.

Direction

Amount

1)

Net Income

2)

Adjustments that are added to net income

b.

First 6

0.04 ´ $802,073

$

116. Rotor Corporation issues $10,000,000 face value, 10-year, 6% semiannual coupon bonds

on January 1, 2013. The bonds require coupon payments on June 30 and December 31 of

each year. The market initially priced the bonds to yield 6% compounded semiannually.

The current market yield on these bonds was 6.2% compounded semiannually on June 30,

2013, and 6.6% compounded semiannually on December 31, 2008. Rotor Corporation

computes interest expense for each six-month period using the market yield at the beginning

of the period.

Required:

a. Compute the carrying value of these bonds on January 1, June 30, and December 31

of 2013, using the fair value option. You may interpolate in the interest tables or use a

calculator or use a spreadsheet program to compute the compound interest factors not

provided in the tables.

b. Compute the total amount of interest expense and unrealized gain or loss for the first

six months of 2013. Do not attempt to separate this amount into interest expense and

holding gain or loss.

c. Compute the total amount of interest expense and unrealized gain or loss for the second

six months of 2013. Do not attempt to separate this amount into interest expense and

holding gain or loss.

117. Indicate whether each of the following independent transactions is a capital (C) or operating (O) lease.

a.

__________ A firm signs a 5-year lease for equipment with a 7-year life.

b.

__________ A firm signs a lease for property with a fair market value of $20,000. The present value of the lease payments is $16,000.

c.

__________ A firm signs a lease for equipment which will allow the lessee to purchase the equipment at the end of the lease for

one-half the fair market value.

d.

__________ A firm signs a 16-year lease for equipment with a 20-year life.

e.

__________ A firm signs a lease for property with a fair value of $90,000. The present value of the lease payments is $85,000.

118. The annual report of Sign Corporation for Year 1 reports capital leases requiring payments totaling $228

million over future years, including $58 million payable at the end of Year 2. The interest rate on these

obligations is 12 percent and their present value (discounted at 12 percent) at the end of Year 1 was $181

million. The assets financed by capital leases appear on the Year 1 year-end balance sheet at $220 million.

Assume no new leases were entered into during Year 2 and that leasehold assets have a remaining useful life of

10 years at the start of Year 2, but no salvage value. Ignore income taxes.

Required:

a.

What would be the total expense for Year 2 for the leasehold assets and the financing thereof?

b.

What would be the total cash expenditure during Year 2 related to the leasehold assets and the financing thereof?

c.

What would be the balance sheet amount for leasehold assets at the end of Year 2?

d.

What would be the balance sheet amount for lease obligations at the end of Year 2?

119. ALT Company, as tenant, acquired for $600,000, paid in a single amount, the right to use an entire office

building for the next ten years. ALT expects to rent out the floors in the building to various commercial tenants.

As tenant, ALT accounts for its lease as a capital lease amortizing the leasehold asset on a straight-line basis

over ten years. ALT, as landlord, signed operating leases with the tenants for all of the rentable space. The rents

total $150,000 received at the end of each year for the next ten years, $1.5 million in total.

Required:

a.

Under current GAAP, can ALT treat the same property as a capital lease and an operating lease?

b.

What is the book value of this property after two years?

Assume, independent of your answer to the preceding question, that the book value of the property after two years is $400,000. On that

date, some of the tenants go bankrupt and ALT believes it will be unable to rent their now-vacant space, which will remain empty for the

remaining eight years. The fair market value of the remaining leasehold with still-solvent, rent-paying tenants is $300,000.

c.

If the remaining tenants will pay $800,000 in total, with present value $310,000, what entry, if any, will ALT make?

d.

If the remaining tenants will pay $320,000 in total, with present value $290,000, what entry, if any, will ALT make?

120. Bolton Co. leases workout equipment to health clubs. On January 1, Year 1, Bolton Co. leases to

Powerhouse Gym, equipment valued at $150,000, for 2 years. The equipment has a 12-year life with zero

salvage value. The lease payments equal $2,500 per year, payable on the last day of the year.

Required:

a.Identify the type of lease. Give reasons for your conclusion.

b.State the correct entries to be made by the lessor for this lease. You may assume straight-line depreciation is

used by Bolton.

a.Operating lease. The lease does not meet any of the criteria for a capital lease.

b.Lessor's entries:

12/31/Year 1:

Cash

2,500

121. Raines Corporation entered into a five-year lease for a computer on January 1, Year 3. The lease requires

Raines to make equal payments of $20,000 on January 1 each year for the five years of the lease, with the first

payment made on January 1, Year 3. Raines’ borrowing rate is 10 percent. Raines uses the straight-line

depreciation method for financial reporting. It estimates a zero salvage value. The accounting period is the

calendar year. Round amounts to the nearest dollar.

Required:

a.

Give the journal entries that Raines would make during Year 3 if this lease were considered an operating lease for financial reporting.

b.

Repeat [a] but assume the lease is a capital lease for financial reporting.

c.

Assume that this lease is considered a capital lease for financial reporting. Calculate depreciation expense for financial reporting purposes

for Year 3 and Year 4.

d.

Compute the total expenses (ignore income taxes) that Raines would recognize over the 5-year term of the lease, assuming it is an

operating lease.

e.

Repeat [d] but assume the lease is a capital lease.

a.

January 1, Year 3

Prepaid Rent

20,000

Cash

20,000

December 31, Year 3

Rent Expense

20,000

Prepaid Rent

20,000

b.

January 1, Year 3

Leased Asset

83,397

Lease Liability

63,397

122. The following information is available from the comparative balance sheets and related income statement

of the Horner Company for the year ended December 31, Year 7.

December 31,

December 31,

Year 6

Year 7

Present value of lease obligation

$2,040,508.60

$1,862,939.10

Leasehold (net of accumulated amortization)

$1,987,224.30

$1,766,421.60

Interest expense on lease obligation for Year 7

$ 122,430.52

123. Describe the sources of long-term debt financing.

SOURCES OF LONG-TERM DEBT FINANCING

1. Borrow from commercial banks, insurance companies, or other financial institutions.

2. Issue bonds in the capital markets.

Loans from commercial banks and other financial institutions often require firms to pledge assets as collateral.

For example, a firm borrowing to finance the acquisition of equipment would likely pledge the equipment as

collateral. If the firm fails to maintain specified levels of financial health while the loan is outstanding or does

not pay principal and interest on the loan when due, the lender has the right to seize the collateral and sell it to

satisfy the amounts due.

124. Consider a firm that recently issued bonds. Further, consider that the firm also set up a bond sinking fund.

Required:

a.

Why would a firm create a long-term liability?

b.

Why would a firm set up a bond sinking fund?

c.

If a firm paid $10,000 into its bond sinking fund at the end of the year, how would this transaction be journalized?

125. Part 1: Briefly explain a bond contract and its relationship to cash flows.

1. The bond contract specifies the basis for computing all future cash flows for that bond issue. Identifying

2. Terminology with respect to bonds includes the following:

126. How are bonds measured at issuance?

1. The promised cash payments indicated in the bond contract.

2. The yield to maturity required by investors to induce them to purchase the bonds.

When the coupon rate equals the historical market interest rate or initial yield to maturity, then the initial issue

price equals the face value of the bonds. An initial issue price equal to the face value of the bonds means that

the implicit interest rate equals the yield to maturity.

127. Describe what bond provisions exist.

BOND PROVISIONS

128. What are the cash flows patterns related to bonds?

129. When a company issues bonds, it must sometimes issue them at a discount, while at other times it will

issue them at a premium.

130. What are the general principles for measuring financial instruments?

1. The amount borrowed initially and the market value of a note or bond at any date subsequent to the initial

2. The internal rate of return, often called yield to maturity, is the discount rate that equates the future cash

1. Amortized Cost

2. Fair Value

131. How are notes valued and accounted for under the authoritative guidance?

1. The note, bond, or other financial instrument will appear on the balance sheet both initially and at each

2. The amount of interest expense each period equals the historical market interest rate times the carrying value

of the financial instrument at the beginning of each period.

132. What are the requirements for the disclosure of the carrying and fair values of debt?

133. Discuss the fair value option in accounting for certain assets and liabilities.

FAIR VALUE OPTION

2. Level 2: Observable inputs other than quoted market prices within Level 1. The category might include

3. Level 3: Unobservable inputs reflecting the reporting entity’s own assumptions about the assumptions

market participants would use in pricing an asset or settling a liability.

inputs.14

134. Describe the various methodologies in accounting for leases.

ACCOUNTING FOR LEASES

135. Describe the effect of the operating and capital lease methods on the financial statements of the lessee.

EFFECT OF THE OPERATING AND CAPITAL LEASE METHODS ON THE FINANCIAL STATEMENTS

OF THE LESSEE

136. What factors enter into choosing the accounting method for leases under U.S. GAAP and IFRS?

1. The lease transfers ownership of the leased asset to the lessee at the end of the lease term.

2. Transfer of ownership at the end of the lease term seems likely because the lessee has a bargain purchase

3. The lease extends for at least 75% of the asset’s expected useful life.

4. The present value of the contractual minimum lease payments equals or exceeds 90% of the fair value of the

asset at the time the lessee signs the lease. The present value computation uses a discount rate appropriate for

the creditworthiness of the lessee.

These criteria attempt to identify who enjoys the benefits and bears the economic risks of the leased property. If

the leased asset, either automatically or for a bargain price, becomes the property of the lessee at the end of the

lease period, then the lessee enjoys all of the economic benefits of the asset and incurs all risks of ownership. If

the life of the lease extends for most of the expected useful life of the asset (U.S. GAAP specifies 75% or

more), then the lessee enjoys most of the benefits, particularly when we measure them in present values, and

incurs most of the risk of technological obsolescence.

Lessors and lessees can usually structure leasing contracts to avoid the first three conditions. Avoiding the

fourth condition is more difficult because it requires the lessor to bear more risk than it might desire. The fourth

condition compares the present value of the lessee’s contractual minimum lease payments with the fair value of

the leased asset at the time the lessee signs the lease. The lessor presumably could either sell the asset for its fair

value or lease it to the lessee for a set of lease payments. The present value of the minimum lease payments has

the economic character of a loan in that the lessee has committed to make payments just as it would commit to

make payments on a loan with a bank. When the present value of the contractual minimum lease payments

equals at least 90% of the amount that the lessor would receive if it sold the asset instead of leasing it, then the

lessor receives most of its return from the leasing arrangement. That is, 90% of the fair value of the asset is not

at risk, and the lessor need receive only 10% of the fair value of the asset at the inception of the lease from

selling or releasing the asset at the end of the lease term.

Under these conditions, the fourth criterion views the lessee as enjoying most of the rewards and bearing most

of the risk of ownership, and the lease therefore qualifies as a capital lease. If, on the other hand, the lessor has

more than 10% of the asset’s initial fair value at risk, then the criterion views the lessor as enjoying most of the

benefits and bearing most of the risks of ownership and would classify the lease as an operating lease. This

fourth criterion has presented the most difficulties in practice because small changes in the amount or timing of

lease payments can shift the present value of the lease payments to just below or just above the 90% threshold.

IFRS Criteria for Lease Accounting

IFRS uses the same general criterion for classifying leases: Which party to the lease enjoys the rewards and

1. Does ownership transfer from the lessor to the lessee at the end of the lease?

2. Is there a bargain purchase option?

3. Does the lease extend for the major part of the asset’s economic life?

4. Does the present value of the minimum lease payments equal substantially all of the asset’s fair value?

5. Is the leased asset specialized for use by the lessee?

137. How does a lessor account for leases?

138. What are the effect of the operating and capital lease methods on the financial statements of the lessor?

139. What disclosures are required for leases?