Chapter 15--Capital Investment Analysis

Student: ___________________________________________________________________________

1. The process by which management plans, evaluates, and controls long-term investment decisions involving

2. The process by which management plans, evaluates, and controls long- term investment decisions involving

3. Care must be taken while making capital investment decisions since it involves a long-term commitment of

4. The methods of evaluating capital investment proposals can be grouped into two general categories: (1)

5. The methods of evaluating capital investment proposals can be grouped into two general categories: (1)

9. If the average rate of return on an asset exceeds the minimum rate of return for investments, the asset should

10. The excess of cash flowing in from revenues over the cash flowing out for expenses is termed net cash

11. The excess of cash flowing in from revenues over the cash flowing out for expenses is termed net

12. The anticipated purchase of a fixed asset for $400,000, with a useful life of 5 years and no residual value, is

expected to yield total net income of $200,000 for 5 years. The expected average rate of return on investment

13. When evaluating a proposal by use of the net present value method, if there is a deficiency of the present

14. The anticipated purchase of a fixed asset for $400,000, with a useful life of 5 years and no residual value, is

15. The anticipated purchase of a fixed asset for $400,000, with a useful life of 5 years and a $40,000 residual

value, is expected to yield total net income of $200,000 for 5 years. The expected average rate of return on

16. The anticipated purchase of a fixed asset for $400,000, with a useful life of 5 years and a $40,000 residual

17. The computations required for the net present value method are less than those the computation required for

18. The computations required for the net present value method are more than the computation required for the

19. If a proposed expenditure of $80,000 for a fixed asset with a 4-year life has an annual expected net cash

20. For years one through five, a proposed expenditure of $250,000 for a fixed asset with a 5-year life has

expected net income of $40,000, $35,000, $25,000, $25,000, and $25,000, respectively, and net cash flows of

22. The average rate of return method of capital investment analysis gives consideration to the present value of

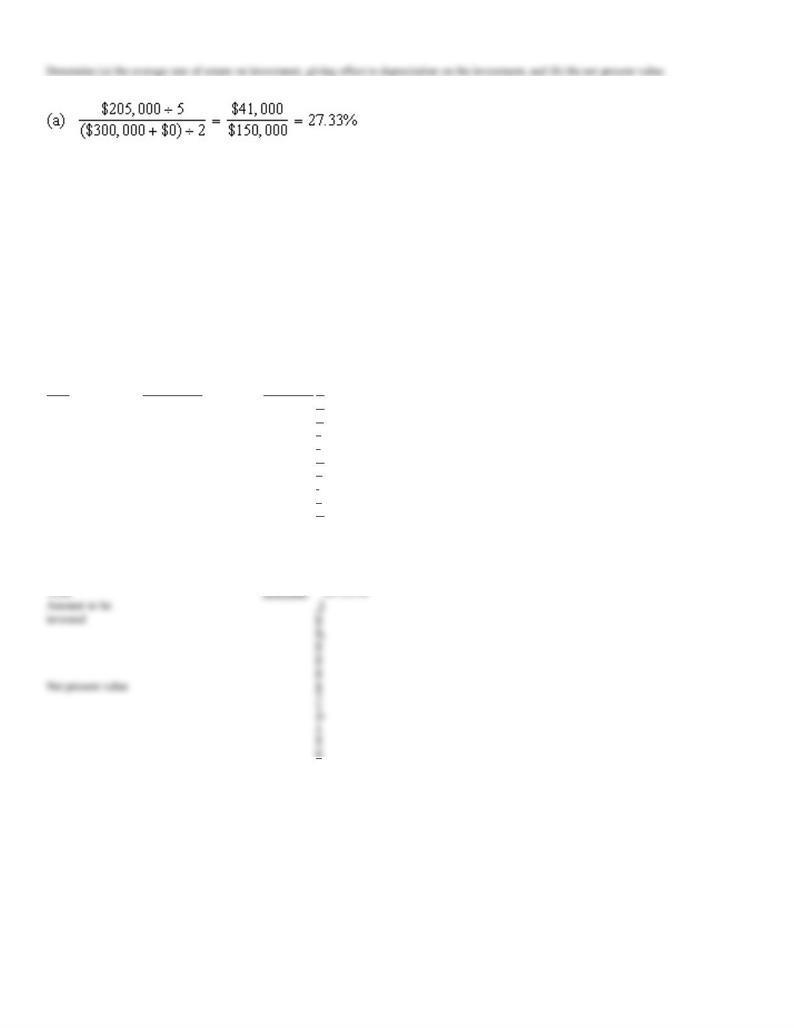

23. The anticipated purchase of a fixed asset for $400,000 with a useful life of 5 years and no residual value is

expected to yield total income of $150,000 (recognition is given to the effect of straight-line depreciation on the

24. The expected period of time that will elapse between the date of a capital investment and the complete

25. The expected period of time that will elapse between the date of a capital investment and the complete

26. If a proposed expenditure of $400,000 for a fixed asset with a 4-year life has an annual expected net cash

27. When evaluating a proposal by use of the cash payback method, if net cash flows exceed the capital

28. When evaluating a proposal by use of the net present value method, if there is an excess of the present value

of future cash inflows over the amount to be invested, the rate of return on the proposal is less than the rate used

29. When evaluating a proposal by use of the net present value method, if there is an excess of the present value

of future cash inflows over the amount to be invested, the rate of return on the proposal exceeds the rate used in

30. In net present value analysis for a proposed capital investment, the expected future net cash flows are

31. When evaluating a proposal by use of the net present value method, if the present value is less than the

32. For years one through five, a proposed expenditure of $400,000 for a fixed asset with a 5-year life has

expected net income of $50,000, $40,000, $20,000, $20,000, and $20,000, respectively, and net cash flows of

33. A present value index can be used to rank competing capital investment proposals when the net present

34. The internal rate of return method of analyzing capital investment proposals uses the present value concept

37. Qualitative considerations in capital investment decisions are most appropriate for strategic investments or

41. When evaluating two competing proposals with unequal lives, management should give greater

consideration to the investment with the longer life because the asset will be useful to the company for a longer

42. Leasing assets may be a favorable alternative to purchasing assets if the asset has a high risk of becoming

43. The process by which management allocates available investment funds among competing capital

44. The process by which management allocates available investment funds among competing capital

46. In capital rationing, alternative proposals are initially screened by establishing minimum standards using

47. The process by which management plans, evaluates, and controls long-term investment decisions involving

48. Decisions to install new equipment, replace old equipment, and purchase or construct a new building are

50. By converting dollars to be received in the future into current dollars, the present value methods take into

51. The primary advantages of the average rate of return method of analyzing a capital investment proposal are

52. An anticipated purchase of equipment for $1,200,000, with a useful life of 8 years and no residual value, is

expected to yield the following annual net incomes and net cash flows:

Year

Net Income

Net Cash

Flow

1

$180,000

$330,000

2

170,000

320,000

3

130,000

280,000

4

120,000

270,000

5

50,000

200,000

6

50,000

200,000

7

50,000

200,000

8

50,000

200,000

53. Which of the following can be used to place capital investment proposals involving different amounts of

54. Using the following partial table of present value of $1 at compound interest, compute the present value of

$20,000 (rounded to nearest dollar) to be received one year from today, assuming an earnings rate of 15%.

1

0.909

0.870

0.833

2

0.826

0.756

0.694

3

0.751

0.658

0.579

4

0.683

0.572

0.482

5

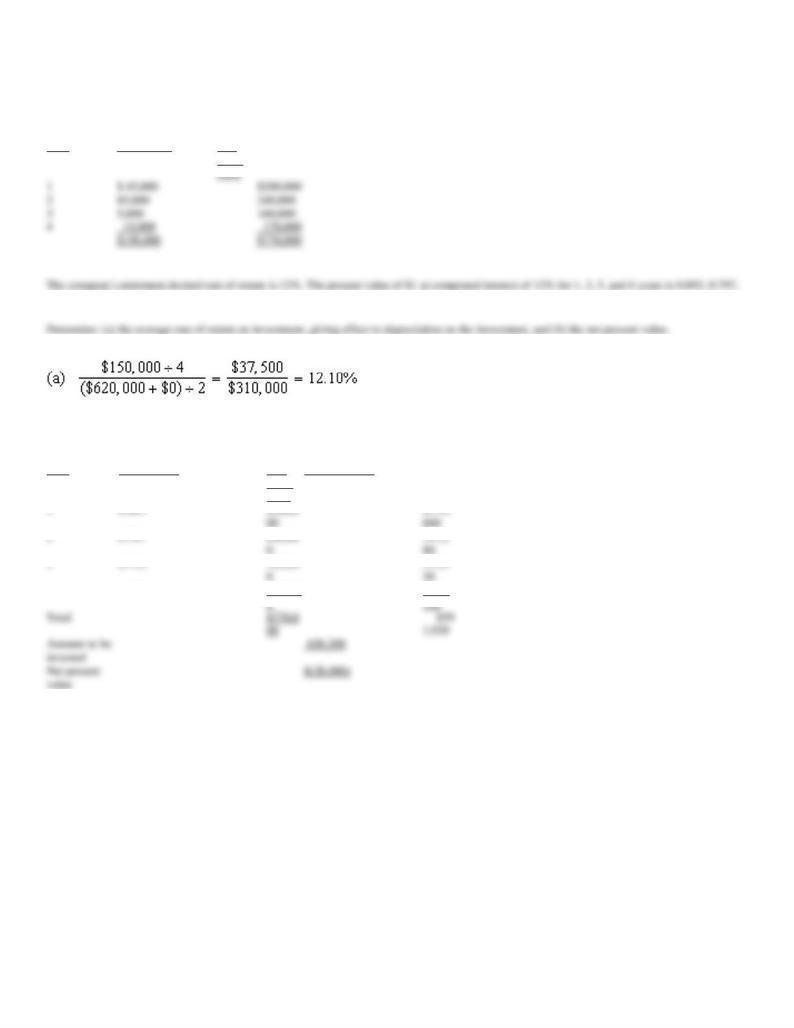

0.621

0.497

0.402

6

0.564

0.432

0.335

7

0.513

0.376

0.279

55. An analysis of a proposal by the net present value method indicated that the present value exceeded the

56. In general, present value methods of analyzing capital investments are more desirable than methods

57. Which method of evaluating capital investment proposals uses the concept of present value to compute a

58. The rate of return is 10% and the cash to be received in one year is $10,000. Determine the present value

amount, using the following partial table of present value of $1 at compound interest:

1

0.943

0.909

0.893

2

0.890

0.826

0.797

3

0.840

0.751

0.712

4

0.792

0.683

0.636

59. Using the following partial table of present value of $1 at compound interest, determine the present value of

$20,000 to be received four years hence with earnings at the rate of 12% a year:

1

0.943

0.909

0.893

2

0.890

0.826

0.797

3

0.840

0.751

0.712

4

0.792

0.683

0.636

60. When several alternative investment proposals of the same amount are being considered, the one with the

largest net present value is the most desirable. If the alternative proposals involve different amounts of

61. Which method of evaluating capital investment proposals uses present value concepts to compute the rate of

64. Crane Company is considering the acquisition of a machine that costs $60,000. The machine is expected to

have a useful life of 5 years, a negligible residual value, an annual cash flow of $15,000, and annual operating

65. The expected average rate of return for a proposed investment of $3,000,000 in a fixed asset giving effect to

depreciation (straight-line method) with a useful life of 20 years, no residual value, and an expected total

67. The management of Hence Corporation is considering the purchase of a new machine costing $200,000.

The company's desired rate of return is 10%. The present value factors for $1 at compound interest of 10% for 1

through 5 years are 0.909, 0.826, 0.751, 0.683, and 0.621, respectively. In addition to the foregoing information,

use the following data in determining the acceptability in this situation:

Income from

Net

Cash

Year

Operations

Flow

1

$50,000

$90,000

2

20,000

60,000

3

10,000

50,000

4

5,000

45,000

5

5,000

45,000

68. The management of Hence Corporation is considering the purchase of a new machine costing $200,000.

The company's desired rate of return is 10%. The present value factors for $1 at compound interest of 10% for 1

through 5 years are 0.909, 0.826, 0.751, 0.683, and 0.621, respectively. In addition to the foregoing information,

use the following data in determining the acceptability in this situation:

Income from

Net

Cash

Year

Operations

Flow

A. 18%.

B. 16%.

C. 58%.

D. 20%.

69. The management of Hence Corporation is considering the purchase of a new machine costing $200,000.

The company's desired rate of return is 10%. The present value factors for $1 at compound interest of 10% for 1

through 5 years are 0.909, 0.826, 0.751, 0.683, and 0.621, respectively. In addition to the foregoing information,

use the following data in determining the acceptability in this situation:

Income from

Net

Cash

Year

Operations

Flow

A. positive $24,960.

B. negative $27,600.

C. positive $27,600.

D. negative $24,960.

70. The management of Hence Corporation is considering the purchase of a new machine costing $200,000.

The company's desired rate of return is 10%. The present value factors for $1 at compound interest of 10% for 1

through 5 years are 0.909, 0.826, 0.751, 0.683, and 0.621, respectively. In addition to the foregoing information,

use the following data in determining the acceptability in this situation:

Income from

Net

Cash

Year

Operations

Flow

A. 0.88.

B. 1.45.

C. 1.14.

D. 0.70.

71. The management of London Corporation is considering the purchase of a new machine costing $750,000.

The company's desired rate of return is 6%. The present value factors for $1 at compound interest of 6% for 1

through 5 years are 0.943, 0.890, 0.840, 0.792, and 0.747, respectively. In addition to this information, use the

following data in determining the acceptability in this situation:

Income from

Net

Cash

Year

Operations

Flow

A. 3 years.

B. 5 years.

C. 20 years.

D. 4 years.

72. The management of London Corporation is considering the purchase of a new machine costing $750,000.

The company's desired rate of return is 6%. The present value factors for $1 at compound interest of 6% for 1

through 5 years are 0.943, 0.890, 0.840, 0.792, and 0.747, respectively. In addition to this information, use the

following data in determining the acceptability in this situation:

Income from

Net

Cash

Year

Operations

Flow

A. 5%.

B. 10%.

C. 25%.

D. 15%.

73. The management of London Corporation is considering the purchase of a new machine costing $750,000.

The company's desired rate of return is 6%. The present value factors for $1 at compound interest of 6% for 1

through 5 years are 0.943, 0.890, 0.840, 0.792, and 0.747, respectively. In addition to this information, use the

following data in determining the acceptability in this situation:

Income from

Net

Cash

Year

Operations

Flow

A. positive $39,750.

B. positive $118,145.

C. negative $118,145.

D. negative $39,750.

74. The management of London Corporation is considering the purchase of a new machine costing $750,000.

The company's desired rate of return is 6%. The present value factors for $1 at compound interest of 6% for 1

through 5 years are 0.943, 0.890, 0.840, 0.792, and 0.747, respectively. In addition to this information, use the

following data in determining the acceptability in this situation:

Income from

Net

Cash

Year

Operations

Flow

1

$37,500

$187,500

2

37,500

187,500

3

37,500

187,500

4

37,500

187,500

5

37,500

187,500

76. The expected average rate of return for a proposed investment of $540,000 in a fixed asset, with a useful life

of four years, recognition is given to the effect of straight-line depreciation on the investment, no residual value,

77. The amount of the average investment for a proposed investment of $70,000 in a fixed asset, with a useful

life of four years, recognition is given to the effect of straight-line depreciation on the investment, no residual

78. The amount of the estimated average income for a proposed investment of $60,000 in a fixed asset, giving

effect to depreciation (straight-line method), with a useful life of four years, no residual value, and an expected

79. Assuming that the desired rate of return is 6%, determine the present value of $10,000 to be received in one

year, using the following partial table of present value of $1 at compound interest.

1

0.943

0.909

0.893

2

0.890

0.826

0.797

3

0.840

0.751

0.712

4

0.792

0.683

0.636

80. Using the following partial table of present value of $1 at compound interest, determine the present value of

$20,000 to be received four years hence, with earnings at the rate of 10% a year.

1

0.943

0.909

0.893

2

0.890

0.826

0.797

3

0.840

0.751

0.712

4

0.792

0.683

0.636

81. Using the following partial table of present value of $1 at compound interest, determine the present value of

$20,000 to be received three years hence, with earnings at the rate of 10% a year.

1

0.943

0.909

0.893

2

0.890

0.826

0.797

3

0.840

0.751

0.712

4

0.792

0.683

0.636

82. If the rate of earnings is 10% and the cash to be received in two years is $10,000, determine the present

value amount, using the following partial table of present value of $1 at compound interest.

1

0.943

0.909

0.893

2

0.890

0.826

0.797

3

0.840

0.751

0.712

4

0.792

0.683

0.636

86. Which of the following provisions of the Internal Revenue Code can be used to reduce the amount of the

87. Assume in analyzing alternative proposals that Proposal F has a useful life of six years and Proposal J has a

89. The process by which management allocates available investment funds among competing investment

90. In capital rationing, an initial screening of alternative proposals is usually performed by establishing

91. In capital rationing, alternative proposals that survive initial screening and further analysis using present

92. Mars Corp. is choosing between two different capital investment proposals. Machine A has a useful life of 4

1

0.909

2

0.826

3

0.751

4

0.683

5

0.621

6

0.513

Machine A will generate net cash flow of $70,000 in each of the four years. Machine B will generate $80,000 in year 1, $70,000 in year 2, $60,000 in

year 3, and $40,000 per year for the remaining 3 years of its useful life.

94. A 5-year project is estimated to cost $700,000 and have no residual value. If the straight-line depreciation

95. Both proposal M, and N cost $800,000, have a 6-year life, and have expected total cash flows of

96. A $350,000 capital investment proposal has an estimated life of four years and no residual value. The

estimated net cash flows are as follows:

97. Heedy Inc. is considering a capital investment proposal that costs $460,000 and has an estimated life of four

years, and no residual value. The estimated net cash flows are as follows:

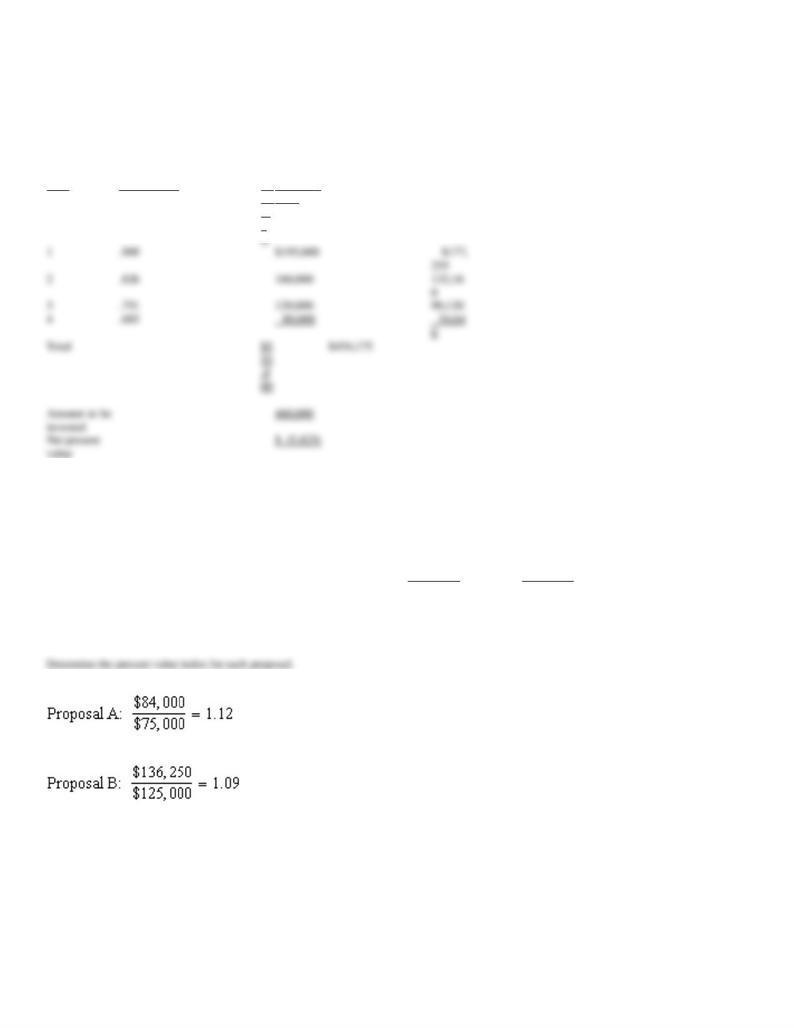

98. The net present value has been computed for Proposals A and B. Relevant data are as follows:

Proposal A

Proposal B

Amount to be invested

$75,000

$125,000

Total present value of net cash flow

84,000

136,250

Net present value

9,000

11,250

99. Sommers Company is evaluating a project requiring a capital expenditure of $300,000. The project has an

estimated life of 5 years and no salvage value. The estimated net income and net cash flow from the project are

as follows:

Year

Net Income

Net Cash

Flow

1

$ 60,000

$120,000

1

0.893

2

0.797

3

0.712

4

0.636

5

0.567

100. June Co. is evaluating a project requiring a capital expenditure of $620,000. The project has an estimated

life of four years and no salvage value. The estimated net income and net cash flow from the project are as

follows:

Year

Net Income

Net

Cash

0.712, and 0.636, respectively.

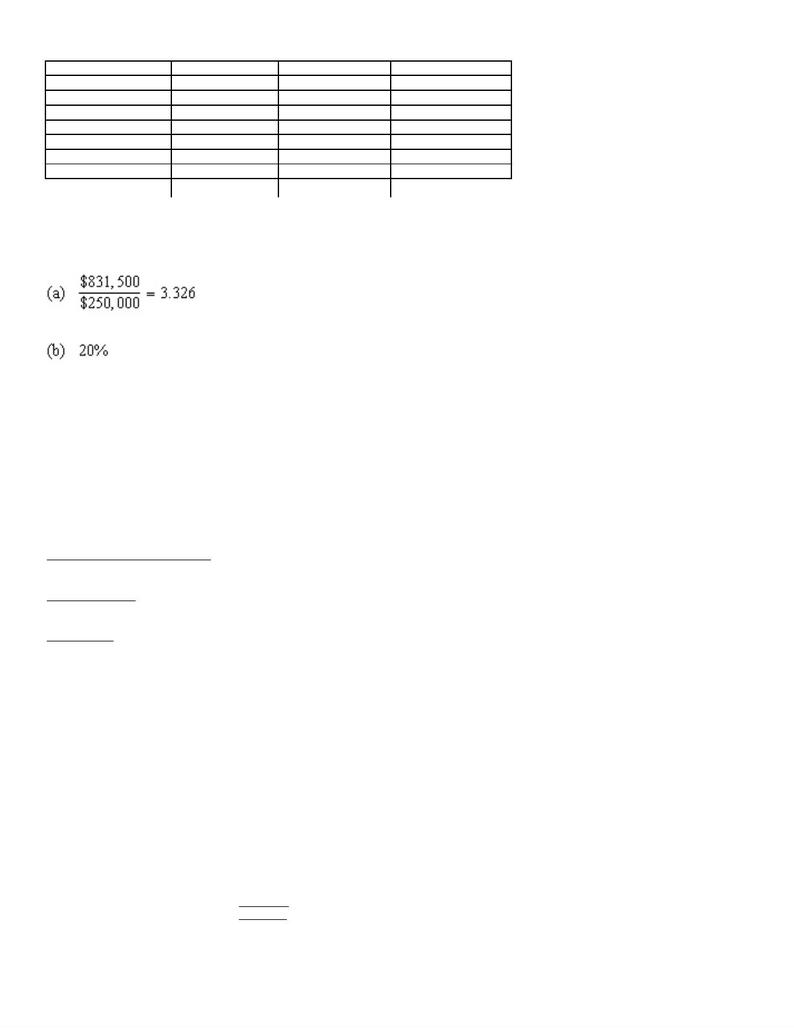

101. The internal rate of return method is used to analyze a $831,500 capital investment proposal with annual

net cash flows of $250,000 for each of the six years of its useful life.

1

0.909

0.870

0.833

2

1.736

1.626

1.528

3

2.487

2.283

2.106

4

3.170

2.855

2.589

5

3.791

3.353

2.991

6

4.355

3.785

3.326

7

4.868

4.160

3.605

102. Harris Co. is considering a 12-year project that is estimated to cost $900,000 and has no residual value.

103. Proposals L and K each cost $500,000, have 6-year lives, and have expected total cash flows of $750,000.

Proposal L is expected to provide equal annual net cash flows of $125,000, while the net cash flows for

Proposal K are as follows:

Year 1

$250,000

Year 2

200,000

Year 3

100,000

Year 4

90,000

Year 5

60,000

Year 6

50,000

$750,000

Determine the cash payback period for each proposal.

Chapter 15--Capital Investment Analysis Key

1. The process by which management plans, evaluates, and controls long-term investment decisions involving

2. The process by which management plans, evaluates, and controls long- term investment decisions involving

3. Care must be taken while making capital investment decisions since it involves a long-term commitment of

4. The methods of evaluating capital investment proposals can be grouped into two general categories: (1)

5. The methods of evaluating capital investment proposals can be grouped into two general categories: (1)

9. If the average rate of return on an asset exceeds the minimum rate of return for investments, the asset should

10. The excess of cash flowing in from revenues over the cash flowing out for expenses is termed net cash

11. The excess of cash flowing in from revenues over the cash flowing out for expenses is termed net

12. The anticipated purchase of a fixed asset for $400,000, with a useful life of 5 years and no residual value, is

expected to yield total net income of $200,000 for 5 years. The expected average rate of return on investment

13. When evaluating a proposal by use of the net present value method, if there is a deficiency of the present

14. The anticipated purchase of a fixed asset for $400,000, with a useful life of 5 years and no residual value, is

15. The anticipated purchase of a fixed asset for $400,000, with a useful life of 5 years and a $40,000 residual

value, is expected to yield total net income of $200,000 for 5 years. The expected average rate of return on

16. The anticipated purchase of a fixed asset for $400,000, with a useful life of 5 years and a $40,000 residual

17. The computations required for the net present value method are less than those the computation required for

18. The computations required for the net present value method are more than the computation required for the

19. If a proposed expenditure of $80,000 for a fixed asset with a 4-year life has an annual expected net cash

20. For years one through five, a proposed expenditure of $250,000 for a fixed asset with a 5-year life has

expected net income of $40,000, $35,000, $25,000, $25,000, and $25,000, respectively, and net cash flows of

22. The average rate of return method of capital investment analysis gives consideration to the present value of

23. The anticipated purchase of a fixed asset for $400,000 with a useful life of 5 years and no residual value is

expected to yield total income of $150,000 (recognition is given to the effect of straight-line depreciation on the

24. The expected period of time that will elapse between the date of a capital investment and the complete

25. The expected period of time that will elapse between the date of a capital investment and the complete

26. If a proposed expenditure of $400,000 for a fixed asset with a 4-year life has an annual expected net cash

27. When evaluating a proposal by use of the cash payback method, if net cash flows exceed the capital

28. When evaluating a proposal by use of the net present value method, if there is an excess of the present value

of future cash inflows over the amount to be invested, the rate of return on the proposal is less than the rate used

29. When evaluating a proposal by use of the net present value method, if there is an excess of the present value

of future cash inflows over the amount to be invested, the rate of return on the proposal exceeds the rate used in

30. In net present value analysis for a proposed capital investment, the expected future net cash flows are

31. When evaluating a proposal by use of the net present value method, if the present value is less than the

32. For years one through five, a proposed expenditure of $400,000 for a fixed asset with a 5-year life has

expected net income of $50,000, $40,000, $20,000, $20,000, and $20,000, respectively, and net cash flows of

33. A present value index can be used to rank competing capital investment proposals when the net present

34. The internal rate of return method of analyzing capital investment proposals uses the present value concept

37. Qualitative considerations in capital investment decisions are most appropriate for strategic investments or

41. When evaluating two competing proposals with unequal lives, management should give greater

consideration to the investment with the longer life because the asset will be useful to the company for a longer

42. Leasing assets may be a favorable alternative to purchasing assets if the asset has a high risk of becoming

43. The process by which management allocates available investment funds among competing capital

44. The process by which management allocates available investment funds among competing capital

46. In capital rationing, alternative proposals are initially screened by establishing minimum standards using

47. The process by which management plans, evaluates, and controls long-term investment decisions involving

48. Decisions to install new equipment, replace old equipment, and purchase or construct a new building are

50. By converting dollars to be received in the future into current dollars, the present value methods take into

51. The primary advantages of the average rate of return method of analyzing a capital investment proposal are

52. An anticipated purchase of equipment for $1,200,000, with a useful life of 8 years and no residual value, is

expected to yield the following annual net incomes and net cash flows:

Year

Net Income

Net Cash

Flow

1

$180,000

$330,000

2

170,000

320,000

3

130,000

280,000

4

120,000

270,000

5

50,000

200,000

6

50,000

200,000

7

50,000

200,000

8

50,000

200,000

53. Which of the following can be used to place capital investment proposals involving different amounts of

54. Using the following partial table of present value of $1 at compound interest, compute the present value of

$20,000 (rounded to nearest dollar) to be received one year from today, assuming an earnings rate of 15%.

1

0.909

0.870

0.833

2

0.826

0.756

0.694

3

0.751

0.658

0.579

4

0.683

0.572

0.482

5

0.621

0.497

0.402

6

0.564

0.432

0.335

7

0.513

0.376

0.279

55. An analysis of a proposal by the net present value method indicated that the present value exceeded the

56. In general, present value methods of analyzing capital investments are more desirable than methods

57. Which method of evaluating capital investment proposals uses the concept of present value to compute a

58. The rate of return is 10% and the cash to be received in one year is $10,000. Determine the present value

amount, using the following partial table of present value of $1 at compound interest:

1

0.943

0.909

0.893

2

0.890

0.826

0.797

3

0.840

0.751

0.712

4

0.792

0.683

0.636

59. Using the following partial table of present value of $1 at compound interest, determine the present value of

$20,000 to be received four years hence with earnings at the rate of 12% a year:

1

0.943

0.909

0.893

2

0.890

0.826

0.797

3

0.840

0.751

0.712

4

0.792

0.683

0.636

60. When several alternative investment proposals of the same amount are being considered, the one with the

largest net present value is the most desirable. If the alternative proposals involve different amounts of

61. Which method of evaluating capital investment proposals uses present value concepts to compute the rate of

64. Crane Company is considering the acquisition of a machine that costs $60,000. The machine is expected to

have a useful life of 5 years, a negligible residual value, an annual cash flow of $15,000, and annual operating

65. The expected average rate of return for a proposed investment of $3,000,000 in a fixed asset giving effect to

depreciation (straight-line method) with a useful life of 20 years, no residual value, and an expected total

67. The management of Hence Corporation is considering the purchase of a new machine costing $200,000.

The company's desired rate of return is 10%. The present value factors for $1 at compound interest of 10% for 1

through 5 years are 0.909, 0.826, 0.751, 0.683, and 0.621, respectively. In addition to the foregoing information,

use the following data in determining the acceptability in this situation:

Income from

Net

Cash

Year

Operations

Flow

1

$50,000

$90,000

2

20,000

60,000

3

10,000

50,000

4

5,000

45,000

5

5,000

45,000

68. The management of Hence Corporation is considering the purchase of a new machine costing $200,000.

The company's desired rate of return is 10%. The present value factors for $1 at compound interest of 10% for 1

through 5 years are 0.909, 0.826, 0.751, 0.683, and 0.621, respectively. In addition to the foregoing information,

use the following data in determining the acceptability in this situation:

Income from

Net

Cash

Year

Operations

Flow

A. 18%.

B. 16%.

C. 58%.

D. 20%.

69. The management of Hence Corporation is considering the purchase of a new machine costing $200,000.

The company's desired rate of return is 10%. The present value factors for $1 at compound interest of 10% for 1

through 5 years are 0.909, 0.826, 0.751, 0.683, and 0.621, respectively. In addition to the foregoing information,

use the following data in determining the acceptability in this situation:

Income from

Net

Cash

Year

Operations

Flow

A. positive $24,960.

B. negative $27,600.

C. positive $27,600.

D. negative $24,960.

70. The management of Hence Corporation is considering the purchase of a new machine costing $200,000.

The company's desired rate of return is 10%. The present value factors for $1 at compound interest of 10% for 1

through 5 years are 0.909, 0.826, 0.751, 0.683, and 0.621, respectively. In addition to the foregoing information,

use the following data in determining the acceptability in this situation:

Income from

Net

Cash

Year

Operations

Flow

A. 0.88.

B. 1.45.

C. 1.14.

D. 0.70.

71. The management of London Corporation is considering the purchase of a new machine costing $750,000.

The company's desired rate of return is 6%. The present value factors for $1 at compound interest of 6% for 1

through 5 years are 0.943, 0.890, 0.840, 0.792, and 0.747, respectively. In addition to this information, use the

following data in determining the acceptability in this situation:

Income from

Net

Cash

Year

Operations

Flow

A. 3 years.

B. 5 years.

C. 20 years.

D. 4 years.

72. The management of London Corporation is considering the purchase of a new machine costing $750,000.

The company's desired rate of return is 6%. The present value factors for $1 at compound interest of 6% for 1

through 5 years are 0.943, 0.890, 0.840, 0.792, and 0.747, respectively. In addition to this information, use the

following data in determining the acceptability in this situation:

Income from

Net

Cash

Year

Operations

Flow

A. 5%.

B. 10%.

C. 25%.

D. 15%.

73. The management of London Corporation is considering the purchase of a new machine costing $750,000.

The company's desired rate of return is 6%. The present value factors for $1 at compound interest of 6% for 1

through 5 years are 0.943, 0.890, 0.840, 0.792, and 0.747, respectively. In addition to this information, use the

following data in determining the acceptability in this situation:

Income from

Net

Cash

Year

Operations

Flow

A. positive $39,750.

B. positive $118,145.

C. negative $118,145.

D. negative $39,750.

74. The management of London Corporation is considering the purchase of a new machine costing $750,000.

The company's desired rate of return is 6%. The present value factors for $1 at compound interest of 6% for 1

through 5 years are 0.943, 0.890, 0.840, 0.792, and 0.747, respectively. In addition to this information, use the

following data in determining the acceptability in this situation:

Income from

Net

Cash

Year

Operations

Flow

1

$37,500

$187,500

2

37,500

187,500

3

37,500

187,500

4

37,500

187,500

5

37,500

187,500

76. The expected average rate of return for a proposed investment of $540,000 in a fixed asset, with a useful life

of four years, recognition is given to the effect of straight-line depreciation on the investment, no residual value,

77. The amount of the average investment for a proposed investment of $70,000 in a fixed asset, with a useful

life of four years, recognition is given to the effect of straight-line depreciation on the investment, no residual

78. The amount of the estimated average income for a proposed investment of $60,000 in a fixed asset, giving

effect to depreciation (straight-line method), with a useful life of four years, no residual value, and an expected

79. Assuming that the desired rate of return is 6%, determine the present value of $10,000 to be received in one

year, using the following partial table of present value of $1 at compound interest.

1

0.943

0.909

0.893

2

0.890

0.826

0.797

3

0.840

0.751

0.712

4

0.792

0.683

0.636

80. Using the following partial table of present value of $1 at compound interest, determine the present value of

$20,000 to be received four years hence, with earnings at the rate of 10% a year.

1

0.943

0.909

0.893

2

0.890

0.826

0.797

3

0.840

0.751

0.712

4

0.792

0.683

0.636

81. Using the following partial table of present value of $1 at compound interest, determine the present value of

$20,000 to be received three years hence, with earnings at the rate of 10% a year.

1

0.943

0.909

0.893

2

0.890

0.826

0.797

3

0.840

0.751

0.712

4

0.792

0.683

0.636

82. If the rate of earnings is 10% and the cash to be received in two years is $10,000, determine the present

value amount, using the following partial table of present value of $1 at compound interest.

1

0.943

0.909

0.893

2

0.890

0.826

0.797

3

0.840

0.751

0.712

4

0.792

0.683

0.636

86. Which of the following provisions of the Internal Revenue Code can be used to reduce the amount of the

87. Assume in analyzing alternative proposals that Proposal F has a useful life of six years and Proposal J has a

89. The process by which management allocates available investment funds among competing investment

90. In capital rationing, an initial screening of alternative proposals is usually performed by establishing

91. In capital rationing, alternative proposals that survive initial screening and further analysis using present

92. Mars Corp. is choosing between two different capital investment proposals. Machine A has a useful life of 4

1

0.909

2

0.826

3

0.751

4

0.683

5

0.621

6

0.513

Machine A will generate net cash flow of $70,000 in each of the four years. Machine B will generate $80,000 in year 1, $70,000 in year 2, $60,000 in

year 3, and $40,000 per year for the remaining 3 years of its useful life.

94. A 5-year project is estimated to cost $700,000 and have no residual value. If the straight-line depreciation

95. Both proposal M, and N cost $800,000, have a 6-year life, and have expected total cash flows of

96. A $350,000 capital investment proposal has an estimated life of four years and no residual value. The

estimated net cash flows are as follows:

3

0.712

104,000

74,048

4

0.636

90,000

57,24

97. Heedy Inc. is considering a capital investment proposal that costs $460,000 and has an estimated life of four

years, and no residual value. The estimated net cash flows are as follows:

Year

Net Cash Flow

1

$195,000

2

160,000

3

120,000

4

80,000

The minimum desired rate of return for net present value analysis is 10%. The present value of $1 at compound interest rates of 10% for 1, 2, 3, and 4

years is 0.909, 0.826, 0.751, and 0.683, respectively. Determine the net present value.

Present Value

Ne

t

Present

Value of

Year

of $1 at 10%

Ca

sh

Fl

o

Net Cash

Flow

98. The net present value has been computed for Proposals A and B. Relevant data are as follows:

Proposal A

Proposal B

Amount to be invested

$75,000

$125,000

Total present value of net cash flow

84,000

136,250

Net present value

9,000

11,250

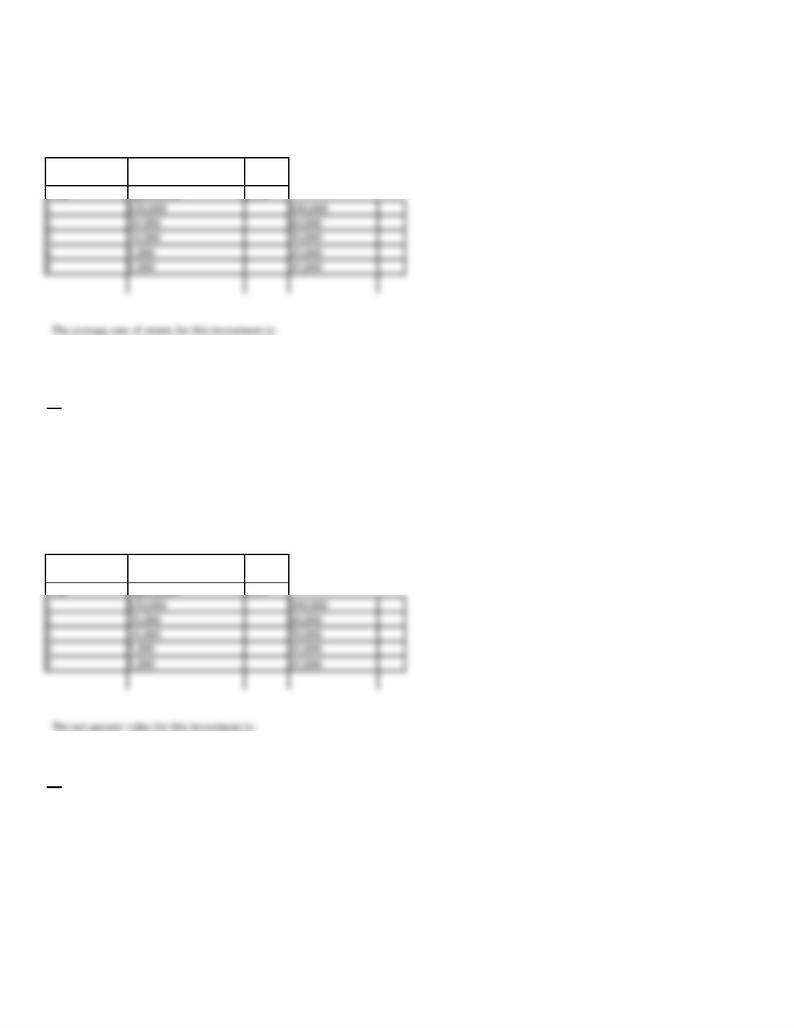

99. Sommers Company is evaluating a project requiring a capital expenditure of $300,000. The project has an

estimated life of 5 years and no salvage value. The estimated net income and net cash flow from the project are

as follows:

Year

Net Income

Net Cash

Flow

1

$ 60,000

$120,000

1

0.893

2

0.797

3

0.712

4

0.636

5

0.567

(b)

Present Value

Net

P

r

e

s

e

n

t

V

al

u

e

o

f

Year

of $1 at 12%

Cash Flow

N

et

C

a

s

h

F

l

o

w

1

0.893

$120,000

$107,160

2

0.797

110,000

87,670

3

0.712

105,000

74,760

4

0.636

90,000

57,240

5

0.567

80,000

45,360

100. June Co. is evaluating a project requiring a capital expenditure of $620,000. The project has an estimated

life of four years and no salvage value. The estimated net income and net cash flow from the project are as

follows:

Year

Net Income

Net

Cash

0.712, and 0.636, respectively.

(b)

Present Value

Present Value of

Year

of $1 at 12%

Net

Cash

Flow

Net Cash Flow

4

0.636

170,00

108,

101. The internal rate of return method is used to analyze a $831,500 capital investment proposal with annual

net cash flows of $250,000 for each of the six years of its useful life.

(a)

Determine a present value factor for an annuity of $1, which can be used in determining the internal rate of return.

(b)

Based on the factor determined in (a) and the portion of the present value of an annuity of $1 table presented below, determine the

internal rate of return for the proposal.

Year

10%

15%

20%

1

0.909

0.870

0.833

2

1.736

1.626

1.528

3

2.487

2.283

2.106

4

3.170

2.855

2.589

5

3.791

3.353

2.991

6

4.355

3.785

3.326

7

4.868

4.160

3.605

102. Harris Co. is considering a 12-year project that is estimated to cost $900,000 and has no residual value.

Harris seeks to earn an average rate of return of 15% on all capital projects. Determine the necessary average

annual income (using straight-line depreciation) that must be achieved on this project for it to be acceptable to

Harris Co.

Estimated Average Annual Income

= Average Rate of Return

Average Investment

X

= .15

($900,000 + $0)/2

X

= .15

$450,000

X

= $67,500

103. Proposals L and K each cost $500,000, have 6-year lives, and have expected total cash flows of $750,000.

Proposal L is expected to provide equal annual net cash flows of $125,000, while the net cash flows for

Proposal K are as follows:

Year 1

$250,000

Year 2

200,000

Year 3

100,000

Year 4

90,000

Year 5

60,000

Year 6

50,000

$750,000

Determine the cash payback period for each proposal.

Proposal L: $500,000/$125,000 = 4 years

Proposal K: 2 years ($250,000 + $200,000) + 0.5 years ($50,000/$100,000) = 2.50 years