CHAPTER 9

Businesses and the Costs of Production

A. Short-Answer, Essays, and Problems

1. Why are costs important in economics?

2. Why don’t economists use the same cost data as accountants use?

3. What is the real cost of putting an unemployed laborer to work raking leaves or digging holes and refilling

them during a severe recession? Explain.

5. Why is it important to distinguish between explicit and implicit costs?

6. Your firm has total sales revenue of $1,000,000 and total explicit costs of $600,000 and total implicit cost

7. Why must normal profits be counted as a cost, according to economists?

8. Evaluate this statement: “If the economic profit is zero, a business will shut down.”

9. Jane quit her job at IBM where she earned $50,000 a year. She cashed in $50,000 in corporate bonds that

earned 10% interest annually to buy a mini-bus. Jane has decided to buy the mini-bus and set up a

commuter service between Lincoln and Omaha. There are 1000 people who will pay $400 a year each for

the commuter service; $280 from each person goes for gas, maintenance, insurance, and depreciation. She

estimates that her entrepreneurial skills would have typically yielded a normal profit of $5,000 in another

business.

10. Debbie was earning $100,000 a year working as a scientist for a drug company. She decided to start her

own business that conducted drug trials. She estimates this entrepreneurial talent or forgone

entrepreneurial income to be $10,000 a year. She used $500,000 in savings that earned 5 percent interest

annually to finance the new business. In the first year, the firm earned revenue of $1,500,000. The costs

for rent, supplies, and employees’ salaries were $1,100,000. What was the accounting profit for the new

business? What was the economic profit (or loss)? Explain your calculations for both questions.

11. Tomas quit his job at the Tri-City bank where he earned $50,000 a year to start his own businesses, a bank

marketing company. He estimates his entrepreneurial talent or forgone entrepreneurial income to be

$5,000 a year. He used $100,000 in savings that earned 5 percent interest annually to finance the new

business. In the first year, the firm earned revenue of $250,000. The costs for rent, supplies, and an

12. John is determining whether he should close his construction firm. His accountant has advised him to

12. Why is the distinction between fixed and variable cost important?

13. Indicate whether the inputs below are variable (V) or fixed (F) in the short run.

Input

Output

14. What is the difference between the short run and the long run?

15. Explain the difference between total product, marginal product and average product.

16. What is the relationship between total product, marginal product, and average product shown by the law of

diminishing returns?

17. Interpret this statement: “If diminishing returns did not occur, the world could be fed out of a flower pot.”

18. Comment on the problem with this statement: “Of course, there are diminishing marginal returns from

19. What is the law of diminishing returns? Give a descriptive example.

20. (Consider This) How can total course learning and studying be related to the law of diminishing returns?

21. The table below shows the total production of a firm as the quantity of labor employed increases. The

quantities of all other resources employed are constant. Compute the marginal and average products and

enter them in the table.

Inputs of

labor

Total

product

Marginal

product of

labor

Average

product of

labor

0

0

—

—

1

40

_____

_____

2

100

_____

_____

3

165

_____

_____

4

200

_____

_____

5

225

_____

_____

6

240

_____

_____

7

245

_____

_____

8

240

_____

_____

22. Explain: “Whenever a number which is less than the previous average of a total is added to that total, the

average will necessarily fall. Conversely, whenever a number which is greater than the previous average of

a total is added to that total, the average will necessarily rise.” How does this help explain the relationship

between the various short-run cost curves? Between the various productivity curves?

23. Complete the following table by finding the average and marginal product. At what input-output level will

average variable cost begin to rise? Explain.

24. You are given the following short-run information for an individual firm. Labor (L) is the only variable

input. The price of labor is $200/week. Fixed costs are $100/week. Complete the rest of the table.

Describe the relationship between the MP and MC. At which output level does the law of diminishing

returns set in?

25. What is the relationship between marginal cost and marginal product?

26. Why does the short-run marginal-cost curve eventually increase for the typical firm?

27. Assume that a firm has a plant of fixed size and that it can vary its output only by varying the amount of

labor it employs. The table below shows the relationships among the amount of labor employed, the output

of the firm, the marginal product of labor, and the average product of labor.

(e) Describe the relationship between the average product of labor and the average variable cost.

1

10

10

10.00

$_____

$_____

$_____

2

22

12

11.00

_____

_____

_____

3

36

14

12.00

_____

_____

_____

4

48

12

12.00

_____

_____

_____

5

58

10

11.60

_____

_____

_____

6

66

8

11.00

_____

_____

_____

7

72

6

10.28

_____

_____

_____

8

76

4

9.50

_____

_____

_____

9

78

2

8.66

_____

_____

_____

10

78

0

7.80

_____

_____

_____

28. Assume a firm has fixed costs of $80 and variable costs as indicated in the table below. Complete the cost

table.

29. Complete the following short-run cost table using the information provided.

Total

product

TFC

AFC

TVC

AVC

TC

MC

30. In the table below you will find a schedule of a firm’s fixed cost and variable cost. Complete the table by

computing total cost, average fixed cost, average variable cost, average total cost, and marginal cost.

31. Complete the following short-run cost table using the information provided.

Q

TC

TFC

TVC

AVC

ATC

MC

32. (Consider This) Suppose your friend is currently a nursing major. She decides she wants to switch her

32.Answer the questions below on the basis of the diagram.

(a) How can you tell if these cost curves are for the short run or the long run?

(b) What does the graph indicate about:

(1) AVC at 6000 units of output?

(2) ATC at 6000 units of output?

(3) AFC at 6000 units of output?

(4) TVC at 6000 units of output?

(5) TFC at all levels of output?

36. The following are three short-run average total cost schedules for the only three possible plant sizes, 1, 2,

and 3. Find the long-run average cost schedule and show the result in the second table.

60

1.05

70

.90

90

1.05

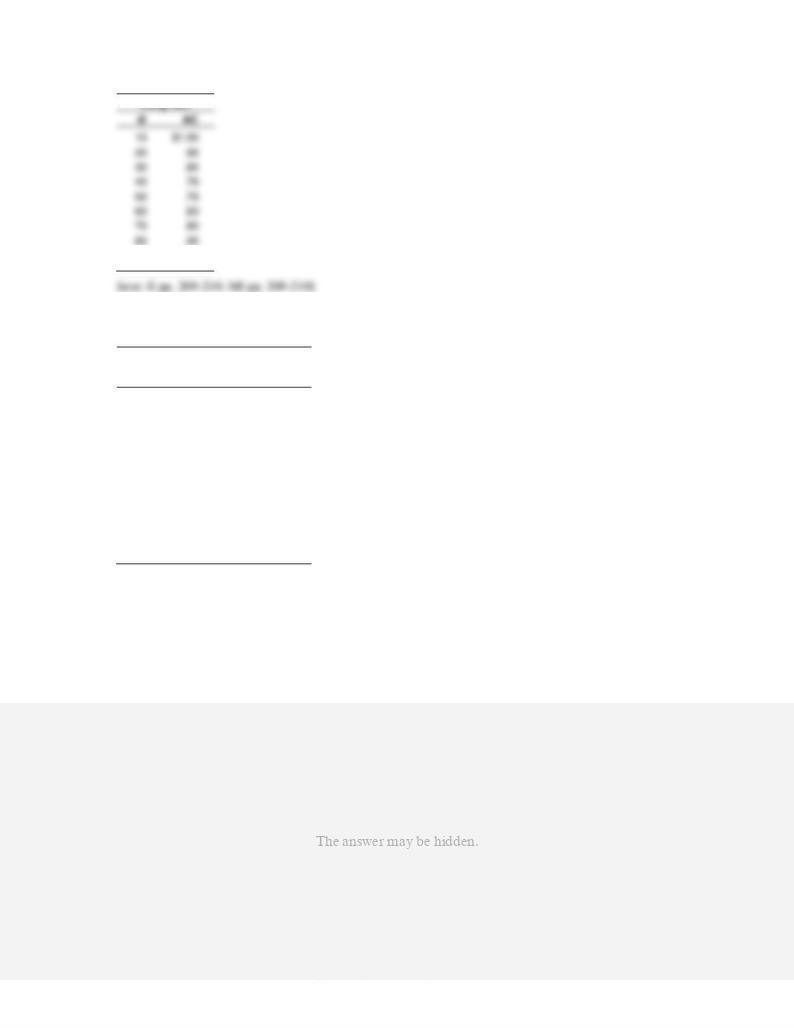

37. In the table below are data from a book company that prints and binds special-order books. The data show

various quantities that can be produced by the firm in an hour and the unit costs of each quantity.

(1)

Quantity of

books

(2)

Unit cost A

of books

(3)

Unit cost B

of books

100

$70

$_____

200

60

_____

300

50

_____

400

40

_____

500

35

_____

600

30

_____

700

35

_____

800

45

_____

900

60

_____

1000

80

_____

38. Below are the short-run average-total-cost schedules for three plants of different size that a firm might

build to produce its product. Assume that these are the only possible sizes of plants that the firm might

build. What is the long-run average-cost schedule for the firm? Show it in the second table below.

Output

Average cost

39. How can diseconomies of scale occur at larger capacities?

40. What factors explain economies of scale?

41. What is minimum efficient scale? What insights would it give about the size of firms in an industry?

42. The values for the long-run ATC curves of three different firms are listed in the table below.

Quantity

ATC 1

ATC 2

ATC 3

5

10

7

12

10

8

6

9

15

7

5

7

20

6

6

6

25

6

7

5

30

6

9

4

35

7

13

6

43. Consider the diagram below. Curves 1–8 are the short-run curves which occur with different plant sizes.

Answer the next two questions.

(a) On the graph show the range of outputs for: (1) economies of scale; (2) diseconomies of scale:

Indicate (3) minimum efficient scale.

(b) In the long run, what plant size should the firm build if it wants to produce: (1) 6000 units; (2) 14,000

units?

44. What effect does the increase of the price of corn have on the cost curves of a firm producing items like

cereal, tortilla shells and chewing gum?

45. What effect does the increase of the price of gasoline have on the cost curves of package delivery firms

46. What are some of the sources of cost savings for recent business start-ups in the U.S. economy such as

Intel, Starbucks, Microsoft, Dell, Google and Cisco Systems?

47. How would a Verson stamping machine help a firm achieve economies of scale?

48. Explain how the Internet has affected the average fixed cost of a daily print newspaper.

49. Why are there two plants run by one firm that produce large commercial aircraft and thousands of plants

run by hundreds of firms that produce ready-mix concrete? Explain in terms of economies of scale.

51. (Last Word) Discuss how the 3-D printer is set to make manufactured goods more affordable for the average

person in the United States.

B. Answers to Short-Answer, Essays, and Problems

1. Why are costs important in economics?

2. Why don’t economists use the same cost data as accountants use?

Implicit costs are as important as the explicit costs which are generally the so-called “accounting costs.”

For example, economists (but not accountants) would count the income forgone in the use of the owner’s

3. What is the real cost of putting an unemployed laborer to work raking leaves or digging holes and refilling

them during a severe recession? Explain.

5. Why is it important to distinguish between explicit and implicit costs?

Implicit costs are as important as the explicit costs which are generally the so-called “accounting costs.”

For example, economists (but not accountants) would count the income forgone in the use of the owner’s

6. Your firm has total sales revenue of $1,000,000 and total explicit costs of $600,000 and total implicit cost

of $300,000. What will be the accounting profit for the firm? What will be the economic profit for the

firm? Explain the difference using the data.

explicit and implicit). The total of the implicit and explicit costs is $900,000 ($600,000 plus $300,000).

7. Why must normal profits be counted as a cost, according to economists?

8. Evaluate this statement: “If the economic profit is zero, a business will shut down.”

9. Jane quit her job at IBM where she earned $50,000 a year. She cashed in $50,000 in corporate bonds that

earned 10% interest annually to buy a mini-bus. Jane has decided to buy the mini-bus and set up a

commuter service between Lincoln and Omaha. There are 1000 people who will pay $400 a year each for

the commuter service; $280 from each person goes for gas, maintenance, insurance, and depreciation. She

estimates that her entrepreneurial skills would have typically yielded a normal profit of $5,000 in another

business.

(a) Complete the following questions: (1) What are Jane’s total revenues? (2) What are Jane’s explicit

costs? (3) What is her accounting profit?

(b) List the important implicit costs that Jane has not included.

10. Debbie was earning $100,000 a year working as a scientist for a drug company. She decided to start her

own business that conducted drug trials. She estimates this entrepreneurial talent or forgone

entrepreneurial income to be $10,000 a year. She used $500,000 in savings that earned 5 percent interest

annually to finance the new business. In the first year, the firm earned revenue of $1,500,000. The costs

for rent, supplies, and employees’ salaries were $1,100,000. What was the accounting profit for the new

business? What was the economic profit (or loss)? Explain your calculations for both questions.

11. Tomas quit his job at the Tri-City bank where he earned $50,000 a year to start his own businesses, a bank

marketing company. He estimates his entrepreneurial talent or forgone entrepreneurial income to be

$5,000 a year. He used $100,000 in savings that earned 5 percent interest annually to finance the new

business. In the first year, the firm earned revenue of $250,000. The costs for rent, supplies, and an

employee’s salary were $200,000. What was the accounting profit for the new business? What was the

economic profit (or loss)? Explain your calculations for both questions.

Total revenue was $250,000 and explicit costs (rent, supplies, and employee salaries and benefits) were

12. John is determining whether he should close his construction firm. His accountant has advised him to

12. Why is the distinction between fixed and variable cost important?

13. Indicate whether the inputs below are variable (V) or fixed (F) in the short run.

Input

Output

14. What is the difference between the short run and the long run?

15. Explain the difference between total product, marginal product and average product.

16. What is the relationship between total product, marginal product, and average product shown by the law of

diminishing returns?

17. Interpret this statement: “If diminishing returns did not occur, the world could be fed out of a flower pot.”

If diminishing returns did not occur, the world could be fed out of a flower pot by simply increasing inputs

18. Comment on the problem with this statement: “Of course, there are diminishing marginal returns from

19. What is the law of diminishing returns? Give a descriptive example.

20. (Consider This) How can total course learning and studying be related to the law of diminishing returns?

21. The table below shows the total production of a firm as the quantity of labor employed increases. The

quantities of all other resources employed are constant. Compute the marginal and average products and

enter them in the table.

Inputs of

labor

Total

product

Marginal

product of

labor

Average

product of

labor

0

0

—

—

1

40

_____

_____

2

100

_____

_____

3

165

_____

_____

4

200

_____

_____

5

225

_____

_____

6

240

_____

_____

7

245

_____

_____

8

240

_____

_____

(a) At what levels are there increasing returns to labor and at what levels are there decreasing returns to

labor?

(b) Describe the relationship between the total product and marginal product.

(c) Describe the relationship between marginal and average product.

Inputs of

labor

Total

product

Marginal

product of

labor

Average

product of

labor

0

0

1

40

40

40

2

100

60

50

3

165

65

55

4

200

35

50

5

225

25

45

6

240

15

40

7

245

5

35

22. Explain: “Whenever a number which is less than the previous average of a total is added to that total, the

average will necessarily fall. Conversely, whenever a number which is greater than the previous average of

a total is added to that total, the average will necessarily rise.” How does this help explain the relationship

between the various short-run cost curves? Between the various productivity curves?

The statement is simply a fact of arithmetic. To find an average, one sums up the relevant numbers and

divides by n, the number of those numbers. The addition of a new number means the sum must now be

divided by (n + 1) to get the new average.

This helps explain the relationship between the marginal cost curve and the average variable and average

total cost curves. Whenever the marginal cost curve is below the average cost curve, it is like the addition

of a number below the average, and the average cost curve (variable or total) will be falling. Whenever the

marginal cost becomes greater than either average cost curve, that average cost will rise.

23. Complete the following table by finding the average and marginal product. At what input-output level will

average variable cost begin to rise? Explain.

3

25

8.33

7

4

30

7.50

5

5

33

6.60

3

6

34

5.67

1

24. You are given the following short-run information for an individual firm. Labor (L) is the only variable

input. The price of labor is $200/week. Fixed costs are $100/week. Complete the rest of the table.

Describe the relationship between the MP and MC. At which output level does the law of diminishing

returns set in?

Total

2

55

35

400

100

500

5.71

3

100

45

600

100

700

4.41

4

150

50

800

100

900

4.00

5

200

50

1000

100

1100

4.00

6

230

30

1200

100

1300

6.66

7

250

20

1400

100

1500

10.00

8

263

13

1600

100

1700

15.38

9

270

7

1800

100

1900

28.57

10

275

5

2000

100

2100

40.00

11

278

3

2200

100

2300

66.66

12

280

2

2400

100

2500

100.00

25. What is the relationship between marginal cost and marginal product?

26. Why does the short-run marginal-cost curve eventually increase for the typical firm?

27. Assume that a firm has a plant of fixed size and that it can vary its output only by varying the amount of

labor it employs. The table below shows the relationships among the amount of labor employed, the output

of the firm, the marginal product of labor, and the average product of labor.

(e) Describe the relationship between the average product of labor and the average variable cost.

1

10

10

10.00

$_____

$_____

$_____

2

22

12

11.00

_____

_____

_____

3

36

14

12.00

_____

_____

_____

4

48

12

12.00

_____

_____

_____

5

58

10

11.60

_____

_____

_____

6

66

8

11.00

_____

_____

_____

7

72

6

10.28

_____

_____

_____

8

76

4

9.50

_____

_____

_____

9

78

2

8.66

_____

_____

_____

10

78

0

7.80

_____

_____

_____

(a) See table.

1

10

10

10.00

$ 20

$2.00

$2.00

2

22

12

11.00

40

1.67

1.82

3

36

14

12.00

60

1.43

1.67

4

48

12

12.00

80

1.67

1.67

5

58

10

11.60

100

2.00

1.72

6

66

8

11.00

120

2.50

1.82

7

72

6

10.28

140

3.33

1.94

8

76

4

9.50

160

5.00

2.10

9

78

2

8.66

180

10.00

2.31

10

78

0

7.80

200

—

2.56

(b) Divide the increase in total labor cost by the increase in total output to get marginal cost.

28. Assume a firm has fixed costs of $80 and variable costs as indicated in the table below. Complete the cost

table.

3

180

260

26.67

60

86.67

30

4

220

300

20

55

75

40

6

340

420

13.33

56.67

70

70

7

440

520

11.43

62.86

74.29

100

8

580

660

10

72.50

82.50

140

29. Complete the following short-run cost table using the information provided.

Total

product

TFC

AFC

TVC

AVC

TC

MC

30. In the table below you will find a schedule of a firm’s fixed cost and variable cost. Complete the table by

computing total cost, average fixed cost, average variable cost, average total cost, and marginal cost.

2

100

180

280

50.00

90.00

140.00

80

3

100

240

340

33.33

80.00

113.33

60

4

100

320

420

25.00

80.00

105.00

80

5

100

440

540

20.00

88.00

108.00

120

6

100

600

700

16.66

100.00

116.67

160

7

100

800

900

14.29

114.29

128.57

200

8

100

1040

1140

12.50

142.50

130.00

240

9

100

1340

1440

11.11

148.89

160.00

300

10

100

1800

1900

10.00

180.00

190.00

460

31. Complete the following short-run cost table using the information provided.

Q

TC

TFC

TVC

AVC

ATC

MC

Q

TC

TFC

TVC

AVC

ATC

MC

1

7

4

3

3.00

7.00

$3

2

9

4

5

2.50

4.50

2

3

10

4

6

2.00

3.33

1

4

11

4

7

1.75

2.75

1

5

13

4

9

1.80

2.60

2

6

17

4

13

2.17

2.83

4

7

22

4

18

2.57

3.14

5

32. (Consider This) Suppose your friend is currently a nursing major. She decides she wants to switch her

32. Answer the questions below on the basis of the diagram.

(a) How can you tell if these cost curves are for the short run or the long run?

(b) What does the graph indicate about:

(1) AVC at 6000 units of output?

(2) ATC at 6000 units of output?

(3) AFC at 6000 units of output?

(4) TVC at 6000 units of output?

(5) TFC at all levels of output?

(6) TC at 10,000 units of output?

33. Explain what happens to AFC, AVC, ATC, and MC curves in these two situations: (a) fixed cost increase;

(b) variable cost increase.

34. What effect would each of the following have on the short-run average and marginal costs of an auto

dealership: (a) auto mechanics receive a 10% wage increase; (b) property taxes decrease; (c) auto dealers

institute a one-time only promotional campaign?

35. Explain the circumstances under which a firm might encounter a rather extended range of output over

which long-run average costs are relatively constant.

36. The following are three short-run average total cost schedules for the only three possible plant sizes, 1, 2,

and 3. Find the long-run average cost schedule and show the result in the second table.

60

1.05

70

.90

90

1.05

Long Run

Q

AC

10

$_____

_____

_____

_____

_____

_____

_____

_____

_____

_____

_____

_____

_____

_____

_____

90

_____

Long Run

90

1.05

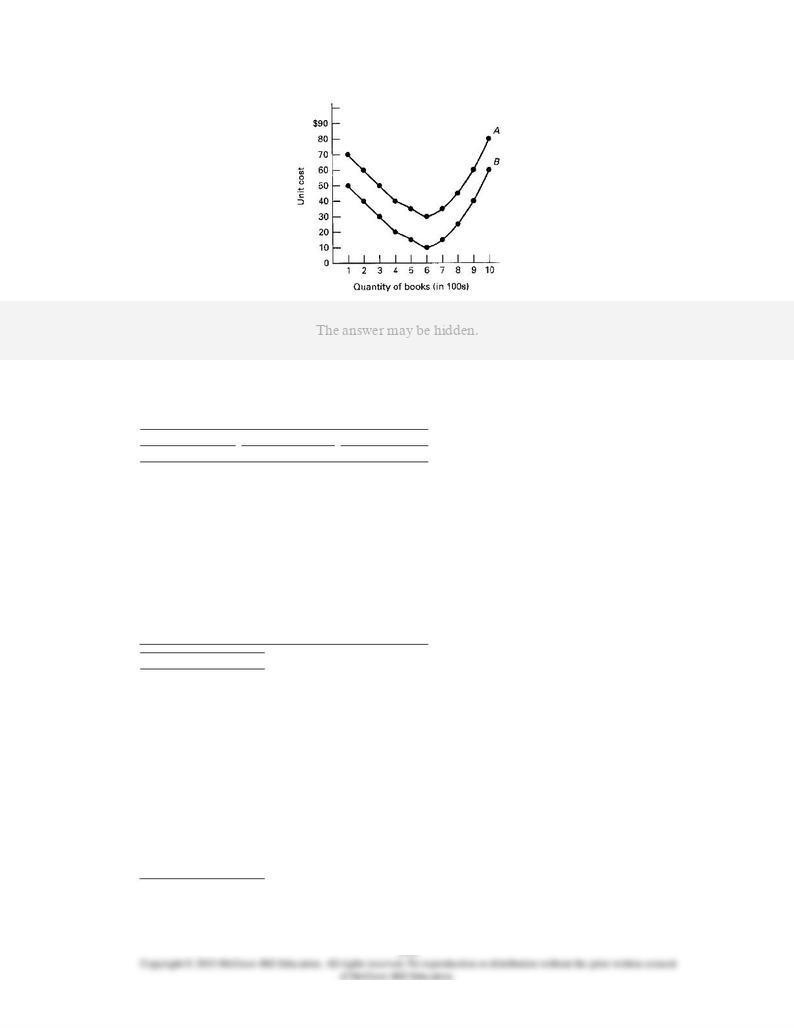

37. In the table below are data from a book company that prints and binds special-order books. The data show

various quantities that can be produced by the firm in an hour and the unit costs of each quantity.

(1)

Quantity of

books

(2)

Unit cost A

of books

(3)

Unit cost B

of books

100

$70

$_____

200

60

_____

300

50

_____

400

40

_____

500

35

_____

600

30

_____

700

35

_____

800

45

_____

900

60

_____

1000

80

_____

(a) In the graph below, label the axes and plot the long-run average cost curve for this firm using the data

in columns 1 and 2 of the table above.

(b) The firm then decides to subcontract the binding work to another company that specializes in the

binding of books. As a consequence, the unit costs of the firm are decreased by $20 at each output

level. Fill in column 3 of the table, and then graph the new long-run average cost curve B for the firm

on the graph.

(c) What will be the minimum cost with unit cost A? With unit cost B?

(d) If the firm produces 400 books, what will be the cost with curve A? With curve B?

(c) The minimum cost with A will be $30 at 600 units. The minimum cost with B will be $10 with 600

38. Below are the short-run average-total-cost schedules for three plants of different size that a firm might

build to produce its product. Assume that these are the only possible sizes of plants that the firm might

build. What is the long-run average-cost schedule for the firm? Show it in the second table below.

Plant size X

Plant size Y

Plant size Z

Output

ATC

Output

ATC

Output

ATC

5

$10

5

$13

5

$72

10

9

10

12

10

65

15

8

15

11

15

52

20

7

20

10

20

41

25

6

25

8

25

33

30

9

30

7

30

20

35

12

35

9

35

15

40

18

40

12

40

14

45

20

45

17

45

12

50

23

50

19

50

14

55

29

55

25

55

20

60

31

60

33

60

30

Output

Average cost

5

$_____

10

_____

15

_____

20

_____

25

_____

30

_____

35

_____

40

_____

45

_____

50

_____

55

_____

60

_____

For what output levels should the firm build plant X, plant Y, and plant Z?

39. How can diseconomies of scale occur at larger capacities?

40. What factors explain economies of scale?

41. What is minimum efficient scale? What insights would it give about the size of firms in an industry?

42. The values for the long-run ATC curves of three different firms are listed in the table below.

Quantity

ATC 1

ATC 2

ATC 3

5

10

7

12

10

8

6

9

15

7

5

7

20

6

6

6

25

6

7

5

30

6

9

4

35

7

13

6

40

8

17

9

(a) Which firm faces the lowest minimum ATC?

(b) Which firm has the greatest minimum efficient scale?

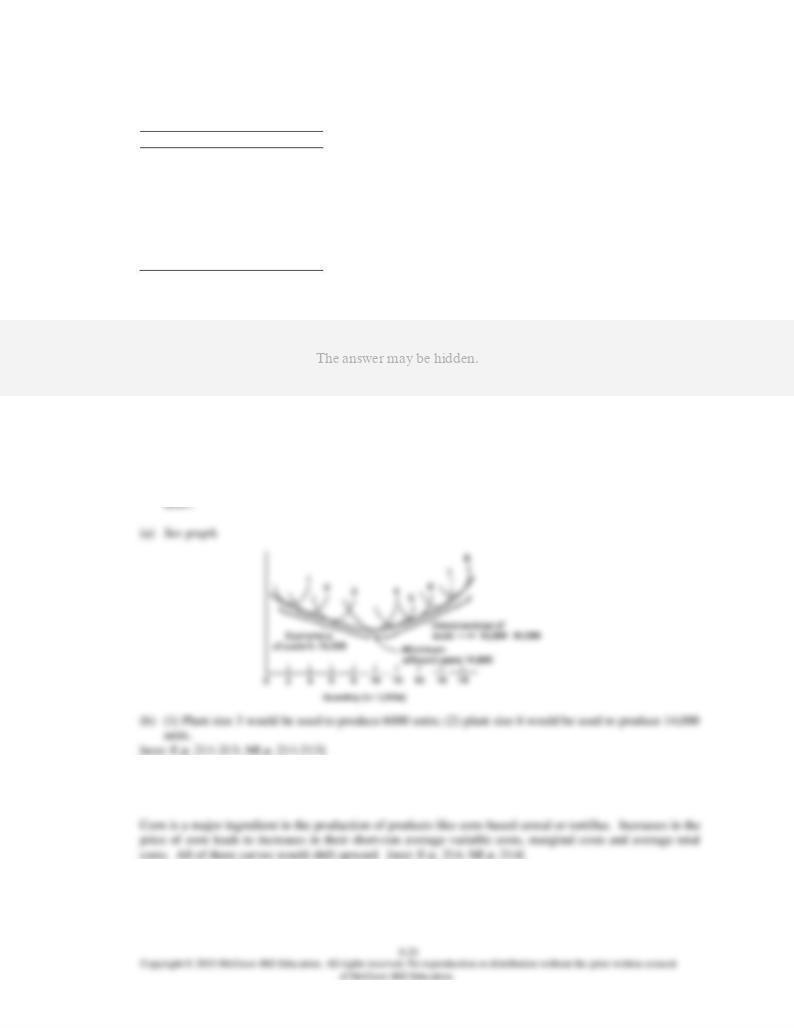

43. Consider the diagram below. Curves 1–8 are the short-run curves that occur with different plant sizes.

Answer the next two questions.

(a) On the graph show the range of outputs for: (1) economies of scale; (2) diseconomies of scale:

Indicate (3) minimum efficient scale.

(b) In the long run, what plant size should the firm build if it wants to produce: (1) 6000 units; (2) 14,000

44. What effect does the increase of the price of corn have on the cost curves of a firm producing items like

corn-based cereal or tortillas?

45. What effect does the increase of the price of gasoline have on the cost curves of package delivery firms

such as Federal Express or United Parcel Service? How might the effects differ for a software firm such as

Symantec that uses the Internet?

Gasoline is a major input used in businesses involved in package delivery such as Federal Express or

46. What are some of the sources of cost savings for business start-ups in the U.S. economy such as Google,

Intel, Starbucks, and Microsoft?

47. How would a Verson stamping machine help a firm achieve economies of scale?

48. Explain how the Internet has affected the average fixed cost of a daily print newspaper.

49. Why are there two plants run by one firm that produce large commercial aircraft and thousands of plants

50. (Last Word) The iPhone costs billions of dollars to develop. Discuss why this product is available to the

average person in the United States.

51. (Last Word) Discuss how the 3-D printer is set to make manufactured goods more affordable for the

average person in the United States.