Chapter 4--Accounting for Merchandising Businesses

Student: ___________________________________________________________________________

1. Operating expenses are subtracted from fees earned for a service business and from gross profit for a

4. Net income or loss may appear on the income statement of both a service business and a merchandising

5. On the income statement, sales returns and allowances and sales discounts are added to gross sales to yield

6. On the income statement, sales discounts are normally deducted from sales to yield the cost of merchandise

7. On the income statement, the merchandise inventory at the beginning of the period is added to sales to yield

8. On the income statement in the single-step form, the total of all expenses is deducted from the total of all

9. A criticism of the single-step income statement is that gross profit and income from operations are not readily

16. The indirect method of preparing the statement of cash flows reconciles net income with net cash flows

19. In a multiple-step income statement, sales will be reduced by sales discounts and sales returns and

23. If payment is due by the end of the month in which the sale is made, the invoice terms are expressed as

27. Sales to customers who use bank credit cards, such as MasterCard and VISA, are generally treated as credit

28. The document issued by the seller that informs the buyer of the details of sales returns is called a debit

29. The effect of a sales return and allowance is a reduction in sales revenue and a decrease in cash or accounts

30. When the seller offers a sales discount, even if borrowing has to be done, it is generally advantageous for

31. If merchandise costing $2,500, terms FOB destination, 2/10, n/30, with prepaid transportation costs of $100,

32. A buyer who acquires merchandise under credit terms of 1/10, n/30 has 30days after the invoice date to take

33. Available discounts taken by the buyer for early payment of an invoice are termed sales discounts by the

34. Purchases of merchandise increase the merchandise inventory account under the perpetual inventory

35. A buyer who acquires merchandise under credit terms of 1/10, n/30 has 10 days after the invoice date to

37. In a perpetual inventory system, merchandise returned to vendors reduces the merchandise inventory

39. If the ownership of merchandise passes to the buyer when the seller delivers the merchandise for shipment,

40. Merchandise is sold for $2,500, terms FOB destination, 2/10, n/30, with transportation costs of $150. If

$500 of the merchandise is returned prior to payment and the invoice is paid within the discount period, the

42. If merchandise costing $2,500, terms FOB destination, 2/10, n/30, with transportation costs of $100, is paid

43. When someone purchases merchandise and incurs the cost of transportation, these costs of purchasing

45. In a transaction where purchased merchandise has been returned, the buyer will increase the Sales Returns

48. There are two alternatives to reporting cash flows from operating activities in the statement of cash flows:

49. If cash dividends of $145,000 were declared during the year and the decrease in dividends payable from the

beginning to the end of the year was $7,000, the statement of cash flows would report $152,000 in the financing

50. Repayments of bonds would be shown as a cash outflow in the investing section of the statement of cash

51. To determine cash payments for operating expenses for the cash flow statement using the direct method, a

60. East, Inc. had beginning inventory of $10,000, purchases of $25,000, and ending inventory of $5,000. What

61. Dig, Inc. had the following merchandise transactions in October:

Purchases

$50,000

Purchase returns

$ 4,000

Purchase discounts

$ 1,000

Transportation in

$ 2,000

66. NBC Company had $32,000 in net sales, $15,000 in cost of merchandise sold, $18,000 in operating

71. The form of income statement that derives its name from the fact that the total of all expenses is deducted

73. A. Bonds Company

The following is a single-step income statement for the A. Bonds Company:

A. $200,000.

B. $127,500.

C. $101,000.

D. $152,500.

74. A. Bonds Company

The following is a single-step income statement for the A. Bonds Company:

A. Bonds Company

Income Statement

For the Year Ended December 31, 2013

Revenues:

Net Sales

$250,000

Interest Income

17,500

A. $101,000.

B. $113,500.

C. $118,500.

D. $152,500.

75. Which of the following would be subtracted from gross profit to determine operating income?

A. Operating expenses

B. Other expenses

C. Income taxes

D. All of these

76. Merchandise not sold at the end of the period is reported as:

A. cost of goods sold.

B. old stock.

C. merchandise inventory.

D. net purchases.

80. Deana, Inc.

Deana, Inc. purchased merchandise for $500,000, received credit for purchase returns of $25,000, took purchase

discounts of $10,000, and paid transportation in of $20,000.

81. Deana, Inc.

Deana, Inc. purchased merchandise for $500,000, received credit for purchase returns of $25,000, took purchase

discounts of $10,000, and paid transportation in of $20,000.

Refer to Deana, Inc. If Deana, Inc. had $20,000 in beginning inventory, and sold goods costing $300,000, what

83. Which of the following accounts will not be found in the Cost of Merchandise Sold section on the income

87. Gold Co. sold merchandise to Bronze Co. on account, $25,000, terms 2/15, net 45. The cost of the

merchandise sold is $18,500. Gold Co. issued a credit memorandum for $2,500 for merchandise returned that

originally cost $1,900. Bronze Co. paid the invoice within the discount period. What is amount of net sales from

91. If Martin, Inc. sold $550,000 worth of merchandise, had $50,000 returned, and then the balance paid during

93. Merchandise is ordered on November 12; the merchandise is shipped by the seller and the invoice is

prepared, dated, and mailed by the seller on November 15; the merchandise is received by the buyer on

November 17; the transaction is recorded in the buyer's accounts on November 18. The credit period begins

94. Merchandise is ordered on November 12; the merchandise is shipped by the seller and the invoice is

prepared, dated, and mailed by the seller on November 15; the merchandise is received by the buyer on

November 17; the transaction is recorded in the seller's accounts on November 15. If the credit terms are 1/10,

95. A sales invoice included the following information: merchandise price, $4,500; transportation, $300; terms

1/10, n/eom, FOB shipping point. Assuming that a credit for merchandise returned of $600 is granted prior to

payment, that the transportation is prepaid by the seller, and that the invoice is paid within the discount period,

96. Sometimes a(n) _____ is offered to buyers as a means of encouraging them to pay before the end of the

98. If a $20,000 sale is made on January 1, with terms of 2/10, n/30, how much would the discount be if

101. In recording the cost of merchandise sold for cash using a perpetual inventory system, the effect on the

103. For the perpetual inventory system, which of the following effects does not occur upon the return from a

104. If merchandise sold on account is returned to the seller, the seller may inform the customer of the details

105. Merchandise subject to terms 1/10, n/30, FOB shipping point, is sold on account to a customer for $20,000.

The seller issued a credit memorandum for $5,000 prior to payment. What is the amount of the cash discount

106. Orange Co. sells merchandise on credit to Zea Co. in the amount of $9,000. The invoice is dated on

September 15 with terms of 1/15, net 45. What is the amount of the discount, and up to what date must the

107. Based on the following information, what would be recorded as purchases discount if the invoice is paid

within the discount period?

1.

$5,000 of merchandise inventory was ordered on April 2, 2010.

2.

$2,000 of this merchandise was received on April 5, 2010.

4.

On April 10, 2010, $500 of the merchandise was returned to the seller.

111. Using a perpetual inventory system, the purchase of $30,000 of merchandise on account would include

114. A sales invoice included the following information: merchandise price, $5,000; terms 1/10, n/eom.

Assuming that a credit for merchandise returned of $600 is granted prior to payment, and that the invoice is paid

115. A sales invoice included the following information: merchandise price, $6,000; terms 2/10, n/eom.

Assuming that a credit for merchandise returned of $600 is granted prior to payment, and that the invoice is paid

116. Merchandise subject to terms 1/10, n/30, FOB shipping point, is sold on account to a customer for $17,500.

The seller issued a credit memorandum for $4,000 prior to payment. What is the amount of the cash discount

119. If title to merchandise purchases passes to the buyer when the goods are shipped from the seller, the terms

120. If title to merchandise purchases passes to the buyer when the goods are delivered to the buyer, the terms

121. Merchandise with an invoice price of $6,000 is purchased subject to terms of 2/10, n/30, FOB destination.

126. Under the indirect method for preparing the statement of cash flows, increases in current liabilities are

127. Which of the following would not affect the operating activities section of the statement of cash flows,

128. A company has a net income of $39,000 and depreciation expenses of $9,000. During the year, its accounts

payable balance decreased by $5,000. What is the net cash flow from operating activities using the indirect

129. Under the indirect method for preparing the statement of cash flows, decreases in current assets are _____

131. ONI, Inc. purchased $60,000 of equipment for cash. How does this transaction impact the statement of

133. The following data for the year ended June 30, 2013, were extracted from the accounting records of Roof

Co.:

134. The following data for the current year ended December 31, 2013, were extracted from the accounting

records of Gilbert Co.:

135. Prepare a multiple-step income statement for Surry Co. from the following data for the year ended

December 31, 2013.

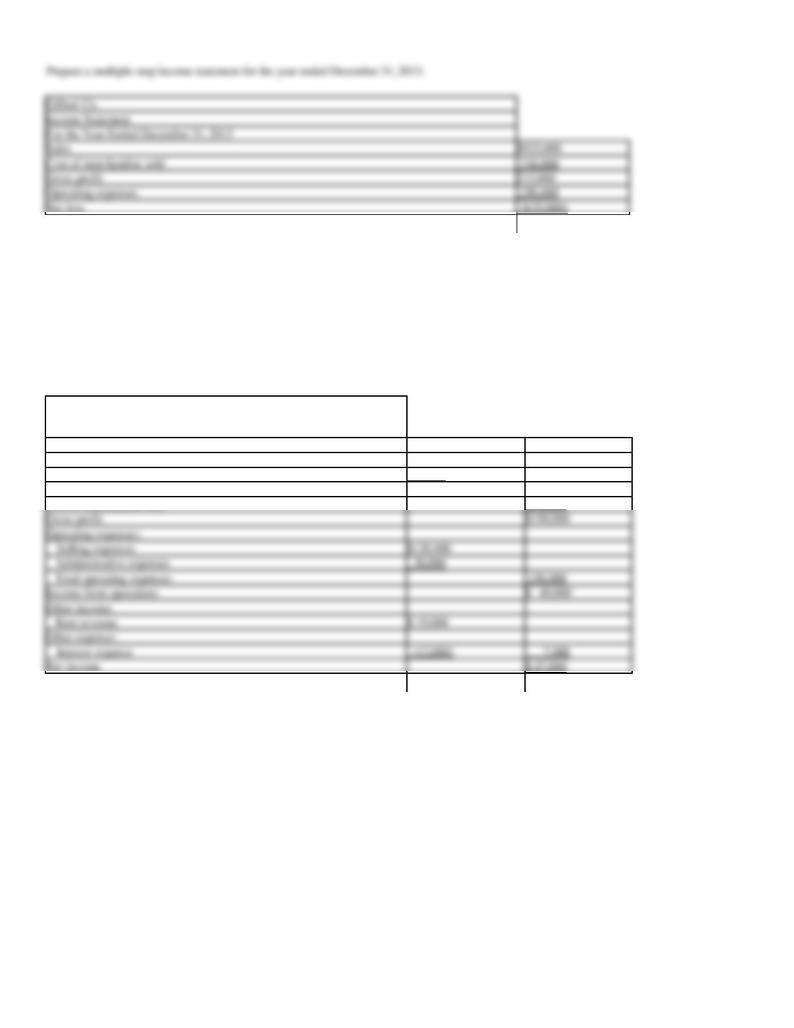

136. Selected data from the ledger of Wiles Co. after adjustment at June 30, the end of the fiscal year, are listed

as follows:

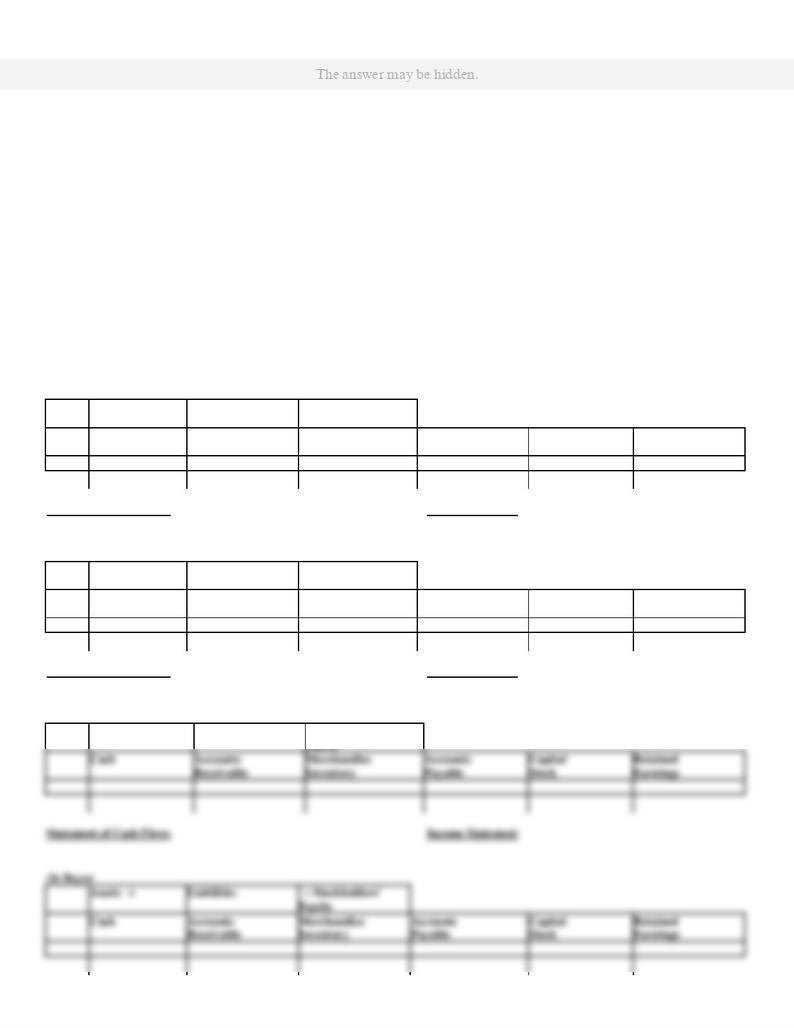

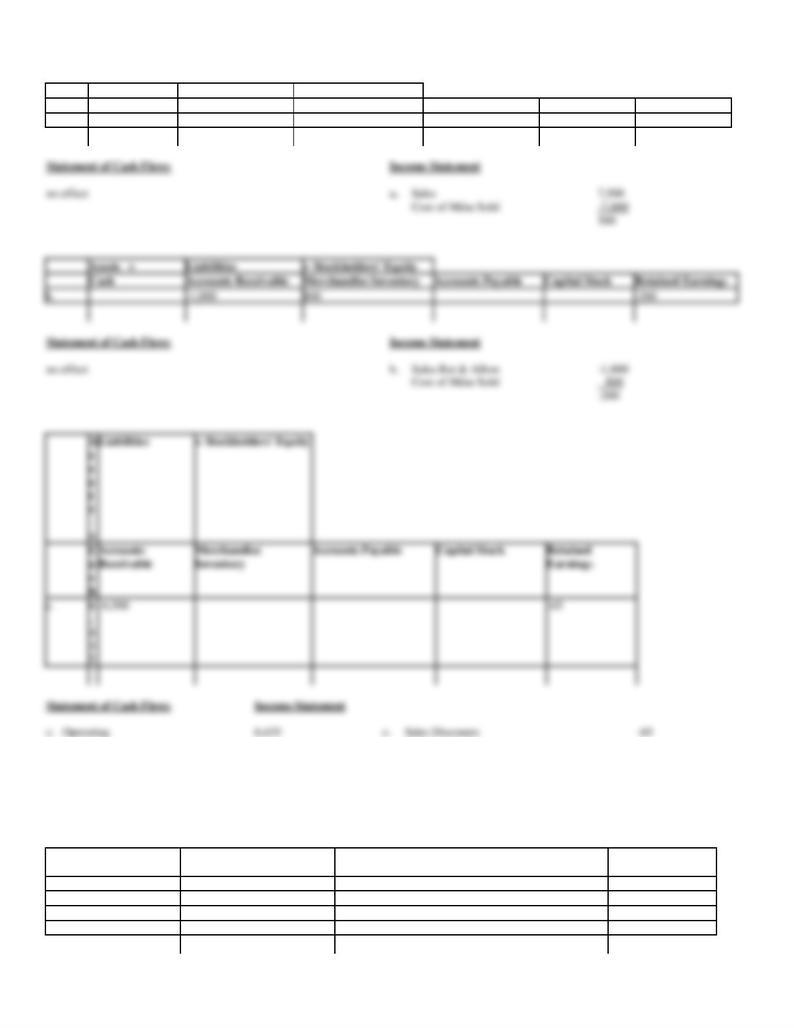

137. Merchandise with a list price of $7,500 and a cost of $7,000 is sold on account, terms 1/10, n/30. Prior to

payment, merchandise with a list price of $1,000 and a cost of $800 is returned. The correct amount is paid

within the discount period.

Record the following transactions, using the integrated financial statement framework that follows:

(a)

Sold the merchandise.

(b)

Received the returned merchandise

(c)

Received the amount owed.

Assets =

Liabilities

+ Stockholders' Equity

Cash

Accounts Receivable

Merchandise Inventory

Accounts Payable

Capital Stock

Retained Earnings

a.

138. Details of invoices for purchases of merchandise are as follows:

Merchandise

Transportation

Terms

Returns and

Allowances

139. Based on the information below, illustrate the effects on the accounts and financial statements of the Seller

and the Buyer. Both use a perpetual inventory system.

(a)

Seller sells Buyer on account merchandise costing $300 for $500, terms 2/10, net 30, FOB destination. The transportation charge is $50.

(b)

Buyer returns as defective $100 worth of the $500 merchandise received. The seller's cost is $60.

(c)

Buyer pays within the discount period.

(a) Seller

Assets =

Liabilities

+ Stockholders'

Equity

Cash

Accounts

Receivable

Merchandise

Inventory

Accounts

Payable

Capital

Stock

Retained

Earnings

Statement of Cash Flows

Income Statement

(a) Buyer

Assets =

Liabilities

+ Stockholders'

Equity

Cash

Accounts

Receivable

Merchandise

Inventory

Accounts

Payable

Capital

Stock

Retained

Earnings

Statement of Cash Flows

Income Statement

(b) Seller

Assets =

Liabilities

+ Stockholders'

Equity

140. State the section(s) of the statement of cash flows prepared by the indirect method (operating activities,

investing activities, financing activities, or not reported) and the amount that would be reported for each of the

following transactions:

(a)

Received $145,000 from the sale of land costing $70,000.

(b)

Purchased investments for $50,000.

141. Gold Co. sold merchandise to Bronze Co. on account, $23,000, terms 2/15, net 45. The cost of the

merchandise sold is $18,500. Gold Co. issued a credit memorandum for $2,500 for merchandise returned that

originally cost $1,900. Bronze Co. paid the invoice within the discount period. What is the amount of net

income earned by Gold Co. on the transactions?

142. Based on the following data, determine the cost of merchandise sold for October.

Chapter 4--Accounting for Merchandising Businesses Key

1. Operating expenses are subtracted from fees earned for a service business and from gross profit for a

4. Net income or loss may appear on the income statement of both a service business and a merchandising

5. On the income statement, sales returns and allowances and sales discounts are added to gross sales to yield

6. On the income statement, sales discounts are normally deducted from sales to yield the cost of merchandise

7. On the income statement, the merchandise inventory at the beginning of the period is added to sales to yield

8. On the income statement in the single-step form, the total of all expenses is deducted from the total of all

9. A criticism of the single-step income statement is that gross profit and income from operations are not readily

16. The indirect method of preparing the statement of cash flows reconciles net income with net cash flows

19. In a multiple-step income statement, sales will be reduced by sales discounts and sales returns and

23. If payment is due by the end of the month in which the sale is made, the invoice terms are expressed as

27. Sales to customers who use bank credit cards, such as MasterCard and VISA, are generally treated as credit

28. The document issued by the seller that informs the buyer of the details of sales returns is called a debit

29. The effect of a sales return and allowance is a reduction in sales revenue and a decrease in cash or accounts

30. When the seller offers a sales discount, even if borrowing has to be done, it is generally advantageous for

31. If merchandise costing $2,500, terms FOB destination, 2/10, n/30, with prepaid transportation costs of $100,

32. A buyer who acquires merchandise under credit terms of 1/10, n/30 has 30days after the invoice date to take

33. Available discounts taken by the buyer for early payment of an invoice are termed sales discounts by the

34. Purchases of merchandise increase the merchandise inventory account under the perpetual inventory

35. A buyer who acquires merchandise under credit terms of 1/10, n/30 has 10 days after the invoice date to

37. In a perpetual inventory system, merchandise returned to vendors reduces the merchandise inventory

39. If the ownership of merchandise passes to the buyer when the seller delivers the merchandise for shipment,

40. Merchandise is sold for $2,500, terms FOB destination, 2/10, n/30, with transportation costs of $150. If

$500 of the merchandise is returned prior to payment and the invoice is paid within the discount period, the

42. If merchandise costing $2,500, terms FOB destination, 2/10, n/30, with transportation costs of $100, is paid

43. When someone purchases merchandise and incurs the cost of transportation, these costs of purchasing

45. In a transaction where purchased merchandise has been returned, the buyer will increase the Sales Returns

48. There are two alternatives to reporting cash flows from operating activities in the statement of cash flows:

49. If cash dividends of $145,000 were declared during the year and the decrease in dividends payable from the

beginning to the end of the year was $7,000, the statement of cash flows would report $152,000 in the financing

50. Repayments of bonds would be shown as a cash outflow in the investing section of the statement of cash

51. To determine cash payments for operating expenses for the cash flow statement using the direct method, a

60. East, Inc. had beginning inventory of $10,000, purchases of $25,000, and ending inventory of $5,000. What

61. Dig, Inc. had the following merchandise transactions in October:

Purchases

$50,000

Purchase returns

$ 4,000

Purchase discounts

$ 1,000

Transportation in

$ 2,000

66. NBC Company had $32,000 in net sales, $15,000 in cost of merchandise sold, $18,000 in operating

71. The form of income statement that derives its name from the fact that the total of all expenses is deducted

73. A. Bonds Company

The following is a single-step income statement for the A. Bonds Company:

A. $200,000.

B. $127,500.

C. $101,000.

D. $152,500.

74. A. Bonds Company

The following is a single-step income statement for the A. Bonds Company:

A. Bonds Company

Income Statement

For the Year Ended December 31, 2013

Revenues:

Net Sales

$250,000

Interest Income

17,500

A. $101,000.

B. $113,500.

C. $118,500.

D. $152,500.

75. Which of the following would be subtracted from gross profit to determine operating income?

A. Operating expenses

B. Other expenses

C. Income taxes

D. All of these

76. Merchandise not sold at the end of the period is reported as:

A. cost of goods sold.

B. old stock.

C. merchandise inventory.

D. net purchases.

80. Deana, Inc.

Deana, Inc. purchased merchandise for $500,000, received credit for purchase returns of $25,000, took purchase

discounts of $10,000, and paid transportation in of $20,000.

81. Deana, Inc.

Deana, Inc. purchased merchandise for $500,000, received credit for purchase returns of $25,000, took purchase

discounts of $10,000, and paid transportation in of $20,000.

Refer to Deana, Inc. If Deana, Inc. had $20,000 in beginning inventory, and sold goods costing $300,000, what

83. Which of the following accounts will not be found in the Cost of Merchandise Sold section on the income

87. Gold Co. sold merchandise to Bronze Co. on account, $25,000, terms 2/15, net 45. The cost of the

merchandise sold is $18,500. Gold Co. issued a credit memorandum for $2,500 for merchandise returned that

originally cost $1,900. Bronze Co. paid the invoice within the discount period. What is amount of net sales from

91. If Martin, Inc. sold $550,000 worth of merchandise, had $50,000 returned, and then the balance paid during

93. Merchandise is ordered on November 12; the merchandise is shipped by the seller and the invoice is

prepared, dated, and mailed by the seller on November 15; the merchandise is received by the buyer on

November 17; the transaction is recorded in the buyer's accounts on November 18. The credit period begins

94. Merchandise is ordered on November 12; the merchandise is shipped by the seller and the invoice is

prepared, dated, and mailed by the seller on November 15; the merchandise is received by the buyer on

November 17; the transaction is recorded in the seller's accounts on November 15. If the credit terms are 1/10,

95. A sales invoice included the following information: merchandise price, $4,500; transportation, $300; terms

1/10, n/eom, FOB shipping point. Assuming that a credit for merchandise returned of $600 is granted prior to

payment, that the transportation is prepaid by the seller, and that the invoice is paid within the discount period,

96. Sometimes a(n) _____ is offered to buyers as a means of encouraging them to pay before the end of the

98. If a $20,000 sale is made on January 1, with terms of 2/10, n/30, how much would the discount be if

101. In recording the cost of merchandise sold for cash using a perpetual inventory system, the effect on the

103. For the perpetual inventory system, which of the following effects does not occur upon the return from a

104. If merchandise sold on account is returned to the seller, the seller may inform the customer of the details

105. Merchandise subject to terms 1/10, n/30, FOB shipping point, is sold on account to a customer for $20,000.

The seller issued a credit memorandum for $5,000 prior to payment. What is the amount of the cash discount

106. Orange Co. sells merchandise on credit to Zea Co. in the amount of $9,000. The invoice is dated on

September 15 with terms of 1/15, net 45. What is the amount of the discount, and up to what date must the

107. Based on the following information, what would be recorded as purchases discount if the invoice is paid

within the discount period?

1.

$5,000 of merchandise inventory was ordered on April 2, 2010.

2.

$2,000 of this merchandise was received on April 5, 2010.

4.

On April 10, 2010, $500 of the merchandise was returned to the seller.

111. Using a perpetual inventory system, the purchase of $30,000 of merchandise on account would include

114. A sales invoice included the following information: merchandise price, $5,000; terms 1/10, n/eom.

Assuming that a credit for merchandise returned of $600 is granted prior to payment, and that the invoice is paid

115. A sales invoice included the following information: merchandise price, $6,000; terms 2/10, n/eom.

Assuming that a credit for merchandise returned of $600 is granted prior to payment, and that the invoice is paid

116. Merchandise subject to terms 1/10, n/30, FOB shipping point, is sold on account to a customer for $17,500.

The seller issued a credit memorandum for $4,000 prior to payment. What is the amount of the cash discount

119. If title to merchandise purchases passes to the buyer when the goods are shipped from the seller, the terms

120. If title to merchandise purchases passes to the buyer when the goods are delivered to the buyer, the terms

121. Merchandise with an invoice price of $6,000 is purchased subject to terms of 2/10, n/30, FOB destination.

126. Under the indirect method for preparing the statement of cash flows, increases in current liabilities are

127. Which of the following would not affect the operating activities section of the statement of cash flows,

128. A company has a net income of $39,000 and depreciation expenses of $9,000. During the year, its accounts

payable balance decreased by $5,000. What is the net cash flow from operating activities using the indirect

129. Under the indirect method for preparing the statement of cash flows, decreases in current assets are _____

131. ONI, Inc. purchased $60,000 of equipment for cash. How does this transaction impact the statement of

133. The following data for the year ended June 30, 2013, were extracted from the accounting records of Roof

Co.:

134. The following data for the current year ended December 31, 2013, were extracted from the accounting

records of Gilbert Co.:

135. Prepare a multiple-step income statement for Surry Co. from the following data for the year ended

December 31, 2013.

Sales, $915,000; cost of merchandise sold, $670,000; administrative expenses, $30,000; interest expense,

$12,000; rent revenue, $19,000; sales returns and allowances, $55,000; selling expenses, $120,000.

Surry Co.

Income Statement

For the Year Ended December 31, 2013

Revenue from sales:

Sales

$915,000

Less: Sales returns and allowances

55,000

Net sales

$860,000

Cost of merchandise sold

670,000

136. Selected data from the ledger of Wiles Co. after adjustment at June 30, the end of the fiscal year, are listed

as follows:

Accounts Receivable

$39,120

Prepaid Insurance

$ 4,680

Accumulated Depreciation

60,540

Notes Payable

77,750

Administrative Expenses

90,500

Retained Earnings

75,000

Capital Stock

60,000

Salaries Payable

3,060

Cost of Merchandise Sold

655,000

Sales (net)

920,000

Dividends

40,000

Selling Expenses

110,000

Interest Revenue

10,500

Supplies

3,125

Office Equipment

82,700

Prepare a single-step income statement for the year ended June 30, 2013.

137. Merchandise with a list price of $7,500 and a cost of $7,000 is sold on account, terms 1/10, n/30. Prior to

payment, merchandise with a list price of $1,000 and a cost of $800 is returned. The correct amount is paid

within the discount period.

Record the following transactions, using the integrated financial statement framework that follows:

(a)

Sold the merchandise.

(b)

Received the returned merchandise

(c)

Received the amount owed.

Assets =

Liabilities

+ Stockholders' Equity

Cash

Accounts Receivable

Merchandise Inventory

Accounts Payable

Capital Stock

Retained Earnings

a.

Statement of Cash Flows

Income Statement

Assets =

Liabilities

+ Stockholders' Equity

Cash

Accounts Receivable

Merchandise Inventory

Accounts Payable

Capital Stock

Retained Earnings

b.

Statement of Cash Flows

Income Statement

Assets =

Liabilities

+ Stockholders' Equity

Cash

Accounts Receivable

Merchandise Inventory

Accounts Payable

Capital Stock

Retained Earnings

c.

Statement of Cash Flows

Income Statement

Assets =

Liabilities

+ Stockholders' Equity

Cash

Accounts Receivable

Merchandise Inventory

Accounts Payable

Capital Stock

Retained Earnings

a.

7,500

-7,000

500

138. Details of invoices for purchases of merchandise are as follows:

Merchandise

Transportation

Terms

Returns and

Allowances

a. $1,000

$25

FOB shipping point, 1/10, n/30

$200

b. 5,000

---

FOB destination, n/30

400

c. 4,000

50

FOB shipping point, 2/10, n/30

150

d. 5,000

---

FOB destination, 1/10, n/30

---

Determine the amount to be paid in full settlement of each of the invoices, assuming that credit for returns and allowances was received prior to

payment and that all invoices were paid within the discount period. Also assume that the seller has prepaid the transportation expenses.

139. Based on the information below, illustrate the effects on the accounts and financial statements of the Seller

and the Buyer. Both use a perpetual inventory system.

(a)

Seller sells Buyer on account merchandise costing $300 for $500, terms 2/10, net 30, FOB destination. The transportation charge is $50.

(b)

Buyer returns as defective $100 worth of the $500 merchandise received. The seller's cost is $60.

(c)

Buyer pays within the discount period.

(a) Seller

Assets =

Liabilities

+ Stockholders'

Equity

Cash

Accounts

Receivable

Merchandise

Inventory

Accounts

Payable

Capital

Stock

Retained

Earnings

Statement of Cash Flows

Income Statement

(a) Buyer

Assets =

Liabilities

+ Stockholders'

Equity

Cash

Accounts

Receivable

Merchandise

Inventory

Accounts

Payable

Capital

Stock

Retained

Earnings

Statement of Cash Flows

Income Statement

(b) Seller

Assets =

Liabilities

+ Stockholders'

Equity

(a) Seller

Assets =

Liabilities

+ Stockholders'

Equity

Cash

Accounts

Receivable

Merchandise

Inventory

Accounts

Payable

Capital

Stock

Retained

Earnings

500

-300

200

-50

150

Statement of Cash Flows

Income Statement

no effect

Sales

500

Cost of Mdse Sold

-300

Delivery Expenses

-50

Effect onNet Income

150

(a) Buyer

Assets =

Liabilities

+ Stockholders'

Equity

Cash

Accounts

Receivable

Merchandise

Inventory

Accounts

Payable

Capital

Stock

Retained

Earnings

500

500

Statement of Cash Flows

Income Statement

no effect

no effect

(b) Seller

Assets =

Liabilities

+ Stockholders'

Equity

Cash

Accounts

Receivable

Merchandise

Inventory

Accounts

Payable

Capital

Stock

Retained

Earnings

140. State the section(s) of the statement of cash flows prepared by the indirect method (operating activities,

investing activities, financing activities, or not reported) and the amount that would be reported for each of the

following transactions:

(a)

Received $145,000 from the sale of land costing $70,000.

(b)

Purchased investments for $50,000.

(c)

Declared $35,000 cash dividends on stock. $5,000 dividends were payable at the beginning of the year, and $6,000 were payable at the

end of the year.

(d)

Acquired equipment for $32,000 cash.

(e)

Declared and issued 100 shares of $20 par common stock as a stock dividend, when the market price of the stock was $32 a share.

(f)

Recognized by an adjusting entry depreciation for the year, $48,000.

141. Gold Co. sold merchandise to Bronze Co. on account, $23,000, terms 2/15, net 45. The cost of the

merchandise sold is $18,500. Gold Co. issued a credit memorandum for $2,500 for merchandise returned that

originally cost $1,900. Bronze Co. paid the invoice within the discount period. What is the amount of net

income earned by Gold Co. on the transactions?

$3,490 (Net Sales $23,000 - $2,500 - $410) - (Cost of Merchandise Sold $18,500 - $1,900)

142. Based on the following data, determine the cost of merchandise sold for October.

Cost of merchandise sold:

Merchandise Inventory, October 1

$98,560

Purchases

$433,880

Less: Purchases returns and allowances

$12,760