Chapter 15: The Statement of Cash Flows

Student: ___________________________________________________________________________

2. Because noncash investing and financing transactions do not affect cash, they should not be reflected in the

4. The statement of cash flows discloses the effect on cash of the purchase and sale of both short- and long-term

7. For purposes of preparing the statement of cash flows, cash is defined as including both cash and cash

9. The statement of cash flows shows the effects on net income of a company's operating, investing, and

11. The primary purpose of the statement of cash flows is to provide information about a company's cash

12. The primary purpose of the statement of cash flows is to provide information about a company's investing

13. Investors could use the statement of cash flows to determine whether the company will be able to pay

14. The statement of cash flows explains the difference between net income as shown on the income statement

15. Interest paid on bonds payable would be included in the financing activities category on the statement of

16. Interest received on investments would be included in the operating activities category on the statement of

17. Cash payments made on accounts payable or accrued liabilities are considered repayments of loans and are

18. Noncash investing and financing transactions, such as the exchange of a long-term asset for a long-term

liability, represent significant investing and financing activities and are reflected in a separate schedule as part

19. The income statement indicates a business's success or failure in earning an income from its operating

20. Under the indirect method, gains or losses from the sale of equipment used in operations would appear as

21. When preparing a statement of cash flows using the indirect method, amortization expense is added to net

22. When preparing a statement of cash flows using the indirect method, a gain on sale of land is deducted from

23. When preparing a statement of cash flows using the indirect method, depreciation expense is added to net

24. When preparing a statement of cash flows using the indirect method, an increase in accounts receivable is

25. When preparing a statement of cash flows using the indirect method, an increase in wages payable is

26. When preparing a statement of cash flows using the indirect method, an increase in accounts payable is

27. A decrease in the balance of merchandise inventory is subtracted from net income when calculating net cash

28. Determining net cash flows from operating activities using the indirect method reveals cash collected from

29. Purchases and sales of long-term investments for the period should be netted for disclosure in the investing

30. When presenting decreases in long-term investments in the investing activities section of the statement of

31. Since investing activities center on the long-term assets shown on the balance sheet, they do not include any

32. A decrease in plant assets shown in the investing activities section of the statement of cash flows would be

33. Cash inflows and outflows are not netted in the investing activities section of the statement of cash flows but

34. Payment of dividends would be reflected as a cash outflow in the investing activities section of the

35. The activity on the balance sheet to be presented in the financing activities section of the statement of cash

36. The financing activities section of the statement of cash flows includes certain transactions and activities

37. Issuance of notes, either long- or short-term, would be reflected in the financing activities section of the

38. Dividends declared but unpaid are reflected in the financing activities section of the statement of cash

39. Since it impacts Retained Earnings, the net income for the period would appear in the cash flows from

45. Net cash flows from operating activities would be needed to calculate cash flow yield, cash flows to assets,

46. A positive free cash flow indicates that the company has met all its planned cash commitments and has cash

54. Kingston Company settled a long-term note payable it owed to Creative Company by issuing capital

55. Which of the following is reported as a noncash investing and financing transaction on the statement of cash

56. Lincoln Company engaged in this transaction:

Declared and issued the required dividend on preferred stock.

Indicate which section, if any, the above transaction would appear in, or relate to, on a statement of cash

57. Lincoln Company engaged in this transaction:

Collected accounts receivable.

Indicate which section, if any, the above transaction would appear in, or relate to, on a statement of cash

58. Lincoln Company engaged in this transaction:

Accrued interest expense on long-term bonds payable.

Indicate which section, if any, the above transaction would appear in, or relate to, on a statement of cash

59. Lincoln Company engaged in this transaction:

Retired long-term debt with cash.

Indicate which section, if any, the above transaction would appear in, or relate to, on a statement of cash

60. Lincoln Company engaged in this transaction:

Sold land it was holding for speculation.

Indicate which section, if any, the above transaction would appear in, or relate to, on a statement of cash

61. Lincoln Company engaged in this transaction:

Issued stock for land.

Indicate which section, if any, the above transaction would appear in, or relate to, on a statement of cash

62. Lincoln Company engaged in this transaction:

As required by the landlord, prepaid one year’s rent on its leased warehouse.

Indicate which section, if any, the above transaction would appear in, or relate to, on a statement of cash

63. Lincoln Company engaged in this transaction:

Abandoned fully depreciated equipment.

Indicate which section, if any, the above transaction would appear in, or relate to, on a statement of cash

64. Lincoln Company engaged in this transaction:

Received dividends on marketable securities held as a long-term investment.

Indicate which section, if any, the above transaction would appear in, or relate to, on a statement of cash

65. Lincoln Company engaged in this transaction:

Paid income taxes.

Indicate which section, if any, the above transaction would appear in, or relate to, on a statement of cash

66. Lincoln Company engaged in this transaction:

Issued common stock for cash.

Indicate which section, if any, the above transaction would appear in, or relate to, on a statement of cash

67. Lincoln Company engaged in this transaction:

Received 6-month’s rent in advance from a tenant in its office building.

Indicate which section, if any, the above transaction would appear in, or relate to, on a statement of cash

68. Lincoln Company engaged in this transaction:

Accrued employee wages earned but not yet paid at year-end.

Indicate which section, if any, the above transaction would appear in, or relate to, on a statement of cash

69. Lincoln Company engaged in this transaction:

Transferred cash to money market account.

Indicate which section, if any, the above transaction would appear in, or relate to, on a statement of cash

70. Lincoln Company engaged in this transaction:

Converted loans payable to stock.

Indicate which section, if any, the above transaction would appear in, or relate to, on a statement of cash

71. Lincoln Company engaged in this transaction:

Acquired long-term investment by issuance of long-term debt.

Indicate which section, if any, the above transaction would appear in, or relate to, on a statement of cash

72. Lincoln Company engaged in this transaction:

Purchased 30-day U.S. Treasury bill.

Indicate which section, if any, the above transaction would appear in, or relate to, on a statement of cash

73. Lincoln Company engaged in this transaction:

Purchased 60-day commercial paper.

Indicate which section, if any, the above transaction would appear in, or relate to, on a statement of cash

74. Lincoln Company engaged in this transaction:

Purchased treasury stock with cash.

Indicate which section, if any, the above transaction would appear in, or relate to, on a statement of cash

77. If the indirect method is used to prepare a statement of cash flows, which of the following would be added

78. If the indirect method is used to prepare a statement of cash flows, which of the following would be added

80. Assume the indirect method is used to compute net cash flows from operating activities. For this item

extracted from the financial statements—Decrease in Accounts Receivable—indicate the effect on net income

81. Assume the indirect method is used to compute net cash flows from operating activities. For this item

extracted from the financial statements—Dividend Income (assume that cash received is equal to amount

reported)—indicate the effect on net income in arriving at net cash flows from operating activities by choosing

82. Assume the indirect method is used to compute net cash flows from operating activities. For this item

extracted from the financial statements—Interest Income (assume that cash received is equal to amount

reported)—indicate the effect on net income in arriving at net cash flows from operating activities by choosing

83. Assume the indirect method is used to compute net cash flows from operating activities. For this item

extracted from the financial statements—Decrease in Inventory—indicate the effect on net income in arriving at

84. Assume the indirect method is used to compute net cash flows from operating activities. For this item

extracted from the financial statements—Increase in Prepaid Expenses—indicate the effect on net income in

85. Assume the indirect method is used to compute net cash flows from operating activities. For this item

extracted from the financial statements—Increase in Accounts Payable—indicate the effect on net income in

86. Assume the indirect method is used to compute net cash flows from operating activities. For this item

extracted from the financial statements—Decrease in Accrued Liabilities—indicate the effect on net income in

87. Assume the indirect method is used to compute net cash flows from operating activities. For this item

extracted from the financial statements—Interest Expense (assume that cash payments are equal to amount

reported)—indicate the effect on net income in arriving at net cash flows from operating activities by choosing

88. Assume the indirect method is used to compute net cash flows from operating activities. For this item

extracted from the financial statements—Decrease in Income Taxes Payable—indicate the effect on net income

89. Assume the indirect method is used to compute net cash flows from operating activities. For this item

extracted from the financial statements—Depletion Expense—indicate the effect on net income in arriving at

90. Assume the indirect method is used to compute net cash flows from operating activities. For this item

extracted from the financial statements—Gain on Sale of Investment—indicate the effect on net income in

91. Assume the indirect method is used to compute net cash flows from operating activities. For this item

extracted from the financial statements—Loss on Disposal of Equipment—indicate the effect on net income in

92. If the indirect method is used, which of the following would be added to net income to arrive at net cash

93. If the indirect method is used, which of the following would be subtracted from net income to arrive at net

94. If the indirect method is used, which of the following is a proper adjustment to net income to arrive at net

95. Assume that the balance of accounts payable does not change during a period. When preparing a statement

of cash flows, an increase in ending inventory over beginning inventory will result in an adjustment to net

96. In preparing a statement of cash flows using the indirect method, a decrease in an unearned revenue account

97. Bailey Corp. sold investments for $204,000 cash that cost $180,000. The journal entry to record the

98. Freewalt Co. purchased investments for $160,000 cash. The journal entry to record this transaction that

99. Dina Corporation purchased plant assets for $60,000 cash. The journal entry to record the transaction that

100. Northbrook Corporation issued $60,000 bonds payable to acquire Machinery. The journal entry to record

101. Rufina Corp. sold for $20,000 plant assets that cost $40,000 and that had an accumulated depreciation of

102. Determining cash flows from investing activities is the ________ step in preparing the statement of cash

104. Foxworth Company sold plant assets that had accumulated depreciation of $20,000. These assets cost

Foxworth $70,000 when purchased 4 years ago. The sale of the assets resulted in a gain for Foxworth of

105. Use this information to answer the following question.

1. Sold machinery for $9,000 cash.

2. Purchased a building for $80,000 cash.

3. Issued $70,000 worth of stock to acquire an airplane.

4. Converted long-term bonds by issuing $100,000 worth of stock.

5. Declared and paid a $10,000 cash dividend.

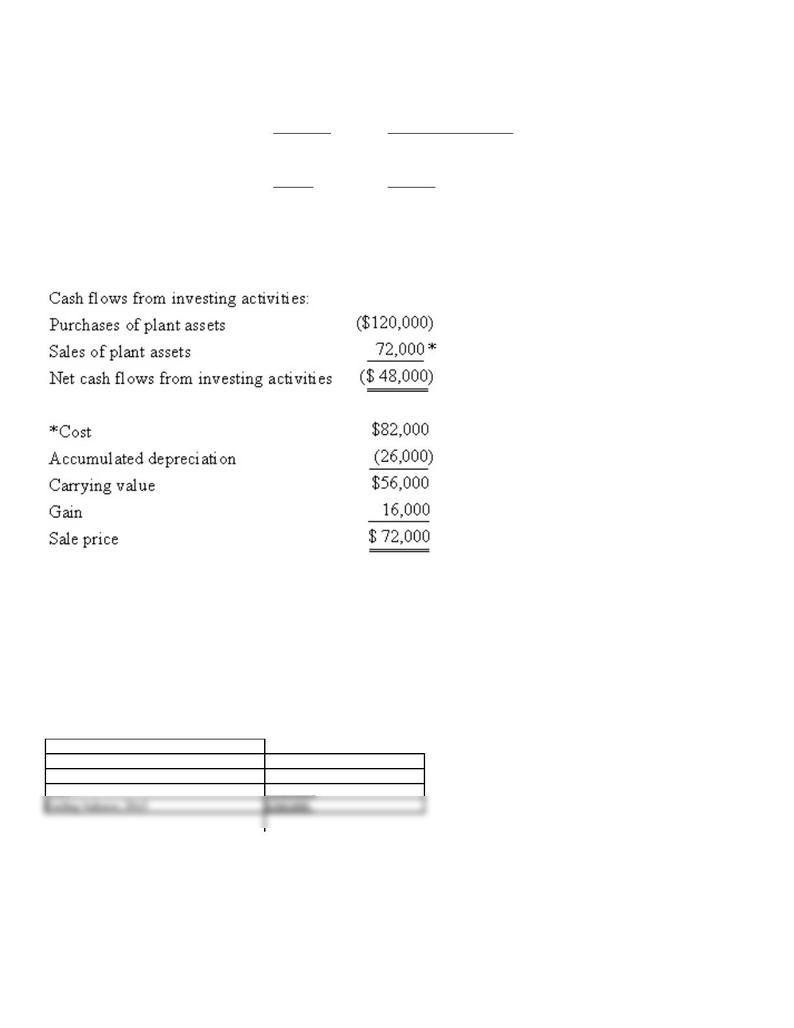

106. Use this information to answer the following question.

1. Sold machinery for $9,000 cash.

2. Purchased a building for $80,000 cash.

3. Issued $70,000 worth of stock to acquire an airplane.

4. Converted long-term bonds by issuing $100,000 worth of stock.

5. Declared and paid a $10,000 cash dividend.

107. Use this information to answer the following question.

1. Sold machinery for $9,000 cash.

2. Purchased a building for $80,000 cash.

3. Issued $70,000 worth of stock to acquire an airplane.

4. Converted long-term bonds by issuing $100,000 worth of stock.

5. Declared and paid a $10,000 cash dividend.

108. Use this information to answer the following question.

1. Sold machinery for $9,000 cash.

2. Purchased a building for $80,000 cash.

3. Issued $70,000 worth of stock to acquire an airplane.

4. Converted long-term bonds by issuing $100,000 worth of stock.

5. Declared and paid a $10,000 cash dividend.

109. Use this information to answer the following question.

1. Sold machinery for $9,000 cash.

2. Purchased a building for $80,000 cash.

3. Issued $70,000 worth of stock to acquire an airplane.

4. Converted long-term bonds by issuing $100,000 worth of stock.

5. Declared and paid a $10,000 cash dividend.

110. On a statement of cash flows prepared using the indirect method, the amount representing cash paid for

113. Which of the following items would not be included in a statement of cash flows prepared using the

115. Grace Corporation issued 60,000 shares of $5 par value common stock for $600,000. The journal entry to

117. If net cash flows from operating activities were $388,000, net income were $100,000, and net sales were

118. If net cash flows from operating activities were $296,000, net income were $200,000, and sales were

121. During 20x5, Oates Company had sales of $250,000, net income of $25,000, average total assets of

$350,000, dividend payments of $17,500, net cash flows from operating activities of $26,000, purchases of

plant assets of $37,500, and sales of plant assets of $45,000. Cash flow yield equals (Round amounts to one

122. During 20x5, Oates Company had sales of $500,000, net income of $50,000, average total assets of

$700,000, dividend payments of $35,000, net cash flows from operating activities of $90,000, purchases of

plant assets of $75,000, and sales of plant assets of $90,000. Cash flows to sales equals (Round amounts to one

123. During 20x5, Oates Company had sales of $250,000, net income of $25,000, average total assets of

$350,000, dividend payments of $17,500, net cash flows from operating activities of $36,000, purchases of

plant assets of $37,500, and sales of plant assets of $45,000. Cash flows to assets equals (Round amounts to one

124. During 20x5, Oates Company had sales of $500,000, net income of $50,000, average total assets of

$700,000, dividend payments of $35,000, net cash flows from operating activities of $90,000, purchases of

125. To determine whether a company's operations are covering its dividend payments, it is best to focus on

126. Indicate on the blanks below the letter of the type of activity (O = operating activity, F = financing activity,

127. Why does the acquisition of land in exchange for common stock qualify as a noncash investing and

financing transaction?

128. Indicate on the blanks below the letter of the type of activity (O = operating activity, F = financing activity,

129. During the year, Ollie's Outdoor Outfitters issued 20,000 shares of common stock in exchange for a prime

piece of land. Two employees of the accounting department, Audrey and Neil, disagree as to the appearance of

this particular transaction on the statement of cash flows. Audrey believes it to be a significant noncash

transaction, and it therefore should be presented as such at the bottom of the statement. Neil contends that

because this transaction did not cause any cash to flow in or out of the company, it has no place on the

statement of cash flows. Who is correct and why?

130. When preparing a statement of cash flows using the indirect method, why is depreciation added back to net

income within the operating activities section?

131. How is it possible for a company to show a net loss for a given year, yet produce positive net cash flows

from operating activities?

132. Green Skies Company prepares its statement of cash flows using the indirect method. Indicate whether

133. Houston Shoe Co. is preparing a statement of cash flows using the indirect method. Indicate on the blanks

134. Marla Co. sells equipment with a carrying value of $90,000 for $70,000. Where, and for what amounts,

would this transaction appear on a statement of cash flows using the indirect method?

136. Which accounts are analyzed to determine cash flows from financing activities?

137. What elements are used to calculate free cash flow? Indicate whether the element is added or subtracted.

139.

4. A type of marketable security that a company buys and

5. The amount of cash that remains after deducting the

140. Using the indirect method, calculate the amount of net cash flows from operating activities from the

following data. Show your work

141. Using the indirect method, calculate the amount of net cash flows from operating activities from the

following data. Show your work.

142. Following are the income statement and other information for Zambrano Corporation.

Zambrano Corporation

Income Statement

For the Year Ended December 31, 20x5

Sales

$6,000

Cost of goods sold

3

,

0

0

0

Gross margin

$

3

143. Following are the income statement and other information for American Horse Corporation.

American Horse Corporation

Income Statement

For the Year Ended December 31, 20x5

Sales

$6,000

Cost of goods sold

3

,

0

0

0

Gross margin

$

3

144. The following comparative balance sheet and other information relate to Carlson Company.

Carlson Company

Comparative Balance Sheets

December 31, 20x5 and 20x4

Assets

20x5

20x4

Cash

$ 140

$ 140

Accounts receivable (net)

210

280

Inventory

350

420

Prepaid expenses

105

70

Equipment (net)

3,010

2,800

Investments and other assets

4,900

4,200

Total assets

$8,715

$7,910

Liabilities and Stockholders' Equity

Accounts payable

$ 350

$ 280

Income taxes payable

70

140

Long-term note payable

2,100

1,400

Common stock

1,400

1,400

Retained earnings

4,795

4,690

Total liabilities and stockholders' equity

$8,715

$7,910

145. Ralston Company's cash balance at December 31, 20x5, was $23,000. During the year, Ralston sold assets

with a book value of $245,000 that resulted in a loss of $110,000. Calculate the company's cash balance at

December 31, 20x6 , given the following information for the year ended December 31, 20x6. Show your work.

Net Income

$470,000

Depreciation and Amortization Expense

88,000

Decrease in Accounts Receivable (net)

14,000

Decrease in Inventory

25,000

Increase in Accounts Payable

20,000

Net Cash Flows from Investing Activities

??

Net Cash Flows from Financing Activities

(400,000)

146. The activity in the Plant Assets and related Accumulated Depreciation accounts for 20x5 is shown below.

In addition, the income statement shows a gain on sale of plant assets of $16,000.

Plant Assets

Accumulated Depreciation

20x5 Beginning balance

$234,000

$124,000

20x5 Purchases

120,000

20x5 Depreciation

36,000

20x5 Disposals

(82,000)

(26,000)

20x5 Ending balance

$272,000

$134,000

Based on the information given, compute the amounts to be shown and indicate how they would appear on the statement of cash flows. Assume that

the indirect method is being used and that the plant assets were purchased for cash.

147. The activity from the Long-Term Investments account for Fisk Corporation appears below. In addition, the

income statement shows a loss on the sale of investments of $32,000.

Long-Term Investments

Beginning balance, 20x5

$184,000

Purchases

278,000

Sales

(202,000)

Ending balance, 20x5

$260,000

Based on the information given, compute the amounts to be shown and indicate how they would appear on the statement of cash flows. Assume that

the indirect method is being used and that the investments were purchased for cash.

148. The following 20x5 information relates to Taylor, Inc.:

Net Income

$365,000

Depreciation Expense

96,000

Amortization of Intangible Assets

11,000

Beginning Accounts Receivable

420,000

Ending Accounts Receivable

439,000

Beginning Inventory

516,000

Ending Inventory

560,000

Beginning Prepaid Expenses

48,000

Ending Prepaid Expenses

42,000

Beginning Accounts Payable

119,000

Ending Accounts Payable

146,000

Purchase of Long-Term Assets for Cash

616,000

Cash from Issuance of Long-Term Debt

200,000

Issuance of Stock for Cash

160,000

Issuance of Stock for Long-Term Assets

110,000

Purchase of Treasury Stock

64,000

Sale of Long-Term Investment at Cost

39,000

149. The following information relates to Royale Enterprises for the year ended December 31, 20x5:

Net Income

$300,000

Depreciation Expense

72,000

Amortization of Intangible Assets

9,000

Beginning Accounts Receivable

336,000

Ending Accounts Receivable

351,000

Beginning Inventory

413,000

Ending Inventory

450,000

Beginning Prepaid Expenses

34,000

Ending Prepaid Expenses

38,000

Beginning Accounts Payable

95,000

Ending Accounts Payable

116,000

Purchase of Long-Term Assets for Cash

493,000

Cash from Issuance of Long-Term Debt

160,000

Issuance of Stock for Cash

128,000

Issuance of Stock for Long-Term Assets

88,000

Purchase of Treasury Stock

51,000

Sale of Long-Term Investment at Cost

31,000

150. The following information relates to Ferguson Company for 20x6 and 20x5:

Ferguson Company

Comparative Balance Sheets

December 31, 20x6 and 20x5

Assets

20x6

20x5

Change

Cash

$ 21,000

$ 54,000

($ 33,000)

Accounts receivable (net)

421,000

480,000

(59,000)

Inventory

310,000

340,000

(30,000)

Prepaid expenses

17,000

15,000

2,000

Investments

80,000

80,000

0

Land

350,000

300,000

50,000

Building (net)

680,000

700,000

(20,000)

Equipment (net)

520,000

340,000

180,000

Total assets

$2,399,000

$2,309,000

$ 90,000

Liabilities

Accounts payable

$ 328,000

$ 335,000

($ 7,000)

Accrued liabilities

171,000

170,000

1,000

Income taxes payable

22,000

34,000

(12,000)

Bonds payable

410,000

700,000

(290,000)

Long-term note payable

130,000

0

130,000

Total liabilities

$1,061,000

$1,239,000

($178,000)

151. Use the following data for Jenkins Co. to prepare a statement of cash flows using the indirect method for

the year ended June 30, 20x6.

Jenk

ins

Co.

Inco

me

State

ment

For

the

Year

Ende

d

June

30,

20x6

Sales

$700,000

Less

expe

nses

Cost of goods sold

$400,000

Depreciation expense

40,000

Administrative expenses

104,000

Selling expenses

70,000

Loss on sale of investment

1,000

6

1

5

,

0

0

0

Inco

me

befor

e

inco

me

taxes

$ 85,000

152. Use the following data for Window Rock Company to prepare a statement of cash flows using the indirect

method for the year ended June 30, 20x6.

Win

dow

Rock

Com

pany

Inco

me

State

ment

For

the

Year

Ende

d

June

30,

20x6

Sales

$1,400,000

Less

expe

nses

Cost of goods sold

$800,000

Depreciation expense

80,000

Administrative expenses

208,000

Selling expenses

140,000

Loss on sale of investment

2,000

1

,

2

3

0

,

0

0

0

Inco

me

befor

e

170,000

153. For 20x5, Sahara Company had average total assets of $520,000, sales of $450,000, net income of

154. For 20x5, Devers Enterprises had average total assets of $1,040,000, sales of $900,000, net income of

155. Use the following information to obtain the ratios below. Round amounts to one decimal place

Net cash flows from operating activities

$837 million

Net income

465 million

Sales

6,750 million

Average total assets

7,150 million

Dividends

105 million

Purchases of plant assets

170 million

Sales of plant assets

380 million

Chapter 15: The Statement of Cash Flows Key

2. Because noncash investing and financing transactions do not affect cash, they should not be reflected in the

4. The statement of cash flows discloses the effect on cash of the purchase and sale of both short- and long-term

7. For purposes of preparing the statement of cash flows, cash is defined as including both cash and cash

9. The statement of cash flows shows the effects on net income of a company's operating, investing, and

11. The primary purpose of the statement of cash flows is to provide information about a company's cash

12. The primary purpose of the statement of cash flows is to provide information about a company's investing

13. Investors could use the statement of cash flows to determine whether the company will be able to pay

14. The statement of cash flows explains the difference between net income as shown on the income statement

15. Interest paid on bonds payable would be included in the financing activities category on the statement of

16. Interest received on investments would be included in the operating activities category on the statement of

17. Cash payments made on accounts payable or accrued liabilities are considered repayments of loans and are

18. Noncash investing and financing transactions, such as the exchange of a long-term asset for a long-term

liability, represent significant investing and financing activities and are reflected in a separate schedule as part

19. The income statement indicates a business's success or failure in earning an income from its operating

20. Under the indirect method, gains or losses from the sale of equipment used in operations would appear as

21. When preparing a statement of cash flows using the indirect method, amortization expense is added to net

22. When preparing a statement of cash flows using the indirect method, a gain on sale of land is deducted from

23. When preparing a statement of cash flows using the indirect method, depreciation expense is added to net

24. When preparing a statement of cash flows using the indirect method, an increase in accounts receivable is

25. When preparing a statement of cash flows using the indirect method, an increase in wages payable is

26. When preparing a statement of cash flows using the indirect method, an increase in accounts payable is

27. A decrease in the balance of merchandise inventory is subtracted from net income when calculating net cash

28. Determining net cash flows from operating activities using the indirect method reveals cash collected from

29. Purchases and sales of long-term investments for the period should be netted for disclosure in the investing

30. When presenting decreases in long-term investments in the investing activities section of the statement of

31. Since investing activities center on the long-term assets shown on the balance sheet, they do not include any

32. A decrease in plant assets shown in the investing activities section of the statement of cash flows would be

33. Cash inflows and outflows are not netted in the investing activities section of the statement of cash flows but

34. Payment of dividends would be reflected as a cash outflow in the investing activities section of the

35. The activity on the balance sheet to be presented in the financing activities section of the statement of cash

36. The financing activities section of the statement of cash flows includes certain transactions and activities

37. Issuance of notes, either long- or short-term, would be reflected in the financing activities section of the

38. Dividends declared but unpaid are reflected in the financing activities section of the statement of cash

39. Since it impacts Retained Earnings, the net income for the period would appear in the cash flows from

45. Net cash flows from operating activities would be needed to calculate cash flow yield, cash flows to assets,

46. A positive free cash flow indicates that the company has met all its planned cash commitments and has cash

54. Kingston Company settled a long-term note payable it owed to Creative Company by issuing capital

55. Which of the following is reported as a noncash investing and financing transaction on the statement of cash

56. Lincoln Company engaged in this transaction:

Declared and issued the required dividend on preferred stock.

Indicate which section, if any, the above transaction would appear in, or relate to, on a statement of cash

57. Lincoln Company engaged in this transaction:

Collected accounts receivable.

Indicate which section, if any, the above transaction would appear in, or relate to, on a statement of cash

58. Lincoln Company engaged in this transaction:

Accrued interest expense on long-term bonds payable.

Indicate which section, if any, the above transaction would appear in, or relate to, on a statement of cash

59. Lincoln Company engaged in this transaction:

Retired long-term debt with cash.

Indicate which section, if any, the above transaction would appear in, or relate to, on a statement of cash

60. Lincoln Company engaged in this transaction:

Sold land it was holding for speculation.

Indicate which section, if any, the above transaction would appear in, or relate to, on a statement of cash

61. Lincoln Company engaged in this transaction:

Issued stock for land.

Indicate which section, if any, the above transaction would appear in, or relate to, on a statement of cash

62. Lincoln Company engaged in this transaction:

As required by the landlord, prepaid one year’s rent on its leased warehouse.

Indicate which section, if any, the above transaction would appear in, or relate to, on a statement of cash

63. Lincoln Company engaged in this transaction:

Abandoned fully depreciated equipment.

Indicate which section, if any, the above transaction would appear in, or relate to, on a statement of cash

64. Lincoln Company engaged in this transaction:

Received dividends on marketable securities held as a long-term investment.

Indicate which section, if any, the above transaction would appear in, or relate to, on a statement of cash

65. Lincoln Company engaged in this transaction:

Paid income taxes.

Indicate which section, if any, the above transaction would appear in, or relate to, on a statement of cash

66. Lincoln Company engaged in this transaction:

Issued common stock for cash.

Indicate which section, if any, the above transaction would appear in, or relate to, on a statement of cash

67. Lincoln Company engaged in this transaction:

Received 6-month’s rent in advance from a tenant in its office building.

Indicate which section, if any, the above transaction would appear in, or relate to, on a statement of cash

68. Lincoln Company engaged in this transaction:

Accrued employee wages earned but not yet paid at year-end.

Indicate which section, if any, the above transaction would appear in, or relate to, on a statement of cash

69. Lincoln Company engaged in this transaction:

Transferred cash to money market account.

Indicate which section, if any, the above transaction would appear in, or relate to, on a statement of cash

70. Lincoln Company engaged in this transaction:

Converted loans payable to stock.

Indicate which section, if any, the above transaction would appear in, or relate to, on a statement of cash

71. Lincoln Company engaged in this transaction:

Acquired long-term investment by issuance of long-term debt.

Indicate which section, if any, the above transaction would appear in, or relate to, on a statement of cash

72. Lincoln Company engaged in this transaction:

Purchased 30-day U.S. Treasury bill.

Indicate which section, if any, the above transaction would appear in, or relate to, on a statement of cash

73. Lincoln Company engaged in this transaction:

Purchased 60-day commercial paper.

Indicate which section, if any, the above transaction would appear in, or relate to, on a statement of cash

74. Lincoln Company engaged in this transaction:

Purchased treasury stock with cash.

Indicate which section, if any, the above transaction would appear in, or relate to, on a statement of cash

77. If the indirect method is used to prepare a statement of cash flows, which of the following would be added

78. If the indirect method is used to prepare a statement of cash flows, which of the following would be added

80. Assume the indirect method is used to compute net cash flows from operating activities. For this item

extracted from the financial statements—Decrease in Accounts Receivable—indicate the effect on net income

81. Assume the indirect method is used to compute net cash flows from operating activities. For this item

extracted from the financial statements—Dividend Income (assume that cash received is equal to amount

reported)—indicate the effect on net income in arriving at net cash flows from operating activities by choosing

82. Assume the indirect method is used to compute net cash flows from operating activities. For this item

extracted from the financial statements—Interest Income (assume that cash received is equal to amount

reported)—indicate the effect on net income in arriving at net cash flows from operating activities by choosing

83. Assume the indirect method is used to compute net cash flows from operating activities. For this item

extracted from the financial statements—Decrease in Inventory—indicate the effect on net income in arriving at

84. Assume the indirect method is used to compute net cash flows from operating activities. For this item

extracted from the financial statements—Increase in Prepaid Expenses—indicate the effect on net income in

85. Assume the indirect method is used to compute net cash flows from operating activities. For this item

extracted from the financial statements—Increase in Accounts Payable—indicate the effect on net income in

86. Assume the indirect method is used to compute net cash flows from operating activities. For this item

extracted from the financial statements—Decrease in Accrued Liabilities—indicate the effect on net income in

87. Assume the indirect method is used to compute net cash flows from operating activities. For this item

extracted from the financial statements—Interest Expense (assume that cash payments are equal to amount

reported)—indicate the effect on net income in arriving at net cash flows from operating activities by choosing

88. Assume the indirect method is used to compute net cash flows from operating activities. For this item

extracted from the financial statements—Decrease in Income Taxes Payable—indicate the effect on net income

89. Assume the indirect method is used to compute net cash flows from operating activities. For this item

extracted from the financial statements—Depletion Expense—indicate the effect on net income in arriving at

90. Assume the indirect method is used to compute net cash flows from operating activities. For this item

extracted from the financial statements—Gain on Sale of Investment—indicate the effect on net income in

91. Assume the indirect method is used to compute net cash flows from operating activities. For this item

extracted from the financial statements—Loss on Disposal of Equipment—indicate the effect on net income in

92. If the indirect method is used, which of the following would be added to net income to arrive at net cash

93. If the indirect method is used, which of the following would be subtracted from net income to arrive at net

94. If the indirect method is used, which of the following is a proper adjustment to net income to arrive at net

95. Assume that the balance of accounts payable does not change during a period. When preparing a statement

of cash flows, an increase in ending inventory over beginning inventory will result in an adjustment to net

96. In preparing a statement of cash flows using the indirect method, a decrease in an unearned revenue account

97. Bailey Corp. sold investments for $204,000 cash that cost $180,000. The journal entry to record the

98. Freewalt Co. purchased investments for $160,000 cash. The journal entry to record this transaction that

99. Dina Corporation purchased plant assets for $60,000 cash. The journal entry to record the transaction that

100. Northbrook Corporation issued $60,000 bonds payable to acquire Machinery. The journal entry to record

101. Rufina Corp. sold for $20,000 plant assets that cost $40,000 and that had an accumulated depreciation of

102. Determining cash flows from investing activities is the ________ step in preparing the statement of cash

104. Foxworth Company sold plant assets that had accumulated depreciation of $20,000. These assets cost

Foxworth $70,000 when purchased 4 years ago. The sale of the assets resulted in a gain for Foxworth of

105. Use this information to answer the following question.

1. Sold machinery for $9,000 cash.

2. Purchased a building for $80,000 cash.

3. Issued $70,000 worth of stock to acquire an airplane.

4. Converted long-term bonds by issuing $100,000 worth of stock.

5. Declared and paid a $10,000 cash dividend.

106. Use this information to answer the following question.

1. Sold machinery for $9,000 cash.

2. Purchased a building for $80,000 cash.

3. Issued $70,000 worth of stock to acquire an airplane.

4. Converted long-term bonds by issuing $100,000 worth of stock.

5. Declared and paid a $10,000 cash dividend.

107. Use this information to answer the following question.

1. Sold machinery for $9,000 cash.

2. Purchased a building for $80,000 cash.

3. Issued $70,000 worth of stock to acquire an airplane.

4. Converted long-term bonds by issuing $100,000 worth of stock.

5. Declared and paid a $10,000 cash dividend.

108. Use this information to answer the following question.

1. Sold machinery for $9,000 cash.

2. Purchased a building for $80,000 cash.

3. Issued $70,000 worth of stock to acquire an airplane.

4. Converted long-term bonds by issuing $100,000 worth of stock.

5. Declared and paid a $10,000 cash dividend.

109. Use this information to answer the following question.

1. Sold machinery for $9,000 cash.

2. Purchased a building for $80,000 cash.

3. Issued $70,000 worth of stock to acquire an airplane.

4. Converted long-term bonds by issuing $100,000 worth of stock.

5. Declared and paid a $10,000 cash dividend.

110. On a statement of cash flows prepared using the indirect method, the amount representing cash paid for

113. Which of the following items would not be included in a statement of cash flows prepared using the

115. Grace Corporation issued 60,000 shares of $5 par value common stock for $600,000. The journal entry to

117. If net cash flows from operating activities were $388,000, net income were $100,000, and net sales were

118. If net cash flows from operating activities were $296,000, net income were $200,000, and sales were

121. During 20x5, Oates Company had sales of $250,000, net income of $25,000, average total assets of

$350,000, dividend payments of $17,500, net cash flows from operating activities of $26,000, purchases of

plant assets of $37,500, and sales of plant assets of $45,000. Cash flow yield equals (Round amounts to one

122. During 20x5, Oates Company had sales of $500,000, net income of $50,000, average total assets of

$700,000, dividend payments of $35,000, net cash flows from operating activities of $90,000, purchases of

plant assets of $75,000, and sales of plant assets of $90,000. Cash flows to sales equals (Round amounts to one

123. During 20x5, Oates Company had sales of $250,000, net income of $25,000, average total assets of

$350,000, dividend payments of $17,500, net cash flows from operating activities of $36,000, purchases of

plant assets of $37,500, and sales of plant assets of $45,000. Cash flows to assets equals (Round amounts to one

124. During 20x5, Oates Company had sales of $500,000, net income of $50,000, average total assets of

$700,000, dividend payments of $35,000, net cash flows from operating activities of $90,000, purchases of

125. To determine whether a company's operations are covering its dividend payments, it is best to focus on

126. Indicate on the blanks below the letter of the type of activity (O = operating activity, F = financing activity,

1. F

4. O

2. O

5. N

3. F

6. O

127. Why does the acquisition of land in exchange for common stock qualify as a noncash investing and

financing transaction?

128. Indicate on the blanks below the letter of the type of activity (O = operating activity, F = financing activity,

1. F

5. N

8. N

2. N

6. O

9. F

3. F

7. I

10. I

4. O

129. During the year, Ollie's Outdoor Outfitters issued 20,000 shares of common stock in exchange for a prime

piece of land. Two employees of the accounting department, Audrey and Neil, disagree as to the appearance of

this particular transaction on the statement of cash flows. Audrey believes it to be a significant noncash

transaction, and it therefore should be presented as such at the bottom of the statement. Neil contends that

because this transaction did not cause any cash to flow in or out of the company, it has no place on the

statement of cash flows. Who is correct and why?

Audrey is correct in her contention that the issuance of stock in exchange for land represents a significant

noncash transaction and therefore should be disclosed in a separate schedule as part of the statement of cash

flows. Usually, a transaction involving either part of this event would affect cash and would be included in the

body of the cash flow statement. Because the movement of such items significantly affects the makeup of the

balance sheet and income statement, adequate disclosure is necessary.

130. When preparing a statement of cash flows using the indirect method, why is depreciation added back to net

income within the operating activities section?

131. How is it possible for a company to show a net loss for a given year, yet produce positive net cash flows

from operating activities?

132. Green Skies Company prepares its statement of cash flows using the indirect method. Indicate whether

1. –

6. –

2. +

7. +

3. +

8. +

4. +

9. –

5. +

10. –

133. Houston Shoe Co. is preparing a statement of cash flows using the indirect method. Indicate on the blanks

1. O

7. O

2. O

8. NA

3. N

9. F

4. I

10. NA

5. F

11. I O*

6. F

12. O

134. Marla Co. sells equipment with a carrying value of $90,000 for $70,000. Where, and for what amounts,

would this transaction appear on a statement of cash flows using the indirect method?

135. Give two explanations for why the amount of cash outflow for equipment for the year might not equal the

increase in the Equipment account balance from one balance sheet date to the next.

1. Some equipment owned at the beginning of the year was disposed of during the year. This would offset some

2. Some acquisitions of equipment may have been made for something other than cash. Other consideration

3. Some acquisitions of equipment may have been made by giving a down payment in cash and a promissory

136. Which accounts are analyzed to determine cash flows from financing activities?

137. What elements are used to calculate free cash flow? Indicate whether the element is added or subtracted.

138. What does it mean when a company has positive free cash flow? What does it mean when a company has

negative free cash flow?

139.

4. A type of marketable security that a company buys and sells

5. The amount of cash that remains after deducting the funds a

140. Using the indirect method, calculate the amount of net cash flows from operating activities from the

following data. Show your work

141. Using the indirect method, calculate the amount of net cash flows from operating activities from the

following data. Show your work.

Net Income

$51,000

Beginning Accounts Payable

$ 3,000

Beginning Accounts

Ending Accounts Payable

2,800

Receivable

5,000

Depreciation Expense

10,200

Ending Accounts Receivable

4,400

Amortization of Intangible

142. Following are the income statement and other information for Zambrano Corporation.

Zambrano Corporation

Income Statement

For the Year Ended December 31, 20x5

Sales

$6,000

Cost of goods sold

3

,

0

0

0

Gross margin

$

3

,

0

0

0

Operating expenses

$1,200

Depreciation expense

600

1

,

8

0

0

Income before income taxes

$

1

,

2

0

0

Income taxes expense

3

0

0

Net income

$

9

0

0

Accounts receivable (net) decreased by $1,500 during the year. Inventory increased by $900, and Accounts Payable decreased by $1,200 during the

year. Income Taxes Payable increased by $300 during the year.

Prepare a schedule of cash flows from operating activities using the indirect method.

a.

Cash

flow

s

from

oper

ating

activ

ities:

Net

inco

me

$900

Adju

stme

Decr

(1,200)

143. Following are the income statement and other information for American Horse Corporation.

American Horse Corporation

Income Statement

For the Year Ended December 31, 20x5

Sales

$6,000

Cost of goods sold

3

,

0

0

0

Gross margin

$

3

,

0

0

0

Operating expenses

$1,200

Depreciation expense

600

1

,

8

0

0

Income before income taxes

$

1

,

2

0

0

Income taxes expense

3

0

0

Net income

$

9

0

0

Accounts receivable (net) increased by $1,500 during the year. Inventory decreased by $1,900, and Accounts Payable increased by $1,200 during the

year. Income Taxes Payable decreased by $300 during the year.

Prepare a schedule of cash flows from operating activities using the indirect method.

a.

Cash

flows

from

operat

ing

activit

ies:

Net

incom

e

$900

Adjust

Incr

1,200

144. The following comparative balance sheet and other information relate to Carlson Company.

Carlson Company

Comparative Balance Sheets

December 31, 20x5 and 20x4

Assets

20x5

20x4

Cash

$ 140

$ 140

Accounts receivable (net)

210

280

Inventory

350

420

Prepaid expenses

105

70

Equipment (net)

3,010

2,800

Investments and other assets

4,900

4,200

Total assets

$8,715

$7,910

Liabilities and Stockholders' Equity

Accounts payable

$ 350

$ 280

Income taxes payable

70

140

Long-term note payable

2,100

1,400

Common stock

1,400

1,400

Retained earnings

4,795

4,690

Total liabilities and stockholders' equity

$8,715

$7,910

Additional information:

Depreciation expense $560

Cash dividends declared and paid 50

a. Compute net income, assuming net income and the cash dividends were the only items affecting retained earnings. Show your work.

b. Compute net cash flows from operating activities using the indirect method.

a.

Net

incom

e:

Increa

se in

retaine

d

earnin

gs

$10

5

Divide

nds

50

Net

incom

e

$15

5

b.

Cash

flows

from

operati

ng

activiti

es:

Net

incom

e

$15

5

Adjust

Increa

(35)

145. Ralston Company's cash balance at December 31, 20x5, was $23,000. During the year, Ralston sold assets

with a book value of $245,000 that resulted in a loss of $110,000. Calculate the company's cash balance at

December 31, 20x6 , given the following information for the year ended December 31, 20x6. Show your work.

Net Income

$470,000

Depreciation and Amortization Expense

88,000

Decrease in Accounts Receivable (net)

14,000

Decrease in Inventory

25,000

Increase in Accounts Payable

20,000

Net Cash Flows from Investing Activities

??

Net Cash Flows from Financing Activities

(400,000)

Net Income

$470,000

146. The activity in the Plant Assets and related Accumulated Depreciation accounts for 20x5 is shown below.

In addition, the income statement shows a gain on sale of plant assets of $16,000.

Plant Assets

Accumulated Depreciation

20x5 Beginning balance

$234,000

$124,000

20x5 Purchases

120,000

20x5 Depreciation

36,000

20x5 Disposals

(82,000)

(26,000)

20x5 Ending balance

$272,000

$134,000

Based on the information given, compute the amounts to be shown and indicate how they would appear on the statement of cash flows. Assume that

the indirect method is being used and that the plant assets were purchased for cash.

20x5 depreciation expense of $36,000 is added to net income to arrive at net cash flows from operating

activities. The gain, however, should be deducted from net income in the operating activities section.

147. The activity from the Long-Term Investments account for Fisk Corporation appears below. In addition, the

income statement shows a loss on the sale of investments of $32,000.

Long-Term Investments

Beginning balance, 20x5

$184,000

Purchases

278,000

Sales

(202,000)

148. The following 20x5 information relates to Taylor, Inc.:

Net Income

$365,000

Depreciation Expense

96,000

Amortization of Intangible Assets

11,000

Beginning Accounts Receivable

420,000

Ending Accounts Receivable

439,000

Beginning Inventory

516,000

Ending Inventory

560,000

Beginning Prepaid Expenses

48,000

Ending Prepaid Expenses

42,000

Beginning Accounts Payable

119,000

Ending Accounts Payable

146,000

Purchase of Long-Term Assets for Cash

616,000

Cash from Issuance of Long-Term Debt

200,000

Issuance of Stock for Cash

160,000

Issuance of Stock for Long-Term Assets

110,000

Purchase of Treasury Stock

64,000

Sale of Long-Term Investment at Cost

39,000

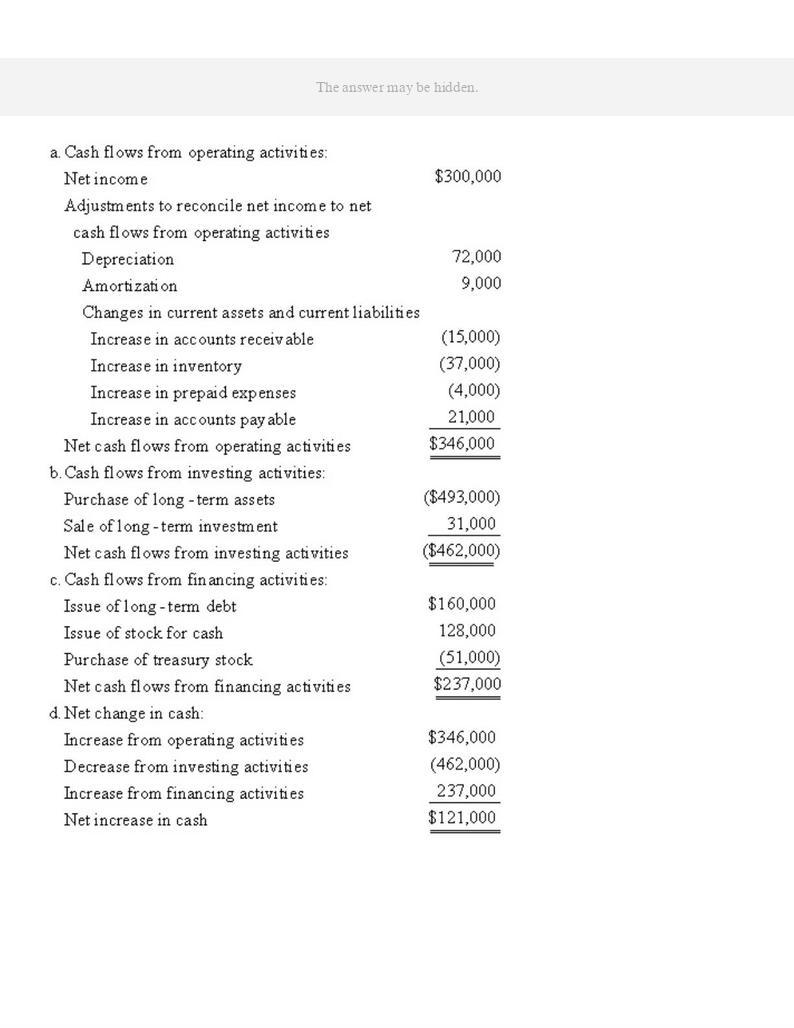

149. The following information relates to Royale Enterprises for the year ended December 31, 20x5:

Net Income

$300,000

Depreciation Expense

72,000

Amortization of Intangible Assets

9,000

Beginning Accounts Receivable

336,000

Ending Accounts Receivable

351,000

Beginning Inventory

413,000

Ending Inventory

450,000

Beginning Prepaid Expenses

34,000

Ending Prepaid Expenses

38,000

Beginning Accounts Payable

95,000

Ending Accounts Payable

116,000

Purchase of Long-Term Assets for Cash

493,000

Cash from Issuance of Long-Term Debt

160,000

Issuance of Stock for Cash

128,000

Issuance of Stock for Long-Term Assets

88,000

Purchase of Treasury Stock

51,000

Sale of Long-Term Investment at Cost

31,000

150. The following information relates to Ferguson Company for 20x6 and 20x5:

Ferguson Company

Comparative Balance Sheets

December 31, 20x6 and 20x5

Assets

20x6

20x5

Change

Cash

$ 21,000

$ 54,000

($ 33,000)

Accounts receivable (net)

421,000

480,000

(59,000)

Inventory

310,000

340,000

(30,000)

Prepaid expenses

17,000

15,000

2,000

Investments

80,000

80,000

0

Land

350,000

300,000

50,000

Building (net)

680,000

700,000

(20,000)

Equipment (net)

520,000

340,000

180,000

Total assets

$2,399,000

$2,309,000

$ 90,000

Liabilities

Accounts payable

$ 328,000

$ 335,000

($ 7,000)

Accrued liabilities

171,000

170,000

1,000

Income taxes payable

22,000

34,000

(12,000)

Bonds payable

410,000

700,000

(290,000)

Long-term note payable

130,000

0

130,000

Total liabilities

$1,061,000

$1,239,000

($178,000)

Stockholders' Equity

Common stock

$ 800,000

$ 600,000

$200,000

Additional paid-in capital

152,000

152,000

0

Retained earnings

386,000

318,000

68,000

Total stockholders' equity

$1,338,000

$1,070,000

$268,000

Total liabilities and stockholders' equity

$2,399,000

$2,309,000

$ 90,000

Additional information:

Net income for 20x6 was $143,000.

Issued a long-term note payable in exchange for computer equipment for $130,000.

Purchased computer terminals for $90,000.

Depreciation on equipment for 20x6 was $40,000.

Depreciation on building for 20x6 was $20,000.

Reacquired bonds payable at par for $290,000.

Declared and paid dividends of $75,000.

Issued 20,000 shares of common stock at par value of $10 per share.

Paid $50,000 for land intended for a new plant site.

Prepare a statement of cash flows using the indirect method. Include a schedule of noncash investing and financing transactions, if applicable.

Ferguson Company

Statement of Cash Flows

For the Year Ended December 31, 20x6

Ferg

uson

Com

pany

State

ment

of

Cash

Flow

s

Net

$272,000

Cash

54,0

151. Use the following data for Jenkins Co. to prepare a statement of cash flows using the indirect method for

the year ended June 30, 20x6.

Jenk

ins

Co.

Inco

me

State

ment

For

the

Year

Ende

d

June

30,

20x6

Sales

$700,000

Less

expe

nses

Cost of goods sold

$400,000

Depreciation expense

40,000

Administrative expenses

104,000

Selling expenses

70,000

Loss on sale of investment

1,000

6

1

5

,

0

0

0

Inco

me

befor

e

inco

me

taxes

$ 85,000

Inco

me

taxes

expe

nse

20,000

Net

inco

me

$ 65,000

Jenkins Co.

Comparative Balance Sheets

June 30, 20x6 and 20x5

Assets

20x6

20x5

Cash

$ 9,000

$ 30,000

Accounts receivable (net)

70,000

55,000

Inventory

80,000

100,000

Prepaid insurance

6,000

5,000

Long-term investments

40,000

50,000

Plant and equipment

160,000

80,000

Accumulated depreciation

(40,000)

(24,000)

Total assets

$325,000

$296,000

Liabilities

Accounts payable

$ 4,000

$ 12,000

Wages payable

440

520

Income taxes payable

1,560

1,480

Notes payable

40,000

24,000

Total liabilities

$ 46,000

$ 38,000

Stockholders' Equity

Common stock

$ 116,000

$ 130,000

Retained earnings

163,000

128,000

Total stockholders' equity

$279,000

$258,000

Total liabilities and stockholders' equity

$325,000

$296,000

Additional information:

A plant asset costing $40,000 was sold for its book value of $16,000.

A long-term investment was sold for $9,000.

The outstanding notes are long-term. A $16,000 note was issued during 20x6 .

Jenkins Co.

Statement of Cash Flows

For the Year Ended June 30, 20x6

Jenk

ins

Co.

State

ment

of

Cash

Flow

s

For

the

Year

Ende

d

June

30,

20x6

Cash

flows

from

opera

ting

activi

ties

Net

income

$65,000

Adjust

ments

to

Net

$102,000

Net

($21,0

152. Use the following data for Window Rock Company to prepare a statement of cash flows using the indirect

method for the year ended June 30, 20x6.

Win

dow

Rock

Com

pany

Inco

me

State

ment

For

the

Year

Ende

d

June

30,

20x6

Sales

$1,400,000

Less

expe

nses

Cost of goods sold

$800,000

Depreciation expense

80,000

Administrative expenses

208,000

Selling expenses

140,000

Loss on sale of investment

2,000

1

,

2

3

0

,

0

0

0

Inco

me

befor

e

inco

me

taxes

170,000

Inco

me

taxes

expe

nse

40,000

Net

inco

me

$ 130,000

Window Rock Company

Comparative Balance Sheets

June 30, 20x6 and 20x5

Assets

20x6

20x5

Cash

$ 18,000

$ 60,000

Accounts receivable (net)

140,000

110,000

Inventory

160,000

200,000

Prepaid insurance

12,000

10,000

Long-term investments

80,000

100,000

Plant and equipment

320,000

160,000

Accumulated depreciation

(80,000)

(48,000)

Total assets

$650,000

$592,000

Liabilities

Accounts payable

$ 8,000

$ 24,000

Wages payable

880

1,040

Income taxes payable

3,120

2,960

Notes payable

80,000

48,000

Total liabilities

$ 92,000

$ 76,000

Stockholders' Equity

Common stock

$ 232,000

$260,000

Retained earnings

326,000

256,000

Total stockholders' equity

$558,000

$516,000

Total liabilities and stockholders' equity

$650,000

$592,000

Additional information:

A plant asset costing $80,000 was sold for its book value of $32,000.

A long-term investment was sold for $18,000.

The outstanding notes are long-term. A $32,000 note was issued during 20x6.

Window Rock Company

Statement of Cash Flows

For the Year Ended June 30, 20x6

Win

dow

Rock

Com

pany

State

ment

of

Cash

Flow

s

For

the

Year

Ende

d

June

30,

20x6

Cash

flows

from

opera

ting

activi

ties

Net

income

$130,000

Net

$204,000

Net

($42,00

153. For 20x5, Sahara Company had average total assets of $520,000, sales of $450,000, net income of

$50,000, net cash flows from operating activities of $75,000, dividend payments of $25,000, purchases of plant

assets of $60,000, and sales of plant assets of $55,000. Using this information, compute (a) cash flow yield, (b)

cash flows to sales, (c) cash flows to assets, and (d) free cash flow. Round amounts to one decimal place.

a. 1.5 times ($75,000 $50,000)

b. 16.7 percent ($75,000 $450,000)

c. 14.4 percent ($75,000 $520,000)

d. $45,000 ($75,000 – $25,000 – $60,000 + $55,000)

154. For 20x5, Devers Enterprises had average total assets of $1,040,000, sales of $900,000, net income of

$100,000, net cash flows from operating activities of $150,000, dividend payments of $50,000, purchases of

plant assets of $120,000, and sales of plant assets of $110,000. Using this information, compute (a) cash flow

yield, (b) cash flows to sales, (c) cash flows to assets, and (d) free cash flow. Round amounts to one decimal

place.

a. 1.5 times ($150,000 $100,000)

b. 16.7 percent ($150,000 $900,000)

c. 14.4 percent ($150,000 $1,040,000)

d. $90,000 ($150,000 – $50,000 – $120,000 + $110,000)

155. Use the following information to obtain the ratios below. Round amounts to one decimal place

Net cash flows from operating activities

$837 million

Net income

465 million

Sales

6,750 million

Average total assets

7,150 million

Dividends

105 million

Purchases of plant assets

170 million

Sales of plant assets

380 million

a. 1.8 times ($837 $465)

b. 12.4% ($837 $6,750)

c. 11.7% ($837 $7,150)

d. $942 million ($837 – $105 – $170 + $380)