Chapter 3--Accrual Accounting Concepts

Student: ___________________________________________________________________________

2. The accrual basis recognizes liabilities at the time the business incurs the obligation to pay for the services or

4. Accrual accounting does not require that the accounting records be updated prior to preparing financial

5. The revenue recognition concept states that revenue should be recorded in the same period as the cash is

6. Under the accrual basis of accounting, the accounting records are normally updated after the preparation of

7. The matching concept requires expenses to be recorded in the same period that the related revenue is

19. Expenses on the income statement are assets used up or services consumed in the process of generating

20. Under the accrual basis of accounting, net cash flows from operating activities on the statement of cash

21. The process that begins with the analysis of transactions and ends with preparing the accounting records for

24. Under the cash basis of accounting, no adjustments are necessary prior to the preparation of the financial

26. Under the cash basis of accounting, a business records only transactions involving increases or decreases of

27. To arrive at cash flows from operations, it is necessary to convert the income statement from an accrual

28. If land costing $75,000 was sold for $135,000, the amount reported in the investing activities section of the

29. To determine cash payments for operating expenses for the cash flow statement using the direct method,

30. Flyer Co. billed a client for flying lessons given in January. The payment was received in February. Under

33. UNI Co. received $1,000 advance from Newbie as rent for the use of a building owned by UNI. How does

36. On April 1, Smart, Inc. paid $7,200 for an insurance premium on a three-year insurance policy. How does

37. Eagle Eye, Inc., a corporation, received an additional investment of $6,000 cash in exchange for shares of

38. As time passes, fixed assets, other than land, lose their capacity to provide useful services. To account for

this decrease in usefulness, the cost of fixed assets is systematically allocated to expense through a process

39. A&M Co. provided services of $1,000,000 to clients on account. How does this transaction affect A&M's

40. A&M Co. purchased land for $50,000 with $10,000 paid in cash and $40,000 in a note payable due three

42. The unearned rent account has a balance of $50,000. If $3,000 of the $50,000 is unearned at the end of the

43. X&Y Co. received $4,000 in payments from clients for services billed in a previous month. What effect

44. XYZ Co. received $3,000 in payments from clients for services billed in a previous month. Which accounts

45. Unearned rent, representing rent for the next six months' occupancy, would be reported on the landlord's

49. The balance in the office supplies account on June 1 was $5,200, supplies purchased during June were

$2,500, and the supplies on hand at June 30 were $1,500. The amount to be used for the appropriate adjusting

50. When cash is received in payment of an account receivable, which section of the Statement of Cash Flows is

54. On April 1, Bear, Inc. paid $2,400 for an insurance premium on a three-year insurance policy. At the end of

55. On June 1, Green Pea, Inc. purchased $1,200 worth of supplies on account. Prior to the purchase, the

balance in the supplies account was $0. On December 31, the fiscal year-end for Green Pea, it is determined that

56. On June 1, Green Pea, Inc. purchased $1,200 worth of supplies on account. Prior to the purchase, the

balance in the supplies account was $200. On December 31, the fiscal year-end for Green Pea, it is determined

59. Deferred expenses (prepaid expenses) are items initially recorded as assets but are expected to become

61. Deferred revenues (unearned revenues) are items initially recorded as liabilities, but expected to become

63. Donald Duck Co.

Donald Duck Co. has a five-day workweek (Monday through Friday). Employees earn $500 per day.

Refer to Donald Duck Co. If the month ends on Tuesday, and wages will not be paid until Friday, how much

64. Donald Duck Co.

Donald Duck Co. has a five-day workweek (Monday through Friday). Employees earn $500 per day.

66. St. Nick Corporation's Toy-Making Supplies account showed a beginning balance of $200 and supplies

purchased of $800. There were $400 of supplies on hand at year-end. The year-end adjustment would include

67. In October, cash is received in advance of rendering services. Assuming that half of the services have been

68. Speedy Company's weekly payroll of $250 is paid on Fridays (five-day work week). Assume that the last

70. When an adjusting entry is made to record insurance expense and reduce the prepaid insurance account,

71. When an entry is made to adjust the supplies account and recognize supplies expense for the period, which

73. The _____ is prepared with various sections, subsections, and captions that aid in its interpretation and

79. The following assets are included in Bruce Auto Parts, Inc.'s December 31, 2010, balance sheet.

Accounts Receivable

(net of Allowance for Uncollectible Accounts)

$ 50,000

Accumulated Depreciation, Building

30,000

Building

100,000

Cash

60,000

Land

130,000

Land Held for Future Use

40,000

Merchandise Inventory

70,000

Trademark

110,000

80. Cash and other assets that are expected to be converted to cash or sold or used up within one year or less

82. ABN Company sold goods, receiving $20,000 in cash and $25,000 on credit. How much revenue should it

85. Which of the following should be deducted from net income in calculating net cash flow from operating

88. Depreciation on factory equipment would be reported in the statement of cash flows prepared by the indirect

89. Which of the following should be added to net income in calculating net cash flow from operating activities

90. Which one of the following should be added to net income in calculating net cash flow from operating

91. On the statement of cash flows prepared by the indirect method, a $50,000 gain on the sale of investments

92. Accounts receivable arising from trade transactions amounted to $50,000 and $56,000 at the beginning and

end of the year, respectively. Net income reported on the income statement for the year was $105,000.

Exclusive of the effect of other adjustments, the cash flows from operating activities to be reported on the

93. The net income reported on the income statement for the current year was $310,000. Depreciation recorded

on fixed assets and amortization of patents for the year were $40,000 and $9,000, respectively. Balances of

current asset and current liability accounts at the end and at the beginning of the year are as follows:

End

Beginning

Cash

$ 50,000

$ 60,000

Accounts receivable

112,000

108,000

Inventories

105,000

93,000

Prepaid expenses

4,500

6,500

Accounts payable (merchandise creditors)

75,000

89,000

94. Describe the differences between the cash and accrual bases of accounting.

95. When are sales recognized under the cash basis of accounting? When are expenses recognized?

96. Assume the November transactions for Hoover Co. are as follows:

a.

Received cash of $40,000 from investors in exchange for capital stock.

b.

Provided services of $15,600 on account.

c.

Purchased supplies on account $800.

d.

Received cash of $10,900 from clients for services previously billed.

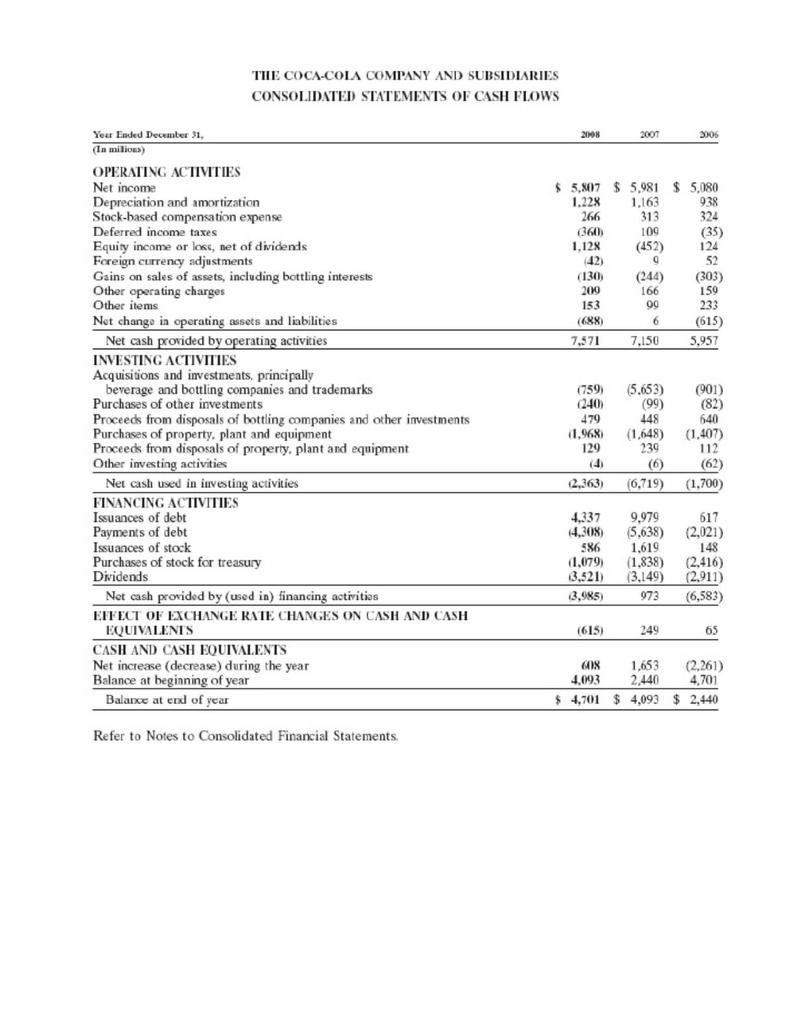

e.

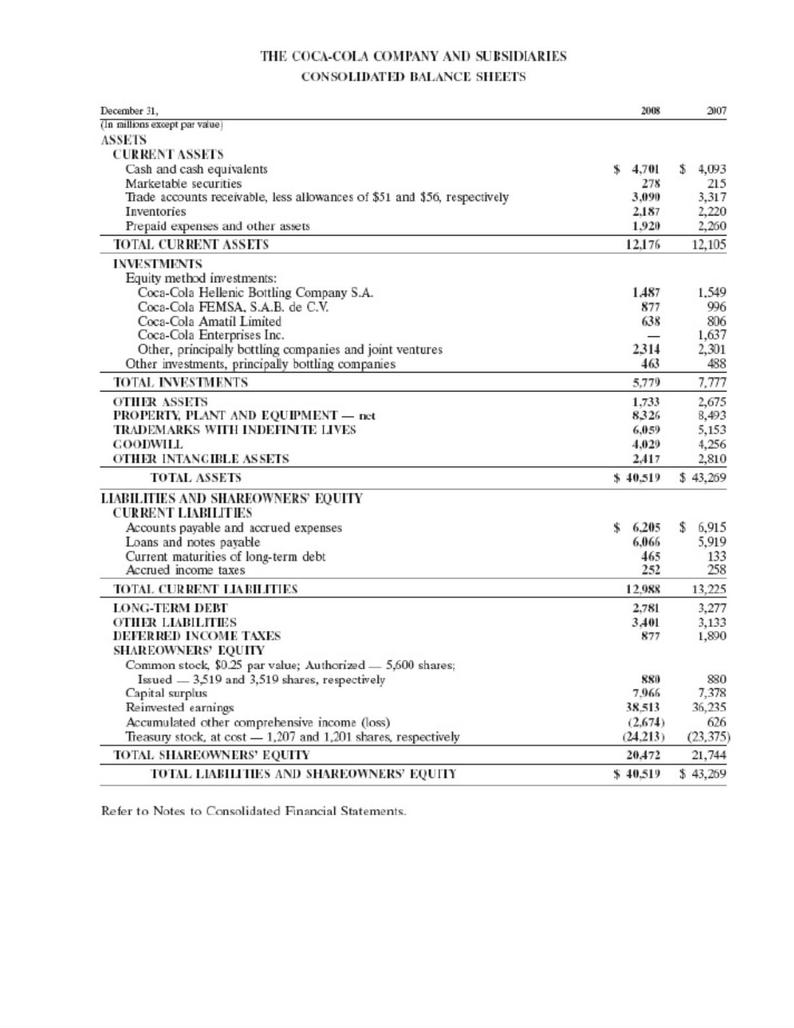

Received $5,100 for services provided from clients who paid cash.

f.

Paid $400 on account for supplies that had been purchased.

g.

Paid $2,400 for a one-year insurance policy.

h.

Paid the following expenses: wages, $8,000; utilities, $900; rent, $2,000.

i.

Paid dividends of $1,500 to stockholders.

Record the transactions, using the integrated financial statement framework that follows:

Assets =

Liabilities

+ Stockholders'

Equity

Cash

Accounts Receivable

Supplies

Prepaid

Insurance

Accounts Payable

Capital Stock

Retained

Earnings

97. Describe the end-of-the-period adjustment process. Why is it necessary?

98. Describe deferrals and accruals.

99. Under the balance sheet classification of property, plant, and equipment, some accounts need adjustment

and others do not. Which do and why? Which do not and why?

100. Why is a physical count of supplies necessary at the end of the accounting period?

101. Classify the following items as:

102. Identify the type of adjustment necessary (the type of item involved) and record the transaction for the

event. Make sure to include the ending balances after adjustment.

Assume that on June 1, 2013, Tasty Sausage Corp. had paid $1,500 in advance for a 6-month insurance policy.

The June 30 adjustment is:

Assets =

Liabilities

+ Stockholders'

Equity

Cash

Prepaid

Insurance

Office

Equipment

Accounts

Payable

Common

Stock

Retained

Earnings

Beg. Bal.

-1,500

1,500

Adjustment

End. Bal.

103. Identify the type of adjustment necessary (the type of item involved) and record the transaction for the

event. Make sure to include the ending balances after adjustment.

104. Identify the type of adjustment necessary (the type of item involved) and record the transaction for the

event. Make sure to include the ending balances after adjustment.

105. Identify the type of adjustment necessary (the type of item involved) and record the transaction for the

event. Make sure to include the ending balances after adjustment.

106. Identify the type of adjustment necessary (the type of item involved) and record the transaction for the

event. Make sure to include the ending balances after adjustment.

107. At the end of the fiscal year, the following adjusting entries were omitted:

(a)

No adjusting entry was made to transfer the $3,000 of prepaid insurance from the asset account to the expense account.

(b)

No adjusting entry was made to record accrued fees of $500 for services provided to customers.

$

$

$

$

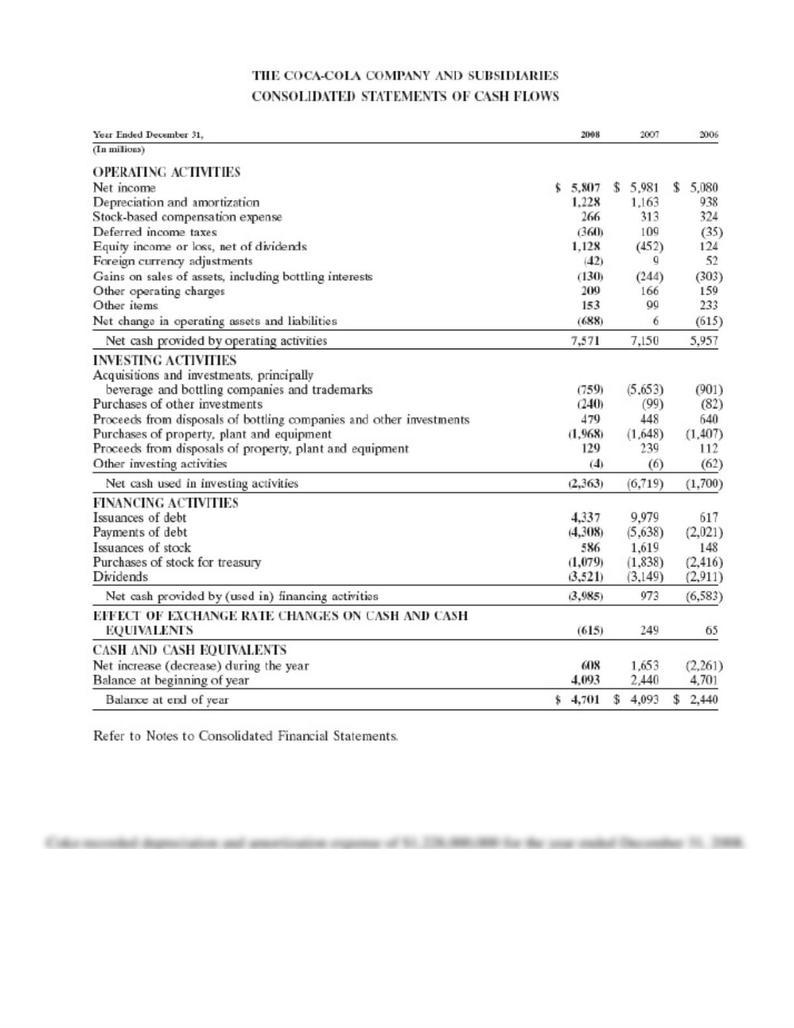

108.

Refer to Coke’s Statement of Cash Flows. What amount of depreciation and amortization did Coke record in

2008?

109.

Refer to Coke’s balance sheet. Does it appear that Coke uses the cash or accrual basis of accounting?

110. Gaston Corporation’s accumulated depreciation increased by $10,000, while patents decreased by $3,200

111. River Corporation’s accumulated depreciation increased by $12,000, while patents decreased by $3,500

Chapter 3--Accrual Accounting Concepts Key

2. The accrual basis recognizes liabilities at the time the business incurs the obligation to pay for the services or

4. Accrual accounting does not require that the accounting records be updated prior to preparing financial

5. The revenue recognition concept states that revenue should be recorded in the same period as the cash is

6. Under the accrual basis of accounting, the accounting records are normally updated after the preparation of

7. The matching concept requires expenses to be recorded in the same period that the related revenue is

19. Expenses on the income statement are assets used up or services consumed in the process of generating

20. Under the accrual basis of accounting, net cash flows from operating activities on the statement of cash

21. The process that begins with the analysis of transactions and ends with preparing the accounting records for

24. Under the cash basis of accounting, no adjustments are necessary prior to the preparation of the financial

26. Under the cash basis of accounting, a business records only transactions involving increases or decreases of

27. To arrive at cash flows from operations, it is necessary to convert the income statement from an accrual

28. If land costing $75,000 was sold for $135,000, the amount reported in the investing activities section of the

29. To determine cash payments for operating expenses for the cash flow statement using the direct method,

30. Flyer Co. billed a client for flying lessons given in January. The payment was received in February. Under

33. UNI Co. received $1,000 advance from Newbie as rent for the use of a building owned by UNI. How does

36. On April 1, Smart, Inc. paid $7,200 for an insurance premium on a three-year insurance policy. How does

37. Eagle Eye, Inc., a corporation, received an additional investment of $6,000 cash in exchange for shares of

38. As time passes, fixed assets, other than land, lose their capacity to provide useful services. To account for

this decrease in usefulness, the cost of fixed assets is systematically allocated to expense through a process

39. A&M Co. provided services of $1,000,000 to clients on account. How does this transaction affect A&M's

40. A&M Co. purchased land for $50,000 with $10,000 paid in cash and $40,000 in a note payable due three

42. The unearned rent account has a balance of $50,000. If $3,000 of the $50,000 is unearned at the end of the

43. X&Y Co. received $4,000 in payments from clients for services billed in a previous month. What effect

44. XYZ Co. received $3,000 in payments from clients for services billed in a previous month. Which accounts

45. Unearned rent, representing rent for the next six months' occupancy, would be reported on the landlord's

49. The balance in the office supplies account on June 1 was $5,200, supplies purchased during June were

$2,500, and the supplies on hand at June 30 were $1,500. The amount to be used for the appropriate adjusting

50. When cash is received in payment of an account receivable, which section of the Statement of Cash Flows is

54. On April 1, Bear, Inc. paid $2,400 for an insurance premium on a three-year insurance policy. At the end of

55. On June 1, Green Pea, Inc. purchased $1,200 worth of supplies on account. Prior to the purchase, the

balance in the supplies account was $0. On December 31, the fiscal year-end for Green Pea, it is determined that

56. On June 1, Green Pea, Inc. purchased $1,200 worth of supplies on account. Prior to the purchase, the

balance in the supplies account was $200. On December 31, the fiscal year-end for Green Pea, it is determined

59. Deferred expenses (prepaid expenses) are items initially recorded as assets but are expected to become

61. Deferred revenues (unearned revenues) are items initially recorded as liabilities, but expected to become

63. Donald Duck Co.

Donald Duck Co. has a five-day workweek (Monday through Friday). Employees earn $500 per day.

Refer to Donald Duck Co. If the month ends on Tuesday, and wages will not be paid until Friday, how much

64. Donald Duck Co.

Donald Duck Co. has a five-day workweek (Monday through Friday). Employees earn $500 per day.

66. St. Nick Corporation's Toy-Making Supplies account showed a beginning balance of $200 and supplies

purchased of $800. There were $400 of supplies on hand at year-end. The year-end adjustment would include

67. In October, cash is received in advance of rendering services. Assuming that half of the services have been

68. Speedy Company's weekly payroll of $250 is paid on Fridays (five-day work week). Assume that the last

70. When an adjusting entry is made to record insurance expense and reduce the prepaid insurance account,

71. When an entry is made to adjust the supplies account and recognize supplies expense for the period, which

73. The _____ is prepared with various sections, subsections, and captions that aid in its interpretation and

79. The following assets are included in Bruce Auto Parts, Inc.'s December 31, 2010, balance sheet.

Accounts Receivable

(net of Allowance for Uncollectible Accounts)

$ 50,000

Accumulated Depreciation, Building

30,000

Building

100,000

Cash

60,000

Land

130,000

Land Held for Future Use

40,000

Merchandise Inventory

70,000

Trademark

110,000

80. Cash and other assets that are expected to be converted to cash or sold or used up within one year or less

82. ABN Company sold goods, receiving $20,000 in cash and $25,000 on credit. How much revenue should it

85. Which of the following should be deducted from net income in calculating net cash flow from operating

88. Depreciation on factory equipment would be reported in the statement of cash flows prepared by the indirect

89. Which of the following should be added to net income in calculating net cash flow from operating activities

90. Which one of the following should be added to net income in calculating net cash flow from operating

91. On the statement of cash flows prepared by the indirect method, a $50,000 gain on the sale of investments

92. Accounts receivable arising from trade transactions amounted to $50,000 and $56,000 at the beginning and

end of the year, respectively. Net income reported on the income statement for the year was $105,000.

Exclusive of the effect of other adjustments, the cash flows from operating activities to be reported on the

93. The net income reported on the income statement for the current year was $310,000. Depreciation recorded

on fixed assets and amortization of patents for the year were $40,000 and $9,000, respectively. Balances of

current asset and current liability accounts at the end and at the beginning of the year are as follows:

End

Beginning

Cash

$ 50,000

$ 60,000

Accounts receivable

112,000

108,000

Inventories

105,000

93,000

Prepaid expenses

4,500

6,500

Accounts payable (merchandise creditors)

75,000

89,000

94. Describe the differences between the cash and accrual bases of accounting.

Under the cash basis of accounting, transactions are recorded when cash is affected. Revenue is recognized

when cash is received, and expenses are recorded when cash is paid. Under accrual accounting, transactions are

recorded as they occur, not just when cash is affected. Thus, revenue is recognized when it is earned. Expenses

are recorded when they are incurred.

95. When are sales recognized under the cash basis of accounting? When are expenses recognized?

Under the cash basis of accounting, the only time revenues or expenses are recognized is when there is a

transaction affecting cash. So, when there is a sale and when the cash is exchanged, sales are recognized. When

an expense is paid in cash, then it is recognized.

96. Assume the November transactions for Hoover Co. are as follows:

a.

Received cash of $40,000 from investors in exchange for capital stock.

b.

Provided services of $15,600 on account.

c.

Purchased supplies on account $800.

d.

Received cash of $10,900 from clients for services previously billed.

e.

Received $5,100 for services provided from clients who paid cash.

f.

Paid $400 on account for supplies that had been purchased.

g.

Paid $2,400 for a one-year insurance policy.

h.

Paid the following expenses: wages, $8,000; utilities, $900; rent, $2,000.

i.

Paid dividends of $1,500 to stockholders.

Record the transactions, using the integrated financial statement framework that follows:

Assets =

Liabilities

+ Stockholders'

Equity

Cash

Accounts Receivable

Supplies

Prepaid

Insurance

Accounts Payable

Capital Stock

Retained

Earnings

a.

b.

c.

d.

e.

f.

g.

h.

i.

Bal.

Calculate the November 30 cash balance and the amount of net income for November for Hoover Co.

Assets =

Liabilities

+ Stockholders'

Equity

Cash

Accounts Receivable

Supplies

Prepaid

Insurance

Accounts Payable

Capital Stock

Retained

Earnings

97. Describe the end-of-the-period adjustment process. Why is it necessary?

Using the accrual basis of accounting requires the accounting records to be updated before preparing the

financial statements. This is necessary to properly match revenues and expenses. These adjustments are

necessary because at any given point in time, some accounts will not be up to date.

98. Describe deferrals and accruals.

Deferrals are created by recording a transaction that delays the recognition of an expense or revenue. An

example of a deferral is prepaid insurance. The expense recognition is "deferred" until time has passed.

Accruals are created when a revenue/expense has not been recorded at the end of the accounting period. An

example of an accrual is interest income earned but not yet recorded.

99. Under the balance sheet classification of property, plant, and equipment, some accounts need adjustment

and others do not. Which do and why? Which do not and why?

100. Why is a physical count of supplies necessary at the end of the accounting period?

101. Classify the following items as:

102. Identify the type of adjustment necessary (the type of item involved) and record the transaction for the

event. Make sure to include the ending balances after adjustment.

Assume that on June 1, 2013, Tasty Sausage Corp. had paid $1,500 in advance for a 6-month insurance policy.

The June 30 adjustment is:

Assets =

Liabilities

+ Stockholders'

Equity

Cash

Prepaid

Insurance

Office

Equipment

Accounts

Payable

Common

Stock

Retained

Earnings

Beg. Bal.

-1,500

1,500

Adjustment

End. Bal.

Item: Expense Deferral

Assets =

Liabilities

+ Stockholders'

Equity

103. Identify the type of adjustment necessary (the type of item involved) and record the transaction for the

event. Make sure to include the ending balances after adjustment.

Assume that on June 1, 2013, Tasty Sausage Corp. has a balance of $100 for supplies. On June 6 it purchased

$600 in supplies for cash. On June 30, at the end of the accounting period, there are $300 of supplies on hand.

The June 30 adjustment is:

Assets =

Liabilities

+ Stockholders'

Equity

Cash

Supplies

Office

Equipment

Accounts

Payable

Common

Stock

Retained

Earnings

Beg. Bal.

-100

100

Supplies

purchased

-600

600

Bal.

-700

700

Item: Expense Deferral

Assets =

Liabilities

+ Stockholders'

Equity

Cash

Supplies

Office

Equipment

Accounts

Payable

Common

Stock

Retained

Earnings

Bal.

-700

700

Adjustment

-400

-400—

Supplies expense

End. Bal.

-700

300

-400

104. Identify the type of adjustment necessary (the type of item involved) and record the transaction for the

event. Make sure to include the ending balances after adjustment.

Assume that on June 1, 2013, Tasty Sausage Corp. received $9,000 in advance to provide sausages over the

next three months. The June 30 adjustment is:

Assets =

Liabilities

+ Stockholders' Equity

Cash

Office

Equipment

Accumulated

Depreciation

Unearned

Revenue

Common

Stock

Retained

Earnings

Beg. Bal.

9,000

9,000

Adjustment

End. Bal.

Item: Revenue Deferral

Assets =

Liabilities

+ Stockholders' Equity

Cash

Office

Equipment

Accumulated

Depreciation

Unearned

Revenue

Common

Stock

Retained

Earnings

Beg. Bal.

9,000

9,000

Adjustment

-3,000

3,000—

Revenue

End. Bal.

9,000

6,000

3,000

105. Identify the type of adjustment necessary (the type of item involved) and record the transaction for the

event. Make sure to include the ending balances after adjustment.

Assume Tasty Sausage Corp. pays salaries on the 28th of each month. Sausage stuffers earn $200/day with a

7-day work week. June 30th is the end of the accounting period. Sausage stuffers have worked on the 29th and

30th but have not yet been paid for those days. The June 30 adjustment is:

Assets =

Liabilities

+ Stockholders' Equity

Cash

Office

Equipment

Accumulated

Depreciation

Salaries

Payable

Common

Stock

Retained

Earnings

Adjustment

End. Bal.

Item: Accrued Expense

Assets =

Liabilities

+ Stockholders' Equity

Cash

Office

Equipment

Accumulated

Depreciation

Salaries

Payable

Common

Stock

Retained

Earnings

Adjustment

400

-400—Salary

expense

End. Bal.

400

-400

106. Identify the type of adjustment necessary (the type of item involved) and record the transaction for the

event. Make sure to include the ending balances after adjustment.

On June 1, Tasty Sausage Corp. borrowed $25,000 from the bank by signing a promissory note from the bank,

with 8% interest. The note is due in three months. Interest for June has been incurred but not yet recorded. The

interest to accrue for June is $175. The June 30 adjustment is:

Assets =

Liabilities

+ Stockholders' Equity

Cash

Office

Equipment

Accumulated

Depreciation

Interest

Payable

Common

Stock

Retained

Earnings

Adjustment

End. Bal.

Item: Accrued Expense

Assets =

Liabilities

+ Stockholders' Equity

Cash

Office

Equipment

Accumulated

Depreciation

Interest

Payable

Common

Stock

Retained

Earnings

Adjustment

175

-175—Interest

expense

End. Bal.

175

-175

107. At the end of the fiscal year, the following adjusting entries were omitted:

(a)

No adjusting entry was made to transfer the $3,000 of prepaid insurance from the asset account to the expense account.

(b)

No adjusting entry was made to record accrued fees of $500 for services provided to customers.

108.

Refer to Coke’s Statement of Cash Flows. What amount of depreciation and amortization did Coke record in

2008?

109.

Refer to Coke’s balance sheet. Does it appear that Coke uses the cash or accrual basis of accounting?

110. Gaston Corporation’s accumulated depreciation increased by $10,000, while patents decreased by $3,200

between consecutive balance sheet dates. There were no purchases or sales of depreciable or intangible assets

during the year. In addition, the income statement showed a gain of $3,500 from sale of land. Reconcile a net

income of $45,000 to net cash flow from operating activities.

Net income

$45,000

Adjustments to reconcile net income to net cash from operating activities:

Depreciation

10,000

Amortization

3,200

Gain from sale of land

(3,500)

Net cash flows from operating activities

$54,700

111. River Corporation’s accumulated depreciation increased by $12,000, while patents decreased by $3,500

between consecutive balance sheet dates. There were no purchases or sales of depreciable or intangible assets

during the year. In addition, the income statement showed a loss on sale of land of $2,500. Accounts receivable

increased $5,000, inventory decreased $3,200, prepaid expenses decreased $800, and account payable increased

$2,000. Reconcile a net income of $55,000 to net cash flow from operating activities.

Net income

$55,000

Adjustments to reconcile net income to net cash from operating activities:

Depreciation

12,000