Chapter 14: Intercorporate Investments in Common Stock

Student: ___________________________________________________________________________

1. The accounting for investments in common stock depends on (1) the expected holding period, and (2) the

2. Securities that firms expect to sell within the next year appear as investment securities in current assets on the

3. Securities that firms expect to hold for more than one year from the date of the balance sheet appear in

4. U.S. GAAP and IFRS view investments of between 20% and 50% of the voting stock of another company as

5. U.S. GAAP and IFRS view investments of less than 20% of the voting shares of another company as

6. U.S. GAAP and IFRS view ownership of more than 50% of an investee as implying an ability to control the

7. The rationale for the equity method is that it better measures an investor’s income from investing activities

when, because of its ownership interest, it can exert significant influence over the operations and dividend

8. For various reasons, a single economic entity may exist in the form of a parent and several legally separate

9. A major mining company owns a mining subsidiary in South America, where the government enforces

stringent control over cash payments outside the country. The parent cannot control all the assets of the

subsidiary, despite owning a majority of the voting shares, but should prepare consolidated statements with the

10. In the acquisition method for a business combination, the excess of the fair value of the consideration over

11. The summary of significant accounting principles, a required part of the financial statement notes, must

include a statement about the parent’s consolidation policy. If an investor does not consolidate a significant

12. If an entity qualifies as a variable interest entity (VIE), U.S. GAAP requires the primary beneficiary of the

14. If the combined market value of trading securities at the end of the year is less than the market value of the

19. When an investor owns less than a majority of the voting stock of another corporation, the accountant must

judge when the investor can exert significant influence. For the sake of uniformity, U.S. GAAP and IFRS

presume that significant influence exists at ownership of _____ or more of the voting stock of the

20. U.S. GAAP and IFRS require firms to account for minority, active investments, generally those where the

investor owns between _____ using the equity method. Under the equity method, the investor recognizes as

revenue (expense) each period its share of the net income (loss) of the investee. The investor recognizes

21. Under the equity method, the investor recognizes as revenue (expense) each period _____. The investor

23. The rationale for the equity method is that it better measures an investor’s income from investing activities

26. The equity method records the initial purchase of an investment in voting common stock at _____. Each

period, the investor treats as revenue its share of the _____ of the investee. The investor treats dividends

27. Marcoff Corporation acquires 30% of the outstanding voting common shares of the Invicta Corporation for

$600,000. Marcoff Corporation acquires the investment in Invicta Corporation by buying previously issued

shares of Invicta Corporation from other investors.

28. Penney Corporation acquires 30% of the outstanding voting common shares of the Instat Corporation for

$600,000. Penney Corporation acquires the investment in Instat Corporation by buying previously issued shares

of Instat Corporation from other investors.

Between the time of the acquisition and the end of Penney Corporation’s next accounting period, Instat

29. Marcoff Corporation acquires 30% of the outstanding voting common shares of the Invicta Corporation for

$600,000. Marcoff Corporation acquires the investment in Invicta Corporation by buying previously issued

shares of Invicta Corporation from other investors.

If Invicta Corporation declares and pays a dividend of $30,000 to holders of its common stock, Marcoff

30. Power Corporation acquires 30% of the outstanding voting common shares of the Inroad Corporation for

$600,000. Power Corporation acquires the investment in Inroad Corporation by buying previously issued shares

of Inroad Corporation from other investors.

Power Corporation records income earned by Inroad Corporation as a(n) _____, while the dividend _____,

31. Pager Corporation acquires 30% of the outstanding voting common shares of the Intercomm Corporation for

$600,000. Pager Corporation acquires the investment in Intercomm Corporation by buying previously issued

shares of Intercomm Corporation from other investors.

Suppose that Intercomm Corporation reports earnings of $100,000 and pays dividends of $40,000, during the

32. Pagoli Corporation acquires 30% of the outstanding voting common shares of the Inform Corporation for

$600,000. Pagoli Corporation acquires the investment in Inform Corporation by buying previously issued shares

of Inform Corporation from other investors.

Between the time of the acquisition and the end of Pagoli Corporation’s next accounting period, Inform

Corporation reports earnings of $80,000; and pays a dividend of $30,000 to holders of its common stock.

Inform Corporation reports earnings of $100,000 and pays dividends of $40,000 during the subsequent

accounting period.

33. acker Corporation acquires 30% of the outstanding voting common shares of the Insight Corporation for

$600,000. Packer Corporation acquires the investment in Insight Corporation by buying previously issued

shares of Insight Corporation from other investors.

Between the time of the acquisition and the end of Packer Corporation’s next accounting period, Insight

Corporation reports earnings of $80,000; and pays a dividend of $30,000 to holders of its common stock.

Insight Corporation reports earnings of $100,000 and pays dividends of $40,000 during the subsequent

accounting period.

Assume now that Packer Corporation sells one-fourth of its investment in Insight Corporation for $165,000.

34. Potion Corporation acquires 30% of the outstanding voting common shares of the Formula Corporation for

$600,000. Potion Corporation acquires the investment in Formula Corporation by buying previously issued

shares of Formula Corporation from other investors.

Between the time of the acquisition and the end of Potion Corporation’s next accounting period, Formula

Corporation reports earnings of $80,000; and pays a dividend of $30,000 to holders of its common stock.

Formula Corporation reports earnings of $100,000 and pays dividends of $40,000 during the subsequent

accounting period.

During the next accounting period, Potion Corporation sells one-fourth of its investment in Formula

Corporation for $165,000.

35. Parton Corporation acquires 30% of the outstanding voting common shares of the Investee Corporation for

$600,000. Parton Corporation acquires the investment in Import Corporation by buying previously issued shares

of Import Corporation from other investors.

When Parton Corporation acquired 30% of Import Corporation’s common shares for $600,000, Import

Corporation’s total shareholders’ equity was $1.5 million. Parton Corporation’s cost exceeds the carrying value

of the net assets acquired by $150,000 [ $600,000 - (0.30 x $1,500,000)]. Parton Corporation may pay this

36. Purchaser Corporation acquires 30% of the outstanding voting common shares of the Investee Corporation

for $600,000. Purchaser Corporation acquires the investment in Investee Corporation by buying previously

issued shares of Investee Corporation from other investors.

When Purchaser Corporation acquired 30% of Investee Corporation’s common shares for $600,000, Investee

Corporation’s total shareholders’ equity was $1.5 million. Purchaser Corporation’s cost exceeds the carrying

value of the net assets acquired by $150,000 [ $600,000 - (0.30 x $1,500,000)]. What is/are the accounting

37. Purchaser Corporation acquires 30% of the outstanding voting common shares of the Investee Corporation

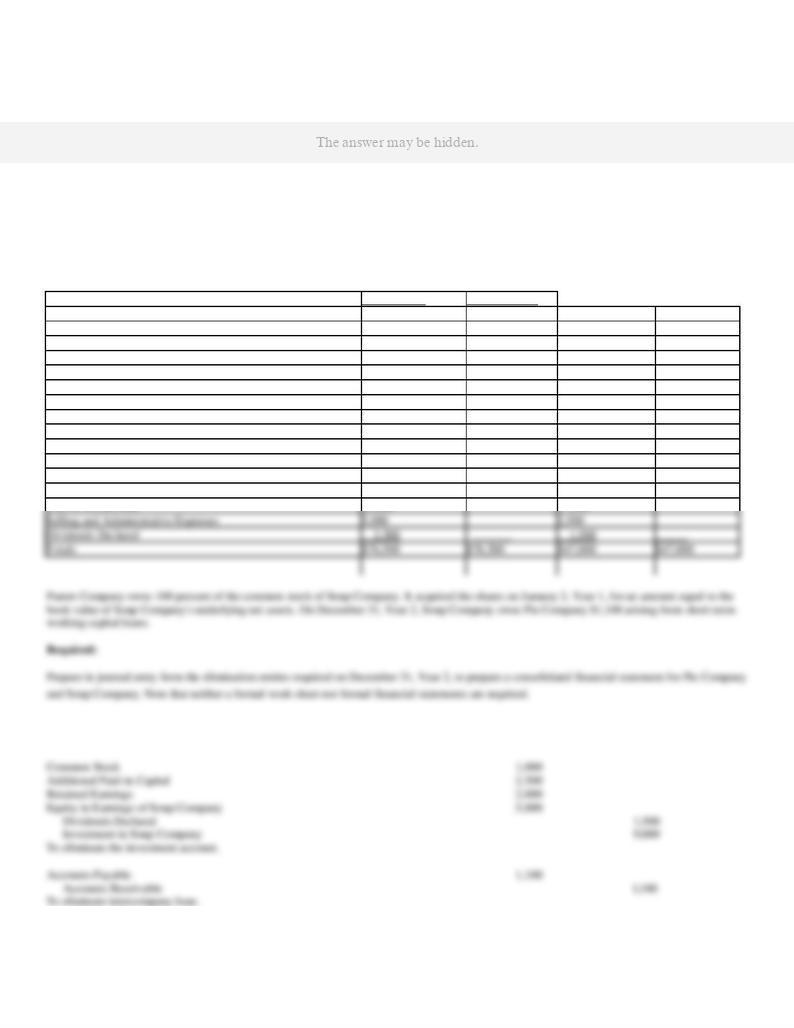

for $600,000. Purchaser Corporation acquires the investment in Investee Corporation by buying previously

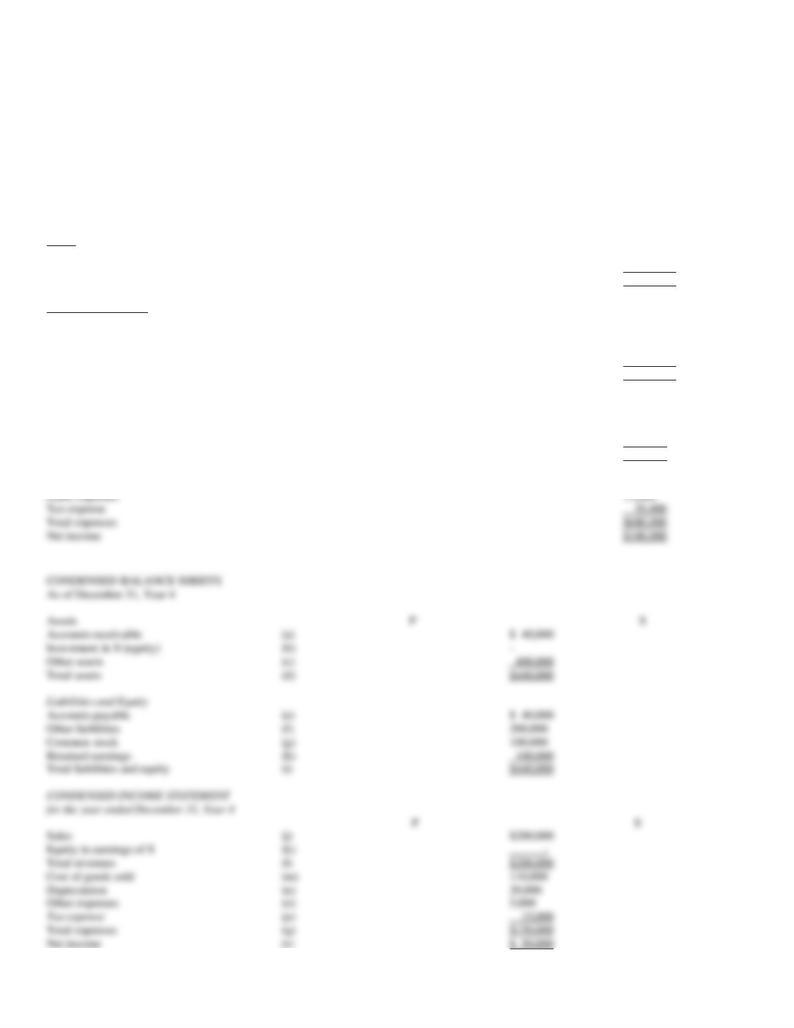

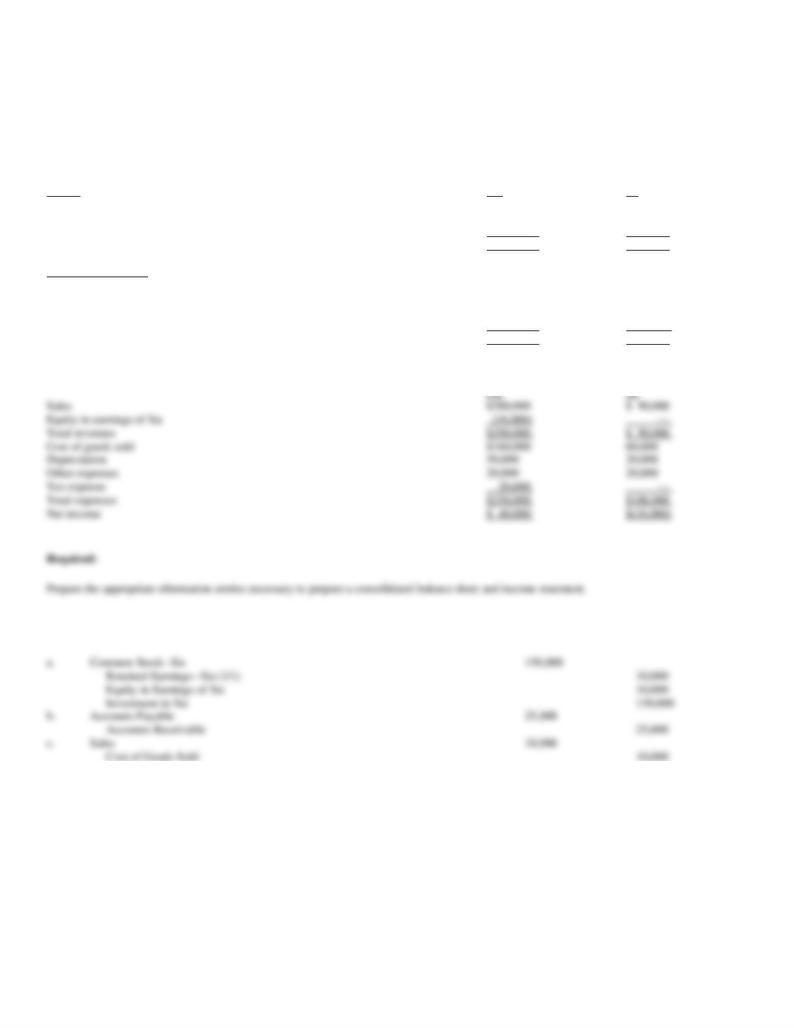

issued shares of Investee Corporation from other investors. When Purchaser Corporation acquired 30% of

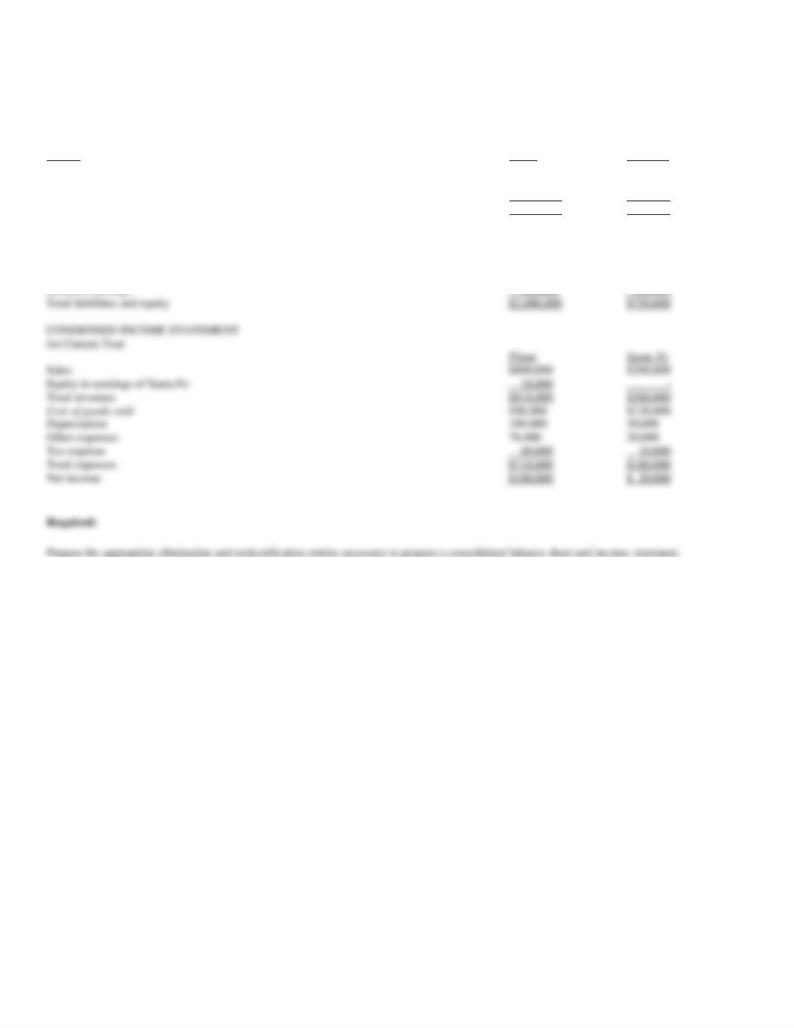

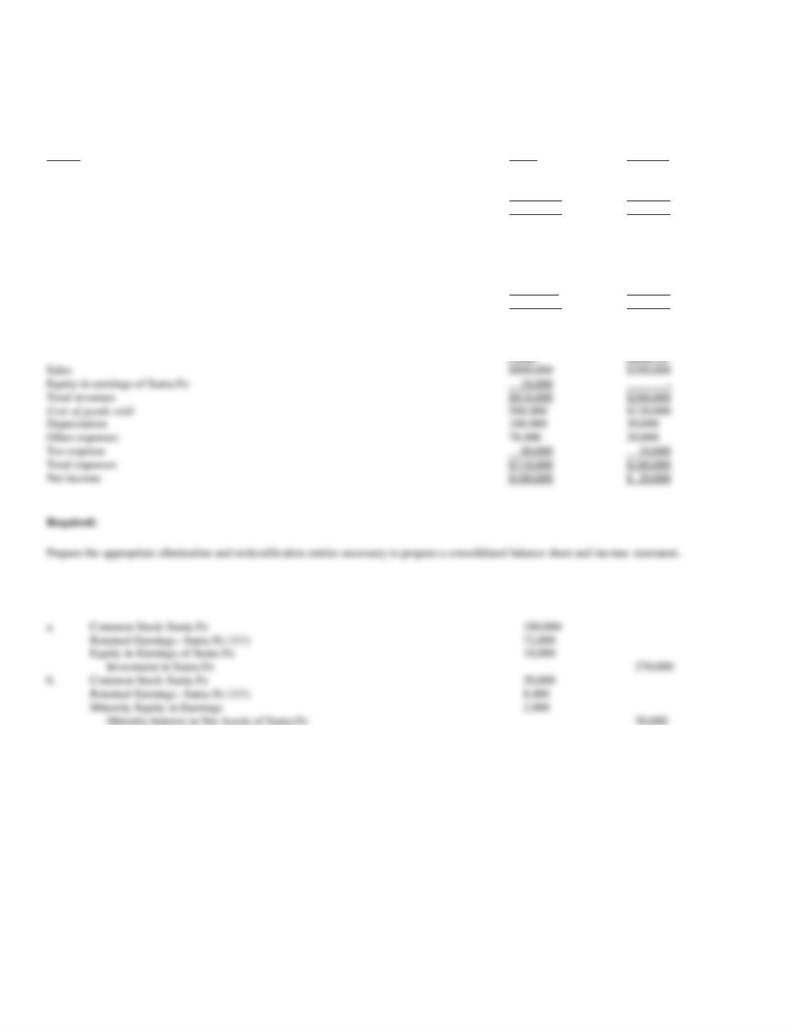

Investee Corporation’s common shares for $600,000, Investee Corporation’s total shareholders’ equity was $1.5

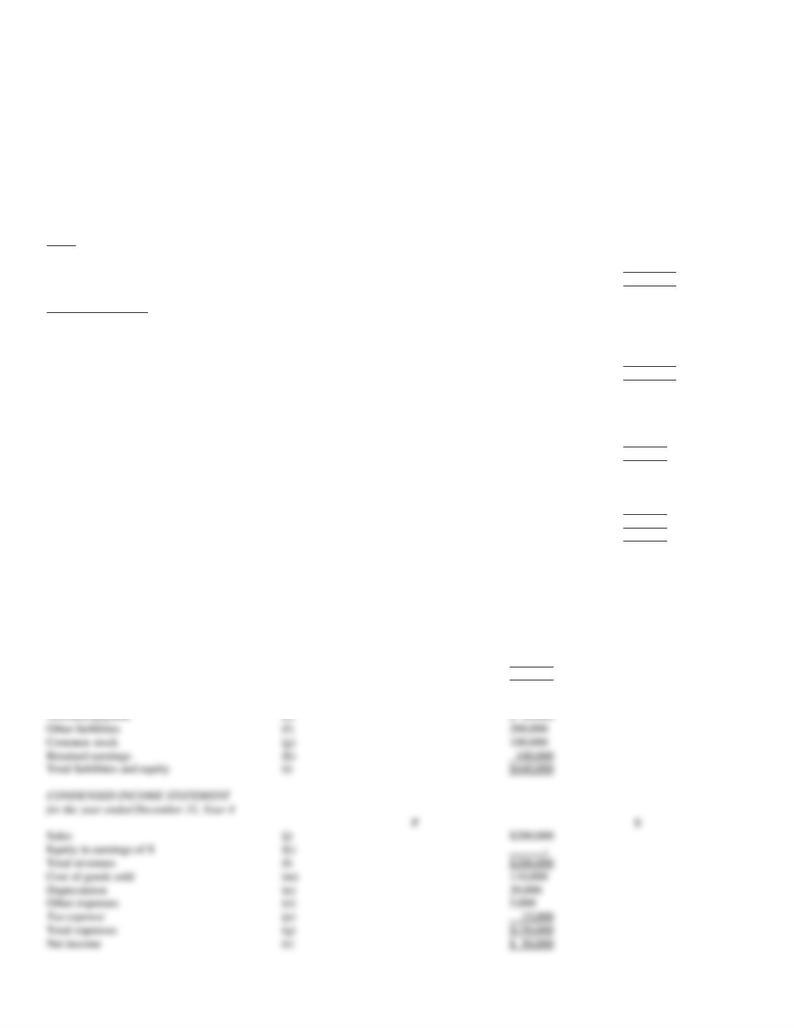

million. Purchaser Corporation’s cost exceeds the carrying value of the net assets acquired by $150,000 [

$600,000 - (0.30 x $1,500,000)].

Purchaser Corporation attributes the $150,000 excess purchase price as follows: $100,000 to remeasure

38. Purchaser Corporation acquires 30% of the outstanding voting common shares of the Investee Corporation

for $600,000. Purchaser Corporation acquires the investment in Investee Corporation by buying previously

issued shares of Investee Corporation from other investors.

Investee Corporation’s other comprehensive income during the first period is as follows:

Unrealized Holding Gains from Marketable Securities. . .$ 3,000

Unrealized Losses from Cash Flow Hedges . . . . . . . . . . (2,000)

Other Comprehensive Income. . . . . . . . . . . . . . . . . . . . $ 1,000

Purchaser Corporation would make the following entry to recognize its share of the items of other

39. Purchaser Corporation acquires 30% of the outstanding voting common shares of the Investee Corporation

for $600,000. Purchaser Corporation acquires the investment in Investee Corporation by buying previously

issued shares of Investee Corporation from other investors.

41. In Year 2, ABC Corp. acquired a 15% interest in XYZ, Inc., for $50,000. During the year, XYZ paid

dividends of $10,000 and had net income of $30,000. ABC sold the shares of XYZ for $65,000 cash. What

43. If Barton Company purchases a minority active interest in Laramie Company for $150,000, Barton will

44. Pareto Corporation owns 40% of Spring Corporation. During Year 3, Spring has net income of $60,000.

45. If Wabasso Company pays $55,000 in dividends to its corporate investor Lament Corporation (Lament

owns 35% of The Wabasso Company), what entry should Lament Corporation record when it receives the

46. InvestCo purchases 30% of NewCo's stock on January 1, Year 1, for $100,000. In Year 1, NewCo paid total

dividends of $30,000 and had a net income of $70,000. In Year 2, NewCo suffered a loss of $20,000 and paid

no dividends. On January 1, Year 3, InvestCo sells its investment in NewCo for $105,000. How is the sale

47. Pense Co. purchased 40% of the stock of Stretch Co. in Year 1 for $100,000. Stretch had net income in Year

1 of $50,000 and net income in Year 2 of $30,000. Stretch also paid total dividends of $20,000 in Year 2. On

January 1, Year 3, Pense Co. sold its investment in Stretch Co. to GE Capital Corporation (GE) for $130,000.

48. For which type of investments would unrealized increases and decreases be recorded directly in an owners'

49. The equity method of accounting for an investment in the common stock of another company should be

50. When an investor uses the equity method to account for investments in common stock, cash dividends

51. Park Inc. owns 35 percent of Exeter Corporation. During the calendar year 2013, Exeter had net earnings of

$300,000 and paid dividends of $36,000. Park mistakenly accounted for the investment in Exeter using the cost

method rather than the equity method of accounting. What effect would this have on the investment account and

52. U.S. GAAP view investments of between 20 and 50 percent of the voting stock of another company (unless

56. Business firms have several reasons for preferring to operate as a group of legally separate corporations,

rather than as a single entity. From the standpoint of the parent company, the more important reasons for

57. For various reasons, a single economic entity may exist in the form of a parent and several legally separate

64. (CMA adapted, Dec 92 #9) In a business combination that is accounted for as a purchase and does not

create negative goodwill, the assets of the acquired company are to be recorded on the books of the acquiring

69. Which of the following investments in securities would require the preparation of consolidated financial

70. U.S. GAAP view investments of over 50 percent of the voting stock of another company (for the purpose of

71. Often, the parent does not own 100% of the voting stock of a consolidated subsidiary. The parent refers to

73. The usual criterion for preparing consolidated financial statements is voting control in the form of majority

ownership of common stock. However, for some entities common stock ownership does not indicate control

because the common stock of the entity lacks one or more of the economic characteristics associated with

74. The usual criterion for preparing consolidated financial statements is voting control in the form of majority

ownership of common stock. However, for some entities common stock ownership does not indicate control

because the common stock of the entity lacks one or more of the economic characteristics associated with

76. Marley Company had the following portfolio of securities at the end of its first year of operations:

Year-End

Security

Classification

Cost

Market Value

A

Trading

$18,000

$23,000

B

Trading

$25,000

$27,000

77. What role does management intent play in the accounting treatment of marketable equity securities?

78. In 2013, Kentucky Inc. purchased stock as follows:

(a)

Acquired 2,000 shares of Gallen Corp. common stock (par value $20) in exchange for 1,200 shares of Kentucky Inc.

preferred stock (par value $30). The preferred stock had a market value of $75 per share on the date of the exchange.

(b)

Purchased 800 shares of Carlton Corp. common stock (par value $10) at $70 per share, plus a brokerage fee of $800.

79. Why would a firm choose to acquire less than 50 percent of an organization yet not desire to exercise

significant influence within the organization?

80. Assume that P uses the equity method of accounting for its investment in S. Solve for the unknown in each

of the following independent cases:

CASE A

CASE B

CASE C

P's ownership of S

A

30%

40%

Investment in beginning of year

$100

B

$130

Investment in end of year

105

$128

C

S's income (loss)

100

90

40

S's dividends paid

80

30

20

81. The Flavor Company owns 25 percent of the shares of Mac, and accounts for its investment using the equity

method. During the year Mac earned income of $1,500 million and declared dividends. Flavor’s share of the

dividends were $150.0 million.

Required:

82. Assume that P uses the equity method of accounting for its investment in S. Solve for the unknown in each

of the following independent cases:

84. The Canada Corporation has been using the equity method for its 100-percent owned subsidiary, Trenton

Company, which has both assets and liabilities on its balance sheet and both revenues and expenses on its

income statement. Trenton has positive cash flow from operations. Canada now consolidates the accounts of the

Trenton Company, which it has owned 100 percent since organizing it. Trenton has no investments of its own

and regularly declares dividends greater than zero, but less than net income.

Required:

Answer the following questions with one of these: larger, smaller, unchanged, or insufficient (information given

to answer question).

85. The adjusted, preclosing trial balances of Pie Company and Soup Company on December 31, Year 2, appear

below.

Pie Company

Soup Company

$ 4,000

$ 1,000

Accounts Receivable

Merchandise Inventory

10,000

10,000

Investment in Soup Company

9,000

--

Land

l,000

2,000

Buildings and Equipment, net

5,000

Accounts Payable

$17,500

$12,500

Bonds Payable

5,000

4,000

Common Stock

2,500

1,000

86. Piu Co. owns 100% of Xu Co. Piu has owned Xu since Xu was incorporated. At December 31, $15,000 of

Xu’s accounts receivable represent amounts payable by Piu. $10,000 of Piu’s accounts receivable represent

amounts payable by Xu. During the current year, Xu sold $10,000 in merchandise to Piu (at cost its cost of

$10,000). Piu has sold all the merchandise purchased from Xu.

CONDENSED BALANCE SHEETS

As of December 31

Assets

Piu

Xu

Accounts receivable

$ 60,000

$ 40,000

Investment in Xu (equity)

130,000

-

Other assets

1,000,000

200,000

Total assets

$1,190,000

$240,000

Liabilities and Equity

Accounts payable

$ 50,000

$ 20,000

Other liabilities

640,000

90,000

Common stock

100,000

150,000

87. On January 1, Year 1, Plano Co. purchased for $180,000, 90% of Santa Fe Co. at a time when Santa Fe had

a book value of $200,000. There were no intercompany transactions during year 4.

CONDENSED BALANCE SHEETS

As of December 31, Year 4

Assets

Plano

Santa Fe

Accounts receivable

$ 50,000

$ 40,000

Investment in Santa Fe (equity)

270,000

-

Other assets

1,680,000

710,000

Total assets

$2,000,000

$750,000

Liabilities and Equity

Accounts payable

$ 40,000

$ 50,000

Other liabilities

1,360,000

400,000

Common stock

200,000

200,000

88. Given the following separate company balance sheets and income statements, answer the following

questions.

CONDENSED BALANCE SHEETS

As of December 31, Year 4

Assets

Plea

Settle

Accounts receivable

$ 50,000

$ 40,000

Investment in Settle (equity)

300,000

-

Other assets

1,680,000

710,000

Total assets

$2,030,000

$750,000

Liabilities and Equity

Accounts payable

$ 70,000

$ 50,000

Other liabilities

1,360,000

400,000

Common stock

200,000

200,000

Retained earnings

400,000

100,000

Total liabilities and equity

$2,030,000

$750,000

CONDENSED INCOME STATEMENT

for the year ended December 31, Year 4

89. Given the following consolidated balance sheet and additional information, prepare a separate company

balance sheet and income statement for P.

-

P owns 100% of S.

-

S sold $20,000 of inventory to P.

-

P sold all of the inventory it purchased from S.

-

$10,000 of S's accounts receivable are payable by P.

CONSOLIDATED BALANCE SHEET

As of December 31, Year 4

Assets

Accounts receivable

$ 50,000

Other assets

1,680,000

Total assets

$1,730,000

Liabilities and Equity

Accounts payable

$ 80,000

Other liabilities

1,200,000

Common stock

50,000

Retained earnings

400,000

Total liabilities and equity

$1,730,000

CONSOLIDATED INCOME STATEMENT

for the year ended December 31, Year 4

Sales

$780,000

Total revenues

$780,000

Cost of goods sold

$490,000

Depreciation

120,000

90. Large, global enterprises typically have an equity interest in other entities throughout the world. Some of the

Company E

23.8%

Company F

20%

91. Parent Computer Corporation acquired significant influence over Child Computer Company on January 2

92. Describe the accounting and reporting of investments in common stock.

93. Describe the accounting for minority, active investments.

94. Why do accountants sometimes refer to the equity method as a one-line consolidation?

95. Discuss the accounting for majority, active investments.

96. Describe U.S. GAAP and IFRS requirements in accounting for the business combination.

97. Describe what a consolidated income statement shows.

98. What is a noncontrolling interest in a consolidated subsidiary?

99. Describe the limitations of consolidated statements.

100. Describe the U.S. GAAP requirement in accounting for joint venture investments.,

101. Variable interest entities have what characteristics?

102. What are qualifying special purpose entities?

103. On July 1, 2013, Mecca Group purchased for cash 35 percent of the outstanding capital stock of Wembley

Studios. Both Mecca Group and Wembley Studios have a December 31 year-end. Wembley Studios, whose

common stock is actively traded in the over-the-counter market, reported its total net income for the year

to Mecca Group and also paid cash dividends on November 15, 2013, to Mecca Group and its other

stockholders.

How should Mecca Group report the above facts in its December 31, 2013, balance sheet and its income

statement for the year then ended? Discuss the rationale for your answer.

104. The equity method of accounting should be applied by an investor to an investment in the voting stock of

Chapter 14: Intercorporate Investments in Common Stock Key

1. The accounting for investments in common stock depends on (1) the expected holding period, and (2) the

2. Securities that firms expect to sell within the next year appear as investment securities in current assets on the

3. Securities that firms expect to hold for more than one year from the date of the balance sheet appear in

4. U.S. GAAP and IFRS view investments of between 20% and 50% of the voting stock of another company as

5. U.S. GAAP and IFRS view investments of less than 20% of the voting shares of another company as

6. U.S. GAAP and IFRS view ownership of more than 50% of an investee as implying an ability to control the

7. The rationale for the equity method is that it better measures an investor’s income from investing activities

when, because of its ownership interest, it can exert significant influence over the operations and dividend

8. For various reasons, a single economic entity may exist in the form of a parent and several legally separate

9. A major mining company owns a mining subsidiary in South America, where the government enforces

stringent control over cash payments outside the country. The parent cannot control all the assets of the

subsidiary, despite owning a majority of the voting shares, but should prepare consolidated statements with the

10. In the acquisition method for a business combination, the excess of the fair value of the consideration over

11. The summary of significant accounting principles, a required part of the financial statement notes, must

include a statement about the parent’s consolidation policy. If an investor does not consolidate a significant

12. If an entity qualifies as a variable interest entity (VIE), U.S. GAAP requires the primary beneficiary of the

14. If the combined market value of trading securities at the end of the year is less than the market value of the

19. When an investor owns less than a majority of the voting stock of another corporation, the accountant must

judge when the investor can exert significant influence. For the sake of uniformity, U.S. GAAP and IFRS

presume that significant influence exists at ownership of _____ or more of the voting stock of the

20. U.S. GAAP and IFRS require firms to account for minority, active investments, generally those where the

investor owns between _____ using the equity method. Under the equity method, the investor recognizes as

revenue (expense) each period its share of the net income (loss) of the investee. The investor recognizes

21. Under the equity method, the investor recognizes as revenue (expense) each period _____. The investor

23. The rationale for the equity method is that it better measures an investor’s income from investing activities

26. The equity method records the initial purchase of an investment in voting common stock at _____. Each

period, the investor treats as revenue its share of the _____ of the investee. The investor treats dividends

27. Marcoff Corporation acquires 30% of the outstanding voting common shares of the Invicta Corporation for

$600,000. Marcoff Corporation acquires the investment in Invicta Corporation by buying previously issued

shares of Invicta Corporation from other investors.

28. Penney Corporation acquires 30% of the outstanding voting common shares of the Instat Corporation for

$600,000. Penney Corporation acquires the investment in Instat Corporation by buying previously issued shares

of Instat Corporation from other investors.

Between the time of the acquisition and the end of Penney Corporation’s next accounting period, Instat

29. Marcoff Corporation acquires 30% of the outstanding voting common shares of the Invicta Corporation for

$600,000. Marcoff Corporation acquires the investment in Invicta Corporation by buying previously issued

shares of Invicta Corporation from other investors.

If Invicta Corporation declares and pays a dividend of $30,000 to holders of its common stock, Marcoff

30. Power Corporation acquires 30% of the outstanding voting common shares of the Inroad Corporation for

$600,000. Power Corporation acquires the investment in Inroad Corporation by buying previously issued shares

of Inroad Corporation from other investors.

Power Corporation records income earned by Inroad Corporation as a(n) _____, while the dividend _____,

31. Pager Corporation acquires 30% of the outstanding voting common shares of the Intercomm Corporation for

$600,000. Pager Corporation acquires the investment in Intercomm Corporation by buying previously issued

shares of Intercomm Corporation from other investors.

Suppose that Intercomm Corporation reports earnings of $100,000 and pays dividends of $40,000, during the

32. Pagoli Corporation acquires 30% of the outstanding voting common shares of the Inform Corporation for

$600,000. Pagoli Corporation acquires the investment in Inform Corporation by buying previously issued shares

of Inform Corporation from other investors.

Between the time of the acquisition and the end of Pagoli Corporation’s next accounting period, Inform

Corporation reports earnings of $80,000; and pays a dividend of $30,000 to holders of its common stock.

Inform Corporation reports earnings of $100,000 and pays dividends of $40,000 during the subsequent

accounting period.

33. acker Corporation acquires 30% of the outstanding voting common shares of the Insight Corporation for

$600,000. Packer Corporation acquires the investment in Insight Corporation by buying previously issued

shares of Insight Corporation from other investors.

Between the time of the acquisition and the end of Packer Corporation’s next accounting period, Insight

Corporation reports earnings of $80,000; and pays a dividend of $30,000 to holders of its common stock.

Insight Corporation reports earnings of $100,000 and pays dividends of $40,000 during the subsequent

accounting period.

Assume now that Packer Corporation sells one-fourth of its investment in Insight Corporation for $165,000.

34. Potion Corporation acquires 30% of the outstanding voting common shares of the Formula Corporation for

$600,000. Potion Corporation acquires the investment in Formula Corporation by buying previously issued

shares of Formula Corporation from other investors.

Between the time of the acquisition and the end of Potion Corporation’s next accounting period, Formula

Corporation reports earnings of $80,000; and pays a dividend of $30,000 to holders of its common stock.

Formula Corporation reports earnings of $100,000 and pays dividends of $40,000 during the subsequent

accounting period.

During the next accounting period, Potion Corporation sells one-fourth of its investment in Formula

Corporation for $165,000.

35. Parton Corporation acquires 30% of the outstanding voting common shares of the Investee Corporation for

$600,000. Parton Corporation acquires the investment in Import Corporation by buying previously issued shares

of Import Corporation from other investors.

When Parton Corporation acquired 30% of Import Corporation’s common shares for $600,000, Import

Corporation’s total shareholders’ equity was $1.5 million. Parton Corporation’s cost exceeds the carrying value

of the net assets acquired by $150,000 [ $600,000 - (0.30 x $1,500,000)]. Parton Corporation may pay this

36. Purchaser Corporation acquires 30% of the outstanding voting common shares of the Investee Corporation

for $600,000. Purchaser Corporation acquires the investment in Investee Corporation by buying previously

issued shares of Investee Corporation from other investors.

When Purchaser Corporation acquired 30% of Investee Corporation’s common shares for $600,000, Investee

Corporation’s total shareholders’ equity was $1.5 million. Purchaser Corporation’s cost exceeds the carrying

value of the net assets acquired by $150,000 [ $600,000 - (0.30 x $1,500,000)]. What is/are the accounting

37. Purchaser Corporation acquires 30% of the outstanding voting common shares of the Investee Corporation

for $600,000. Purchaser Corporation acquires the investment in Investee Corporation by buying previously

issued shares of Investee Corporation from other investors. When Purchaser Corporation acquired 30% of

Investee Corporation’s common shares for $600,000, Investee Corporation’s total shareholders’ equity was $1.5

million. Purchaser Corporation’s cost exceeds the carrying value of the net assets acquired by $150,000 [

$600,000 - (0.30 x $1,500,000)].

Purchaser Corporation attributes the $150,000 excess purchase price as follows: $100,000 to remeasure

38. Purchaser Corporation acquires 30% of the outstanding voting common shares of the Investee Corporation

for $600,000. Purchaser Corporation acquires the investment in Investee Corporation by buying previously

issued shares of Investee Corporation from other investors.

Investee Corporation’s other comprehensive income during the first period is as follows:

Unrealized Holding Gains from Marketable Securities. . .$ 3,000

Unrealized Losses from Cash Flow Hedges . . . . . . . . . . (2,000)

Other Comprehensive Income. . . . . . . . . . . . . . . . . . . . $ 1,000

Purchaser Corporation would make the following entry to recognize its share of the items of other

39. Purchaser Corporation acquires 30% of the outstanding voting common shares of the Investee Corporation

for $600,000. Purchaser Corporation acquires the investment in Investee Corporation by buying previously

issued shares of Investee Corporation from other investors.

41. In Year 2, ABC Corp. acquired a 15% interest in XYZ, Inc., for $50,000. During the year, XYZ paid

dividends of $10,000 and had net income of $30,000. ABC sold the shares of XYZ for $65,000 cash. What

43. If Barton Company purchases a minority active interest in Laramie Company for $150,000, Barton will

44. Pareto Corporation owns 40% of Spring Corporation. During Year 3, Spring has net income of $60,000.

45. If Wabasso Company pays $55,000 in dividends to its corporate investor Lament Corporation (Lament

owns 35% of The Wabasso Company), what entry should Lament Corporation record when it receives the

46. InvestCo purchases 30% of NewCo's stock on January 1, Year 1, for $100,000. In Year 1, NewCo paid total

dividends of $30,000 and had a net income of $70,000. In Year 2, NewCo suffered a loss of $20,000 and paid

no dividends. On January 1, Year 3, InvestCo sells its investment in NewCo for $105,000. How is the sale

47. Pense Co. purchased 40% of the stock of Stretch Co. in Year 1 for $100,000. Stretch had net income in Year

1 of $50,000 and net income in Year 2 of $30,000. Stretch also paid total dividends of $20,000 in Year 2. On

January 1, Year 3, Pense Co. sold its investment in Stretch Co. to GE Capital Corporation (GE) for $130,000.

48. For which type of investments would unrealized increases and decreases be recorded directly in an owners'

49. The equity method of accounting for an investment in the common stock of another company should be

50. When an investor uses the equity method to account for investments in common stock, cash dividends

51. Park Inc. owns 35 percent of Exeter Corporation. During the calendar year 2013, Exeter had net earnings of

$300,000 and paid dividends of $36,000. Park mistakenly accounted for the investment in Exeter using the cost

method rather than the equity method of accounting. What effect would this have on the investment account and

52. U.S. GAAP view investments of between 20 and 50 percent of the voting stock of another company (unless

56. Business firms have several reasons for preferring to operate as a group of legally separate corporations,

rather than as a single entity. From the standpoint of the parent company, the more important reasons for

57. For various reasons, a single economic entity may exist in the form of a parent and several legally separate

64. (CMA adapted, Dec 92 #9) In a business combination that is accounted for as a purchase and does not

create negative goodwill, the assets of the acquired company are to be recorded on the books of the acquiring

69. Which of the following investments in securities would require the preparation of consolidated financial

70. U.S. GAAP view investments of over 50 percent of the voting stock of another company (for the purpose of

71. Often, the parent does not own 100% of the voting stock of a consolidated subsidiary. The parent refers to

73. The usual criterion for preparing consolidated financial statements is voting control in the form of majority

ownership of common stock. However, for some entities common stock ownership does not indicate control

because the common stock of the entity lacks one or more of the economic characteristics associated with

74. The usual criterion for preparing consolidated financial statements is voting control in the form of majority

ownership of common stock. However, for some entities common stock ownership does not indicate control

because the common stock of the entity lacks one or more of the economic characteristics associated with

75. Consolidated financial statements are typically prepared when one company has

A. accounted for its investment in another company by the equity method.

B. significant influence over the operating and financial policies of another company.

C. the controlling financial interest in another company.

D. a substantial equity interest in the net assets of another company.

E. All of these answer choices are correct.

76. Marley Company had the following portfolio of securities at the end of its first year of operations:

Year-End

Security

Classification

Cost

Market Value

A

Trading

$18,000

$23,000

B

Trading

$25,000

$27,000

77. What role does management intent play in the accounting treatment of marketable equity securities?

Management's intent determines whether marketable securities are held as trading securities or securities

available for sale. If the securities are held as trading securities, the income statement shows unrealized holding

gains/losses. If they are held as securities available for sale, other comprehensive income contains unrealized

holding gains/losses.

78. In 2013, Kentucky Inc. purchased stock as follows:

(a)

Acquired 2,000 shares of Gallen Corp. common stock (par value $20) in exchange for 1,200 shares of Kentucky Inc.

preferred stock (par value $30). The preferred stock had a market value of $75 per share on the date of the exchange.

(b)

Purchased 800 shares of Carlton Corp. common stock (par value $10) at $70 per share, plus a brokerage fee of $800.

79. Why would a firm choose to acquire less than 50 percent of an organization yet not desire to exercise

significant influence within the organization?

80. Assume that P uses the equity method of accounting for its investment in S. Solve for the unknown in each

of the following independent cases:

CASE A

CASE B

CASE C

P's ownership of S

A

30%

40%

Investment in beginning of year

$100

B

$130

Investment in end of year

105

$128

C

S's income (loss)

100

90

40

S's dividends paid

80

30

20

81. The Flavor Company owns 25 percent of the shares of Mac, and accounts for its investment using the equity

method. During the year Mac earned income of $1,500 million and declared dividends. Flavor’s share of the

dividends were $150.0 million.

Required:

a.

What amount of income did Flavor report from its investment in Mac?

b.

What amount of cash flow from operations did Flavor report for the year from its investment in Mac?

82. Assume that P uses the equity method of accounting for its investment in S. Solve for the unknown in each

of the following independent cases:

CASE A

CASE B

CASE C

P's ownership of S

40%

25%

40%

Investment in S--beginning of year

$100

$100

$130

Investment in S--end of year

$120

$150

$120

S's income (loss)

A

300

C

S's dividends paid

80

B

0

83. State the purpose of consolidated financial statements. Define which subsidiaries must be included in

consolidated financial statements.

84. The Canada Corporation has been using the equity method for its 100-percent owned subsidiary, Trenton

Company, which has both assets and liabilities on its balance sheet and both revenues and expenses on its

income statement. Trenton has positive cash flow from operations. Canada now consolidates the accounts of the

Trenton Company, which it has owned 100 percent since organizing it. Trenton has no investments of its own

and regularly declares dividends greater than zero, but less than net income.

Required:

Answer the following questions with one of these: larger, smaller, unchanged, or insufficient (information given

to answer question).

a.

What would be the effect on net income of Canada Corporation?

b.

What would be the effect on revenues, including investment income, of Canada Corporation?

c.

What would be the effect on investments of Canada Corporation?

d.

What would be the effect on assets of Canada Corporation?

e.

What would be the effect on liabilities of Canada Corporation?

f.

What would be the effect on the debt/equity ratio (= Liabilities/Total Equities)?

85. The adjusted, preclosing trial balances of Pie Company and Soup Company on December 31, Year 2, appear

below.

Pie Company

Soup Company

$ 4,000

$ 1,000

Accounts Receivable

Merchandise Inventory

10,000

10,000

Investment in Soup Company

9,000

--

Land

l,000

2,000

Buildings and Equipment, net

5,000

Accounts Payable

$17,500

$12,500

Bonds Payable

5,000

4,000

Common Stock

2,500

1,000

Additional Paid-in Capital

1,000

2,500

Retained Earnings, January 1

10,500

2,000

Sales

35,000

25,000

Equity in Earnings of Soup Company

5,000

--

Cost of Goods Sold

25,000

17,500

86. Piu Co. owns 100% of Xu Co. Piu has owned Xu since Xu was incorporated. At December 31, $15,000 of

Xu’s accounts receivable represent amounts payable by Piu. $10,000 of Piu’s accounts receivable represent

amounts payable by Xu. During the current year, Xu sold $10,000 in merchandise to Piu (at cost its cost of

$10,000). Piu has sold all the merchandise purchased from Xu.

CONDENSED BALANCE SHEETS

As of December 31

Assets

Piu

Xu

Accounts receivable

$ 60,000

$ 40,000

Investment in Xu (equity)

130,000

-

Other assets

1,000,000

200,000

Total assets

$1,190,000

$240,000

Liabilities and Equity

Accounts payable

$ 50,000

$ 20,000

Other liabilities

640,000

90,000

Common stock

100,000

150,000

Retained earnings

400,000

(20,000)

Total liabilities and equity

$1,190,000

$240,000

CONDENSED INCOME STATEMENT

for Current Year

87. On January 1, Year 1, Plano Co. purchased for $180,000, 90% of Santa Fe Co. at a time when Santa Fe had

a book value of $200,000. There were no intercompany transactions during year 4.

CONDENSED BALANCE SHEETS

As of December 31, Year 4

Assets

Plano

Santa Fe

Accounts receivable

$ 50,000

$ 40,000

Investment in Santa Fe (equity)

270,000

-

Other assets

1,680,000

710,000

Total assets

$2,000,000

$750,000

Liabilities and Equity

Accounts payable

$ 40,000

$ 50,000

Other liabilities

1,360,000

400,000

Common stock

200,000

200,000

Retained earnings

400,000

100,000

Total liabilities and equity

$2,000,000

$750,000

CONDENSED INCOME STATEMENT

for Current Year

88. Given the following separate company balance sheets and income statements, answer the following

questions.

CONDENSED BALANCE SHEETS

As of December 31, Year 4

Assets

Plea

Settle

Accounts receivable

$ 50,000

$ 40,000

Investment in Settle (equity)

300,000

-

Other assets

1,680,000

710,000

Total assets

$2,030,000

$750,000

Liabilities and Equity

Accounts payable

$ 70,000

$ 50,000

Other liabilities

1,360,000

400,000

Common stock

200,000

200,000

Retained earnings

400,000

100,000

Total liabilities and equity

$2,030,000

$750,000

CONDENSED INCOME STATEMENT

for the year ended December 31, Year 4

Plea

Settle

Sales

$800,000

$200,000

Equity in earnings of Settle

20,000

-

89. Given the following consolidated balance sheet and additional information, prepare a separate company

balance sheet and income statement for P.

-

P owns 100% of S.

-

S sold $20,000 of inventory to P.

-

P sold all of the inventory it purchased from S.

-

$10,000 of S's accounts receivable are payable by P.

CONSOLIDATED BALANCE SHEET

As of December 31, Year 4

Assets

Accounts receivable

$ 50,000

Other assets

1,680,000

Total assets

$1,730,000

Liabilities and Equity

Accounts payable

$ 80,000

Other liabilities

1,200,000

Common stock

50,000

Retained earnings

400,000

Total liabilities and equity

$1,730,000

CONSOLIDATED INCOME STATEMENT

for the year ended December 31, Year 4

Sales

$780,000

Total revenues

$780,000

Cost of goods sold

$490,000

Depreciation

120,000

Other expenses

15,000

Tax expense

55,000

Total expenses

$680,000

Net income

$100,000

CONDENSED BALANCE SHEETS

As of December 31, Year 4

Assets

P

S

Accounts receivable

(a)

$ 40,000

Investment in S (equity)

(b)

-

Other assets

(c)

400,000

Total assets

(d)

$440,000

Liabilities and Equity

90. Large, global enterprises typically have an equity interest in other entities throughout the world. Some of the

interests represent wholly-owned (100%-owned) subsidiaries, while others represent lesser percentages of

ownership. These large global conglomerates provide information on the percentage ownership of their various

affiliated companies in the notes to the consolidated financial statements.

The following list of companies represents the ownership percentage of selected companies by a large global

company:

Company A

50% plus

one share

Company B

100%

Company C

68%

Company D

50%

Company E

23.8%

Company F

20%

Required:

Explain how you would expect the global company holding the indicated interests to account for each of the companies listed above, based on the

percentage ownership reported.

Co

mp

an

y

A,

50

%

plu

s

on

e

sha

re,

wo

uld

be

co

ns

oli

dat

ed

Co

mp

an

y

B,

10

0%

,

wo

uld

be

co

ns

oli

dat

ed

Co

mp

an

y

C,

68

%,

wo

uld

be

co

ns

oli

dat

ed

Co

mp

an

y

D,

50

%,

wo

uld

not

be

co

ns

oli

dat

ed

23.

8%

,

wo

uld

not

be

co

ns

oli

dat

ed

Co

mp

an

y

F,

20

%,

wo

uld

not

be

co

ns

oli

dat

ed

Co

mp

ani

es

D

an

d E

wo

uld

be

acc

ou

nte

d

for

usi

91. Parent Computer Corporation acquired significant influence over Child Computer Company on January 2

by purchasing 20 percent of its outstanding stock for $100 million. Parent attributes the entire excess of cost

over book value acquired to a patent, which it amortizes over 10 years. Child Computer had earnings of $100

million and declared dividends of $30 million during the year. The accounts receivable of Parent Computer

Corporation at December 31 included $600,000 due from Child Computer. Parent Computer Corporation

accounts for its investment in Child Computer using the equity method. Parent Computer Corporation considers

reducing its ownership from 20 percent to 19.5 percent so that it no longer has to use the equity method.

Comment on the ethical implications of this possibility.

Ethical issues confront Parent Computer Corporation’s management when they make financial reporting

decisions. Among the questions that one might raise are: (1)does the action violate a known law or regulation

and (2) has the firm provided sufficient disclosure about the action for the users of financial statements to make

92. Describe the accounting and reporting of investments in common stock.

1. In minority, passive investments, an investor acquires the common stock of another entity (the investee) for

2. In minority, active investments, an investor acquires common shares of an investee with

3. In majority, active investments, an investor acquires shares of an investee so that the investor can control the

93. Describe the accounting for minority, active investments.

MINORITY, ACTIVE INVESTMENTS

P’s investment in S represents a proportionate share of the shareholders’ equity of S. P may pay more than the

94. Why do accountants sometimes refer to the equity method as a one-line consolidation?

95. Discuss the accounting for majority, active investments.

MAJORITY, ACTIVE INVESTMENTS

1. To reduce the parent’s legal or operational risk.

2. To reduce the costs of dealing with jurisdiction-specific differences in corporate laws and tax rules.

3. To expand or diversify.

4. To reduce the costs of divesting assets.

Firms generally save costs if they sell the common stock of a subsidiary rather than trying to sell each of its

assets separately. In addition, a sale of shares transfers all known and, perhaps, unknown liabilities to a buyer.

Consolidated financial statements also provide more helpful information than does the equity method, because

96. Describe U.S. GAAP and IFRS requirements in accounting for the business combination.

THE PURCHASE TRANSACTION

1. Acquires the assets and assumes the liabilities of another corporation, or

2. Acquires all, or a majority, of another corporation’s common shares and thereby acquires

a controlling interest in the net assets of the other corporation.

1. Measure the identifiable tangible and intangible assets and liabilities of the acquired

2. The acquirer compares the fair value of the cash, common stock, or other consideration

97. Describe what a consolidated income statement shows.

98. What is a noncontrolling interest in a consolidated subsidiary?

99. Describe the limitations of consolidated statements.

100. Describe the U.S. GAAP requirement in accounting for joint venture investments.,

JOINT VENTURE INVESTMENTS

101. Variable interest entities have what characteristics?

2. The equity owners lack meaningful decision rights.

102. What are qualifying special purpose entities?

103. On July 1, 2013, Mecca Group purchased for cash 35 percent of the outstanding capital stock of Wembley

Studios. Both Mecca Group and Wembley Studios have a December 31 year-end. Wembley Studios, whose

common stock is actively traded in the over-the-counter market, reported its total net income for the year

to Mecca Group and also paid cash dividends on November 15, 2013, to Mecca Group and its other

stockholders.

How should Mecca Group report the above facts in its December 31, 2013, balance sheet and its income

statement for the year then ended? Discuss the rationale for your answer.

2013.

104. The equity method of accounting should be applied by an investor to an investment in the voting stock of

1.

Investor representation of the board of directors of the investee.

2.

Investor participation in policy making processes.

3.

Material intercompany transactions between the investor and investee companies.

4.

Interchange of investor and investee managerial personnel.

5.

Technological dependency of one entity on the other.

6.

The extent of investor ownership in relation to the concentration of other shareholdings.